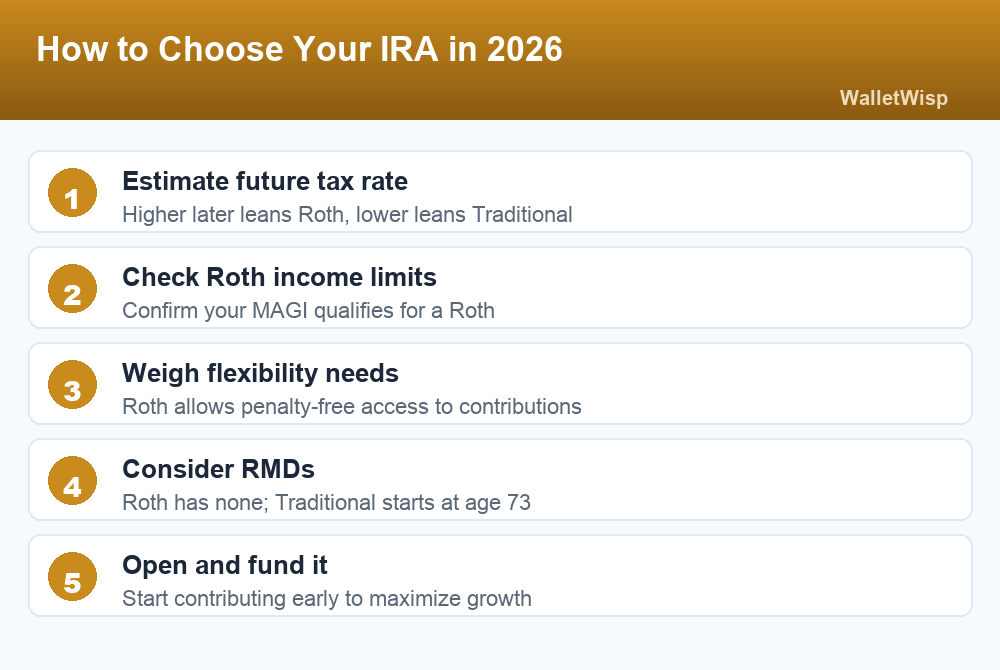

The choice between a Traditional vs Roth IRA comes down to one question: do you want your tax break now or in retirement? A Traditional IRA gives you a tax deduction today and taxes your withdrawals later, while a Roth IRA is funded with after-tax dollars and pays out completely tax-free in retirement. If you expect to be in a higher tax bracket later or you are early in your career, the Roth usually wins; if you need the deduction now and expect a lower bracket in retirement, the Traditional often makes more sense.

Both accounts share the same 2026 contribution limit and both are among the most powerful tax-advantaged tools available to everyday US savers. The difference is entirely about timing, income eligibility, and how much flexibility you want along the way. Below we break down every factor that matters so you can decide with confidence.

Traditional vs Roth IRA: The Core Difference

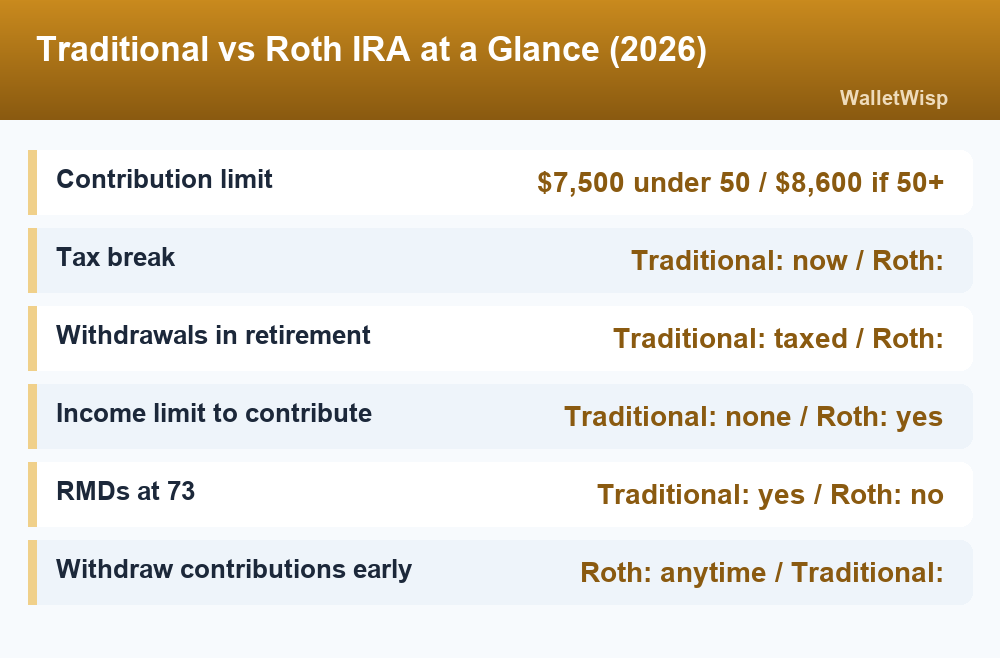

The single biggest difference is when you pay taxes. A Traditional IRA is tax-deferred, and a Roth IRA is tax-free at the end.

How a Traditional IRA is taxed

Contributions may be tax-deductible in the year you make them, which lowers your taxable income now. Your money grows tax-deferred, and you pay ordinary income tax on every dollar you withdraw in retirement. In short: tax break today, tax bill later.

How a Roth IRA is taxed

You contribute money you have already paid taxes on, so there is no deduction upfront. The trade-off is powerful: your investments grow tax-free, and qualified withdrawals in retirement are 100% tax-free, including all the growth. In short: no tax break today, no tax bill later.

This is why the Roth is so often recommended for younger savers. If you invest $7,000 that grows to $70,000 over decades, a Roth lets you keep the entire $70,000, while a Traditional IRA would have that full amount taxed as income on the way out.

2026 Contribution Limits and Income Rules

For 2026, the IRS sets the same base contribution limit for both account types. You can split your contribution between a Traditional and a Roth IRA, but the combined total cannot exceed the annual cap.

| 2026 IRA Rule | Traditional IRA | Roth IRA |

|---|---|---|

| Contribution limit (under 50) | $7,500 | $7,500 |

| Catch-up contribution (50+) | +$1,100 | +$1,100 |

| Total limit if 50 or older | $8,600 | $8,600 |

| Tax break timing | Now (deductible) | In retirement (tax-free) |

| Direct income limit to contribute | None | Yes (phases out at high income) |

| Required Minimum Distributions | Yes, starting at age 73 | None for the original owner |

The most important structural difference in eligibility: anyone with earned income can contribute to a Traditional IRA, but a Roth IRA has a direct income ceiling. High earners may be phased out of contributing to a Roth altogether. For a fuller breakdown of the numbers, see our guide to IRA contribution limits for 2026.

Roth IRA income phase-out ranges (2026)

Your ability to contribute to a Roth IRA depends on your modified adjusted gross income (MAGI) and filing status. Inside the phase-out range you can make a reduced contribution; above it you cannot contribute directly at all.

| Filing status | Full contribution below | Phase-out range | No direct Roth above |

|---|---|---|---|

| Single / Head of household | $153,000 | $153,000 – $168,000 | $168,000 |

| Married filing jointly | $242,000 | $242,000 – $252,000 | $252,000 |

| Married filing separately | $0 | $0 – $10,000 | $10,000 |

The Traditional IRA has no income limit to contribute, but if you (or a spouse) are covered by a workplace retirement plan like a 401(k), your ability to deduct the contribution phases out at higher incomes. You can still contribute; you just may not get the full deduction.

Required Minimum Distributions (RMDs)

This is a major and often overlooked advantage of the Roth. Traditional IRAs require you to start taking Required Minimum Distributions at age 73, whether you need the money or not. Those forced withdrawals are taxed as income and can push you into a higher bracket in your 70s and beyond.

A Roth IRA has no RMDs during the original owner’s lifetime. Your money can keep growing tax-free for as long as you live, which makes the Roth a strong tool for both flexibility and estate planning. If leaving tax-free money to heirs matters to you, the Roth has a clear edge.

Early-Withdrawal Rules Compared

Retirement accounts are meant for retirement, but life happens. The two accounts treat early access very differently, and the Roth is far more flexible.

Roth IRA early withdrawals

Because you already paid taxes on your contributions, you can withdraw your contributions (not the earnings) at any time, at any age, with no taxes and no penalty. Earnings are different: to withdraw earnings tax- and penalty-free, you generally must be at least 59.5 and have had the account open for at least five years. This contribution flexibility is a big reason beginners like the Roth; learn more in our Roth IRA guide for beginners.

Traditional IRA early withdrawals

With a Traditional IRA, nearly every early withdrawal before age 59.5 is subject to ordinary income tax plus a 10% penalty, because none of the money has been taxed yet. There is no way to pull out contributions penalty-free the way you can with a Roth.

Exceptions that apply to both

Both account types allow penalty-free early withdrawals (though taxes may still apply on Traditional funds) for certain situations, including:

- Up to $10,000 toward a first-home purchase

- Qualified higher-education expenses

- Certain unreimbursed medical expenses

- Birth or adoption expenses (up to $5,000)

- A qualifying disability

Who Should Choose a Roth IRA?

A Roth IRA tends to be the better fit if:

- You are young or early in your career and in a relatively low tax bracket now.

- You expect your income and tax rate to be higher in retirement.

- You want maximum flexibility to access your contributions if needed.

- You want to avoid Required Minimum Distributions.

- You want to leave tax-free money to your heirs.

The core Roth bet is simple: pay a known tax rate today to lock in tax-free income for life. For most savers under 40, that bet is very often the right one.

Who Should Choose a Traditional IRA?

A Traditional IRA tends to be the better fit if:

- You are a high earner today and want to lower this year’s tax bill.

- You expect to be in a lower tax bracket in retirement than you are now.

- Your income exceeds the Roth eligibility limits.

- You value the upfront deduction to free up cash for other goals.

The core Traditional bet is that your tax rate will be lower when you withdraw the money than it is today. For peak earners in their 40s and 50s, that is often a reasonable assumption.

Can You Have Both?

Yes, and many people do. You can own both a Traditional and a Roth IRA and split contributions between them, as long as your combined total stays within the annual limit ($7,500 under 50, or $8,600 if 50 or older in 2026). Splitting contributions is a form of “tax diversification” that gives you both taxable and tax-free income sources in retirement, which adds flexibility when managing your future tax bracket.

There is also a strategy called the “backdoor Roth” for high earners who exceed the Roth income limits: you contribute to a Traditional IRA and then convert it to a Roth. It works but has tax complications, so it is worth confirming the details with a tax professional before attempting it.

Don’t Forget the HSA

If you have a high-deductible health plan, a Health Savings Account can be an even more tax-efficient home for some of your savings, offering a deduction now and tax-free medical withdrawals later. Many savers fund an HSA alongside an IRA; see our breakdown of how the HSA works in 2026 to decide how it fits into your plan.

The Bottom Line

There is no universally “best” account in the Traditional vs Roth IRA debate; there is only the best account for your situation. Ask yourself whether your tax rate is more likely to be higher or lower in retirement. If higher, lean Roth. If lower, lean Traditional. If you are unsure, the Roth’s tax-free growth, contribution flexibility, and lack of RMDs make it a safe default for most younger and middle-income savers. The most important move of all is simply to open one and start contributing, because time in the market matters far more than which flavor of IRA you pick.

Frequently Asked Questions

What is the main difference between a Traditional and Roth IRA?

The main difference is tax timing. A Traditional IRA gives you a tax deduction now and taxes your withdrawals in retirement, while a Roth IRA is funded with after-tax money and gives you tax-free withdrawals in retirement.

What are the 2026 IRA contribution limits?

For 2026, you can contribute up to $7,500 if you are under 50, or $8,600 if you are 50 or older thanks to a $1,100 catch-up contribution. This is a combined limit across all your Traditional and Roth IRAs.

Is a Roth or Traditional IRA better for young people?

A Roth IRA is usually better for young savers. When you are early in your career and likely in a lower tax bracket, paying tax now to secure decades of tax-free growth and tax-free withdrawals is typically the stronger long-term move.

Can I contribute to both a Traditional and Roth IRA?

Yes. You can contribute to both in the same year, but your combined contributions cannot exceed the annual limit of $7,500 (or $8,600 if you are 50 or older in 2026).

What is the income limit for a Roth IRA in 2026?

For 2026, single filers can make a full Roth contribution below $153,000 in MAGI, phasing out entirely at $168,000. Married couples filing jointly phase out between $242,000 and $252,000.

Do Roth IRAs have required minimum distributions?

No. Roth IRAs have no required minimum distributions during the original owner’s lifetime, so your money can keep growing tax-free. Traditional IRAs require you to begin taking RMDs at age 73.

Can I withdraw money from my IRA early without a penalty?

With a Roth IRA you can withdraw your contributions anytime tax- and penalty-free. Traditional IRA withdrawals before age 59.5 generally face income tax plus a 10% penalty, though both accounts have exceptions for things like a first home or higher education.

Which IRA should I choose if I don’t know my future tax rate?

When you are unsure, the Roth IRA is often the safer default because of its tax-free growth, flexible access to contributions, and lack of RMDs. You can also split contributions between both accounts to hedge your bet and diversify your future tax exposure.

")

{kind=link}