A CD ladder is a savings strategy where you split your money across several certificates of deposit that mature at different times, so you capture the higher yields of longer terms while still freeing up a slice of cash on a predictable schedule. In 2026, with rates still relatively elevated but the Federal Reserve holding steady and the outlook uncertain, laddering is a sensible middle ground between locking everything into one long CD and leaving it all in savings.

Quick answer: To build a CD ladder, divide your money into equal parts and buy CDs with staggered terms – a classic version uses 1-, 2-, 3-, 4-, and 5-year CDs. Each year one CD matures, and you reinvest it into a new 5-year CD. That keeps roughly one-fifth of your cash accessible every year while most of your balance earns longer-term rates. Compare current rates before you commit, and keep every deposit within FDIC or NCUA limits.

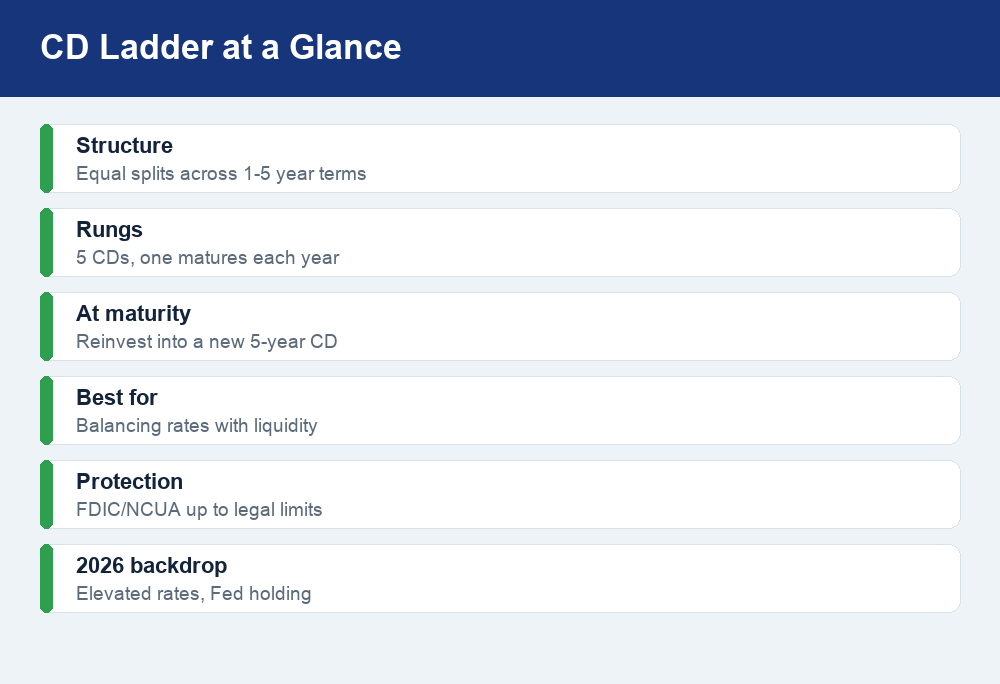

What is a CD ladder?

A certificate of deposit (CD) is a savings product where you agree to leave a lump sum with a bank or credit union for a fixed term – anywhere from a few months to five years or more – in exchange for a fixed interest rate. Generally, the longer the term, the higher the rate. The catch is liquidity: if you pull the money out before the term ends, you usually pay an early-withdrawal penalty.

A CD ladder solves that trade-off by spreading your money across multiple CDs with different maturity dates instead of putting it all in one. Picture a real ladder: each rung is a separate CD, and the rungs are spaced a year apart. Instead of choosing between a high rate (long term) and easy access (short term), you get a bit of both. Some of your money is always coming due soon, and the rest is locked in at longer-term rates.

The most common version is a five-year ladder with five equal rungs. You split your total across 1-, 2-, 3-, 4-, and 5-year CDs. After the first year, the 1-year CD matures. You either take that cash or – to keep the ladder going – reinvest it into a brand-new 5-year CD. Do that each year, and after five years every rung is a 5-year CD, but one still matures every twelve months. You end up earning the highest term rates while never being more than a year away from a chunk of penalty-free cash.

Why build a CD ladder in 2026?

The appeal of laddering comes down to two things people usually have to choose between: rate and liquidity. A ladder gives you a workable amount of both.

You hedge against rate uncertainty. As of mid-2026, deposit rates remain relatively elevated, but the Fed has been holding and nobody knows for sure which way rates go next. If you dump everything into a single 5-year CD and rates keep climbing, you’re stuck at yesterday’s rate. If you keep everything in savings and rates fall, your yield drops with them. A ladder splits the difference: because a rung matures every year, you’re regularly reinvesting at whatever the going rate is. If rates rise, your maturing rungs catch the higher yields. If rates fall, most of your money is still locked in at older, better rates.

You keep cash within reach. Money in a long CD is effectively off-limits without a penalty. With a ladder, roughly one rung’s worth of cash frees up each year, so you have a scheduled off-ramp if you need the money or want to change course.

You lock in a known return. Unlike a variable high-yield savings account, a CD’s rate is fixed for the term. Once you buy the rung, that yield is guaranteed no matter what the Fed does. That predictability is one of the biggest reasons savers reach for CDs when the outlook is murky.

Before you build, it’s worth checking where cash yields stand today. It only takes a few minutes to compare current high-yield savings rates against the CD rates your bank is advertising, so you know whether locking money up is actually buying you extra yield.

How to build a CD ladder step by step

Here’s the classic five-year build. You can scale the dollar amounts to whatever you have and adjust the number of rungs, but the mechanics stay the same.

Step 1: Decide how much to ladder. Only use money you won’t need for everyday expenses. A CD ladder is for savings you can leave alone – an emergency fund’s core, a down-payment stash a few years out, or cash you simply want earning more than it does in checking. Keep a separate liquid cushion for surprises so you’re never forced to break a CD early.

Step 2: Split the total into equal parts. For a five-rung ladder, divide your money by five. If you have $25,000, that’s $5,000 per rung.

Step 3: Buy CDs across staggered terms. Open a 1-year, 2-year, 3-year, 4-year, and 5-year CD, each with one equal share. Shop the rate on every term – the best 1-year rate and the best 5-year rate may come from different institutions, and it’s fine to spread rungs across banks.

Step 4: When the shortest rung matures, reinvest it. After year one, your 1-year CD comes due. To keep the ladder rolling, put that money into a new 5-year CD. It becomes the top of the ladder while your old 2-year rung is now the one maturing next.

Step 5: Repeat every year. Each year, the nearest rung matures and you roll it into a fresh 5-year CD. From year five on, every rung is a 5-year CD, yet one still matures annually. Watch maturity dates closely – most CDs auto-renew into a new term if you don’t act during the short grace period, which can quietly relock your cash.

| Rung | Term at purchase | Amount (example) | What happens at maturity |

|---|---|---|---|

| 1 | 1 year | $5,000 | Matures in year 1 – reinvest into a new 5-year CD |

| 2 | 2 years | $5,000 | Matures in year 2 – reinvest into a new 5-year CD |

| 3 | 3 years | $5,000 | Matures in year 3 – reinvest into a new 5-year CD |

| 4 | 4 years | $5,000 | Matures in year 4 – reinvest into a new 5-year CD |

| 5 | 5 years | $5,000 | Matures in year 5 – reinvest into a new 5-year CD |

The pros and cons of CD laddering

Laddering is popular for good reason, but it isn’t the right home for every dollar. Here’s an honest look at both sides.

Pros:

- Balances yield and access – you earn longer-term rates on most of your money while a rung frees up each year.

- Fixed, predictable returns – each rung’s rate is locked for its term, unlike variable savings accounts.

- Reduces timing risk – staggered maturities mean you’re never betting everything on one rate at one moment.

- Low effort once built – after setup, it’s roughly one reinvestment decision a year.

- Insured – held at insured institutions and kept within limits, your principal is protected.

Cons:

- Money is committed – breaking a rung early triggers a penalty, so laddered cash isn’t truly liquid.

- May trail other options – if a strong stock or bond market runs, CDs will likely underperform (though with far less risk).

- Inflation risk – a locked rate can lose ground to rising prices over a multi-year term.

- Some upkeep – you must track maturity dates to avoid unwanted auto-renewals.

- Taxable interest – CD interest is generally taxed as ordinary income in the year it’s earned, even inside a ladder.

CD ladder vs. high-yield savings vs. bonds

A CD ladder isn’t the only place to keep cash you don’t need immediately. The right tool depends on how soon you’ll want the money and how much rate certainty you’re after. The table below sketches the trade-offs.

| Feature | CD ladder | High-yield savings | Bonds / bond funds |

|---|---|---|---|

| Rate type | Fixed per rung | Variable, can change anytime | Fixed (individual) or fluctuating (funds) |

| Access to cash | One rung per year, penalty otherwise | Anytime, fully liquid | Varies; funds sellable, prices move |

| Principal risk | Very low (insured) | Very low (insured) | Low to moderate (prices can fall) |

| Best for | Multi-year cash you want working harder | Emergency funds, near-term spending | Longer horizons, diversification |

| Federal insurance | Yes, FDIC/NCUA | Yes, FDIC/NCUA | No (not deposit products) |

Many savers use more than one. A high-yield savings account is ideal for your true emergency fund because it’s fully liquid, while a CD ladder puts your longer-horizon cash to work at fixed rates. If you’re weighing all three side by side, our guide to high-yield savings vs. CDs vs. money market accounts breaks down which fits which goal. And while you’re shopping banks, it’s worth checking whether any offer a bank account sign-up bonus – a one-time cash reward can add meaningfully to your first-year return.

Early-withdrawal penalties: know before you lock in

The single most important fine-print item on any CD is the early-withdrawal penalty. If you take money out before the term ends, the bank typically charges you a set number of days’ or months’ worth of interest. On a short-term CD that penalty might be a few months of interest; on a five-year CD it can be a year or more of interest, which can eat into your principal if the CD hasn’t earned much yet.

Penalties vary widely from one institution to the next, so read the disclosure before you deposit. A well-built ladder is designed to avoid these penalties entirely – because a rung matures every year, you rarely need to break a CD early. That’s exactly why keeping a separate, liquid emergency fund matters: it means you’re never forced to crack open a rung at the worst possible time. A handful of banks advertise “no-penalty” CDs, but they usually pay lower rates, so weigh the flexibility against the yield you give up.

FDIC and NCUA coverage: keep your ladder safe

One of the biggest reasons CDs feel safe is federal deposit insurance. CDs at FDIC-insured banks and NCUA-insured credit unions are protected up to the legal limit per depositor, per institution, per ownership category. If the bank fails, your insured balance – principal and accrued interest – is covered.

For most savers a modest ladder sits comfortably under the limit at a single institution. But if your ladder is large, or you spread rungs across several banks, confirm each deposit stays within the coverage cap. Because the exact insurance limits and rules can change, verify current coverage directly at the source – FDIC.gov for banks and NCUA.gov for credit unions – and use the FDIC’s or NCUA’s coverage estimator if you’re near the ceiling. Splitting rungs across multiple insured institutions, or across different ownership categories, is a common way to keep a big ladder fully covered.

Frequently asked questions

How much money do I need to start a CD ladder?

There’s no universal minimum. Many CDs open with a few hundred to a thousand dollars, and some have no minimum at all, so you can build a small ladder with modest sums. The key is that the amount is money you can leave untouched for the term. Divide whatever you’re comfortable committing into equal rungs and check each bank’s minimum before you open.

What happens when a CD in my ladder matures?

When a rung matures, you get a short grace period – often around a week to ten days – to decide what to do. You can withdraw the cash penalty-free, or reinvest it into a new CD to keep the ladder going. If you do nothing, most banks automatically renew the CD into a new term at the then-current rate, which may not be what you want. Set a calendar reminder for each maturity date so an auto-renewal never locks you in by accident.

Are CD ladder rates fixed or will they change?

The rate on each individual CD is fixed for that CD’s entire term – that’s guaranteed the moment you open it. What changes over time is the rate you get when you reinvest a maturing rung, since you’re buying a new CD at whatever rates prevail then. That’s the built-in advantage of a ladder: it keeps rolling money into current rates rather than betting everything on one moment. Don’t rely on a rate you saw last month – always confirm the current offer before you buy.

Is a CD ladder better than just using a high-yield savings account?

Neither is strictly “better” – they do different jobs. A high-yield savings account is fully liquid and ideal for money you might need at any moment, but its rate can drop whenever the bank changes it. A CD ladder locks in fixed rates and often pays more on longer terms, at the cost of tying up your cash. Many people keep an emergency fund in savings and ladder the longer-horizon money they won’t touch for a while.

Do I owe taxes on CD interest inside a ladder?

Yes. Interest earned on a CD is generally taxed as ordinary income in the year it’s credited, and your bank will send a 1099-INT if you earn above the reporting threshold. This applies to each rung as it earns interest, even if you reinvest rather than spend it. If taxes are a concern, ask a tax professional about holding CDs inside a tax-advantaged account like an IRA, and verify the current rules at IRS.gov.

The bottom line

A CD ladder is one of the simplest ways to make idle cash work harder without giving up all your access to it. By staggering maturities across 1- to 5-year terms and reinvesting each rung as it comes due, you capture longer-term rates on most of your money while keeping a portion available every year – a smart hedge for 2026’s uncertain rate environment. Build it with money you can leave alone, keep a liquid emergency fund on the side so you never trigger a penalty, stay within FDIC or NCUA insurance limits, and compare current rates before you lock in each rung. Do that, and your ladder can quietly earn a dependable, insured return year after year.

")

{kind=link}