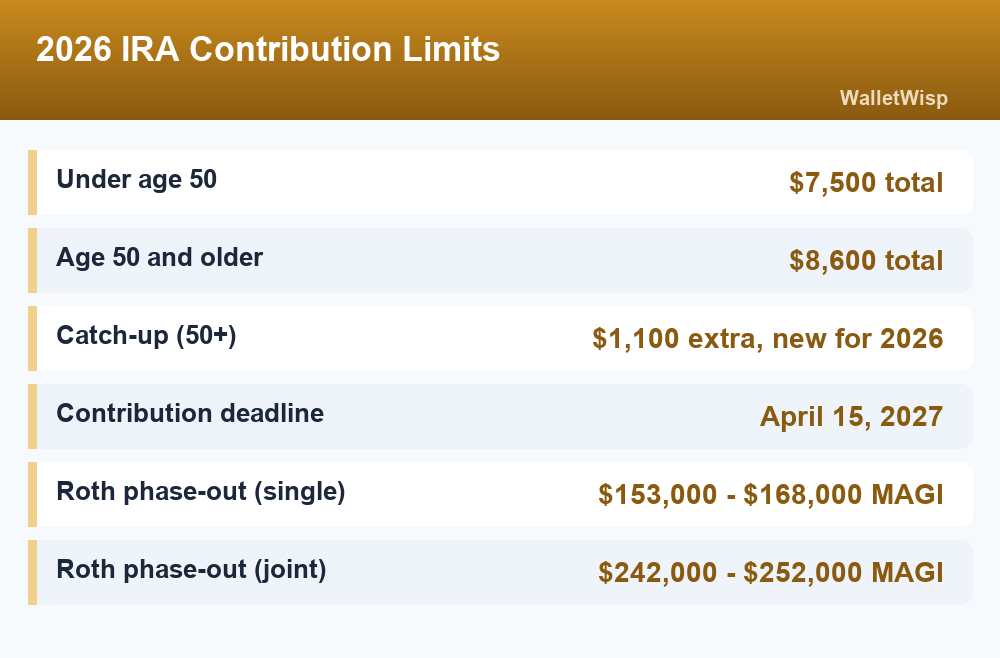

The IRA contribution limits 2026 let you put up to $7,500 into a traditional or Roth IRA if you are under 50, or $8,600 if you are 50 or older thanks to a new $1,100 catch-up. That cap is the combined total across all of your IRAs, not per account. You have until the tax filing deadline in April 2027 to make your 2026 contribution, and whether you can use a Roth or deduct a traditional contribution depends on your income.

Below is exactly how much you can contribute for the 2026 tax year, the income phase-out ranges that decide your options, the deadline, how spousal IRAs work, and what to do if you accidentally put in too much.

2026 IRA contribution limits at a glance

For the 2026 tax year, the IRS raised the base IRA limit from $7,000 to $7,500. The catch-up contribution for savers age 50 and older also increased for the first time in years, moving from $1,000 to $1,100 (it is now indexed to inflation under the SECURE 2.0 Act). Add the two together and older savers can contribute $8,600.

| Who you are | Base limit | Catch-up (50+) | Total 2026 limit |

|---|---|---|---|

| Under age 50 | $7,500 | None | $7,500 |

| Age 50 or older | $7,500 | $1,100 | $8,600 |

A few rules that trip people up:

- It is a shared limit. If you have both a traditional and a Roth IRA, the $7,500 (or $8,600) applies to the two combined. You cannot put $7,500 in each.

- You need earned income. You can only contribute up to the amount of taxable compensation you earned during the year, such as wages, salary, or self-employment income. Investment income and Social Security do not count.

- There is no age ceiling. As long as you have earned income, you can contribute to a traditional or Roth IRA at any age.

- The catch-up starts at 50. You qualify for the extra $1,100 in any year you turn 50 or older, even if your birthday is in December.

Traditional vs Roth IRA: income limits decide your options

Both account types share the same contribution cap, but your income determines what you are actually allowed to do. Two different sets of rules are at play, and it is easy to mix them up.

- Roth IRA: your income can make you ineligible to contribute at all.

- Traditional IRA: anyone with earned income can contribute, but your income (and whether you have a workplace plan like a 401(k)) decides whether the contribution is tax-deductible.

Roth IRA income phase-outs for 2026

Roth contributions are made with after-tax money and grow tax-free. But high earners get phased out. If your modified adjusted gross income (MAGI) lands inside the range below, your allowed contribution shrinks; above the top number, you cannot contribute directly at all.

Traditional IRA deduction phase-outs for 2026

Anyone can contribute to a traditional IRA, but the deduction phases out only if you (or your spouse) are covered by a workplace retirement plan. If neither of you has a workplace plan, you can deduct the full contribution no matter how much you earn.

| Filing status | Roth IRA (eligibility) | Traditional IRA (deduction, if covered by a work plan) |

|---|---|---|

| Single / head of household | $153,000 – $168,000 | $81,000 – $91,000 |

| Married filing jointly (you are covered) | $242,000 – $252,000 | $129,000 – $149,000 |

| Married filing jointly (spouse covered, you are not) | $242,000 – $252,000 | $242,000 – $252,000 |

| Married filing separately | $0 – $10,000 | $0 – $10,000 |

How to read the ranges: below the bottom number you get the full benefit, inside the range you get a partial benefit, and above the top number you get none. For example, a single filer earning $160,000 in 2026 falls inside the Roth range and can make a reduced Roth contribution, while someone earning $170,000 is shut out of direct Roth contributions.

If you are over the Roth limit, a common workaround is the “backdoor Roth,” where you make a nondeductible traditional IRA contribution and then convert it to a Roth. It is legal and widely used, but the tax math gets complicated if you already hold pre-tax IRA money, so it is worth reading up before you try it. New to these accounts? Start with our Roth IRA guide for beginners.

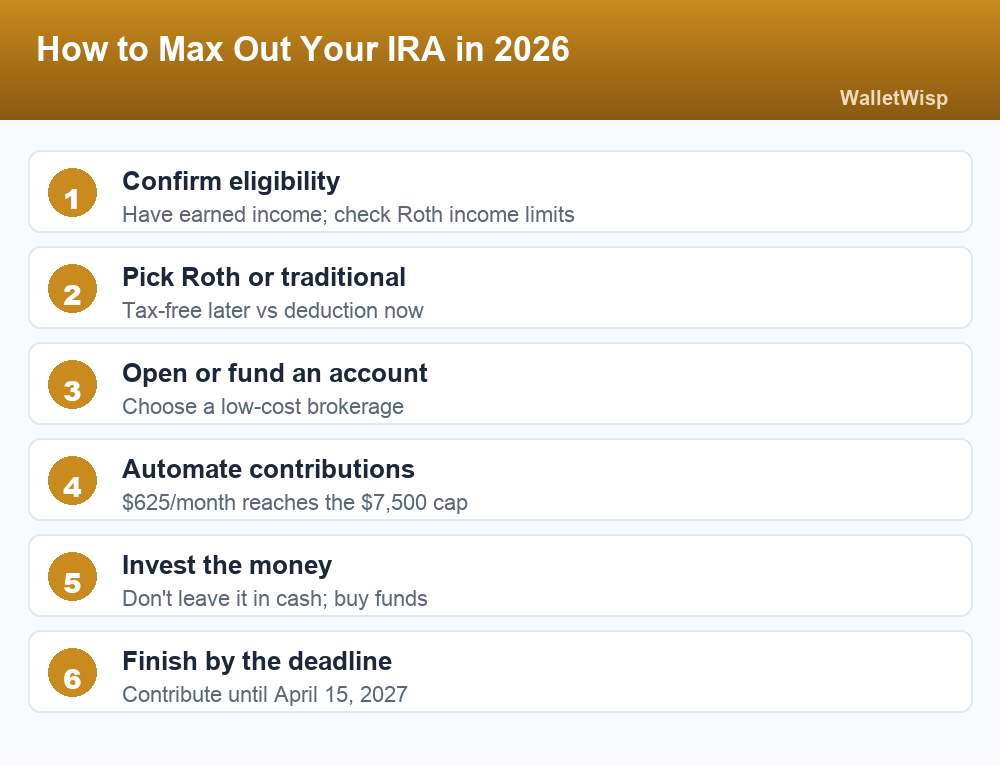

How to max out your IRA in 2026

Hitting the full $7,500 is more achievable when you break it into steps and automate it. Here is a straightforward path.

- Confirm you are eligible. Make sure you have earned income and check your MAGI against the Roth table above.

- Choose Roth or traditional. Roth means no deduction now but tax-free withdrawals later; traditional may cut this year’s tax bill.

- Open or fund an account. Any major low-cost brokerage offers free IRA accounts with no minimums.

- Automate the contributions. About $625 a month reaches the $7,500 cap by year-end without a lump-sum scramble.

- Actually invest the money. Contributing is only step one; the cash sits idle until you buy funds or ETFs inside the IRA.

- Finish by the deadline. You can keep contributing for the 2026 tax year until April 15, 2027.

If you cannot max it out, contribute what you can. Even a few hundred dollars invested for decades compounds meaningfully, and partial contributions still count.

The 2026 IRA contribution deadline

You do not have to fund your 2026 IRA by December 31, 2026. IRA contributions for a tax year can be made right up to the federal tax filing deadline for that year, which is April 15, 2027 for the 2026 tax year. A filing extension does not extend the IRA deadline; it stays at April 15 regardless.

This overlap window matters. Between January 1 and April 15, 2027, you can contribute for either 2026 or 2027, so be sure to tell your brokerage which tax year you mean when you make the deposit. Front-loading early in the year gives your money more time to grow, but funding at the deadline is still far better than skipping the year.

Spousal IRA: contribute for a non-working spouse

Normally you need your own earned income to fund an IRA, but a spousal IRA is the exception. If you file a joint return and one spouse has little or no income, the working spouse can fund an IRA in the non-working spouse’s name, as long as the couple’s combined earned income is at least equal to the total contributed.

Each spouse gets their own limit, so in 2026 a married couple can contribute:

- Up to $15,000 if both spouses are under 50 ($7,500 each).

- Up to $17,200 if both spouses are 50 or older ($8,600 each).

The account belongs to the spouse whose name is on it, and the same Roth income phase-outs apply based on your joint MAGI. Spousal IRAs are one of the simplest ways for single-income households to double their tax-advantaged saving.

What happens if you over-contribute

Putting in more than your limit, or contributing to a Roth when your income is too high, triggers a 6% excise tax on the excess amount for every year it stays in the account. The good news is the fix is usually easy if you act in time.

You have three ways to correct an excess contribution:

- Withdraw it in time. Remove the excess plus any earnings it generated before your tax filing deadline (including extensions) to avoid the 6% penalty. You will owe tax on the earnings, but not the penalty.

- Recharacterize it. Move an ineligible Roth contribution to a traditional IRA (or vice versa) so it lands in an account you qualify for.

- Apply it to a future year. Leave the money in and count it toward next year’s limit, though you pay the 6% for each year it was in excess.

The most common cause of accidental Roth over-contributions is a bonus, raise, or investment gain that pushes your income past the phase-out after you already contributed. If that happens, contact your brokerage; they handle “excess contribution removal” routinely.

Where an IRA fits in your bigger plan

An IRA is powerful, but it is one piece of a larger picture. A common order of priority looks like this: capture any 401(k) employer match first (free money), then decide between maxing an IRA and contributing more to your workplace plan. If you have a high-deductible health plan, an HSA offers a triple tax advantage that can even outrank an IRA for some savers.

And keep your short-term cash separate from retirement money. Your emergency fund belongs somewhere safe and liquid, not in an IRA; parking it in one of the best high-yield savings accounts keeps it accessible while still earning interest. IRAs are for long-term money you will not touch until retirement, since early withdrawals of earnings can trigger taxes and a 10% penalty before age 59½.

Frequently Asked Questions

What is the IRA contribution limit for 2026?

The 2026 IRA contribution limit is $7,500 if you are under 50 and $8,600 if you are 50 or older, which includes an $1,100 catch-up contribution. That total is combined across all your traditional and Roth IRAs.

Can I contribute to both a traditional and a Roth IRA in 2026?

Yes, but the $7,500 (or $8,600) limit applies to the two accounts combined, not each separately. You could put $4,000 in a Roth and $3,500 in a traditional, for example, but not $7,500 in each.

What is the deadline to contribute to a 2026 IRA?

You can make 2026 IRA contributions until the federal tax filing deadline of April 15, 2027. A tax-filing extension does not push back this date, and you should specify the tax year when contributing between January and April.

What are the 2026 Roth IRA income limits?

For 2026, Roth eligibility phases out between $153,000 and $168,000 for single filers and between $242,000 and $252,000 for married couples filing jointly. Above the top of your range, you cannot contribute directly to a Roth.

How much is the catch-up contribution for 2026?

The IRA catch-up contribution for savers age 50 and older is $1,100 in 2026, up from $1,000. It is now indexed to inflation, so it may rise again in future years. Adding it to the base limit brings your total to $8,600.

Can I contribute to an IRA if I do not have a job?

You generally need earned income such as wages or self-employment income to contribute. The exception is a spousal IRA: if you file jointly and your spouse has enough earned income, they can fund an IRA in your name.

What happens if I contribute too much to my IRA?

Excess contributions face a 6% excise tax for each year they remain in the account. You can avoid the penalty by withdrawing the excess plus earnings before your tax deadline, recharacterizing it, or applying it to a future year.

Is a traditional IRA contribution tax-deductible in 2026?

Anyone with earned income can contribute to a traditional IRA, but the deduction phases out if you or your spouse are covered by a workplace plan. If neither of you has one, your full contribution is deductible regardless of income.

")

{kind=link}