The Robinhood Gold Card is a no-annual-fee metal rewards card that pays a flat 3% cash back on every purchase and 5% on travel booked through the Robinhood travel portal — provided you keep a Robinhood Gold membership ($5/month or $50/year). Its standout trick is letting you sweep that cash back straight into your Robinhood brokerage to buy stocks, ETFs, or crypto. For heavy spenders who already pay for Gold, it is one of the most rewarding flat-rate cards available in 2026; for light spenders, the subscription can quietly eat the rewards.

Below is a full breakdown of how the rewards work, the true cost of the Gold requirement, the credit you need for approval, and how the Robinhood Gold Card stacks up against the Apple Card so you can decide if it belongs in your wallet.

Robinhood Gold Card at a glance

The card is issued on the Visa Signature network and is aimed squarely at Robinhood’s existing Gold subscribers. There is no fee for the card itself — the cost is bundled into the Gold membership you were likely already paying for other perks like higher cash APY and an IRA match. Here are the core details as of 2026 (rates and terms are typical figures and can change, so confirm the current offer before applying).

| Feature | Detail |

|---|---|

| Cash back on everything | 3% (unlimited on most spend) |

| Travel via Robinhood portal | 5% cash back |

| Annual card fee | $0 |

| Required membership | Robinhood Gold — $5/month or $50/year |

| Card material | Stainless steel (metal), ~17g |

| Network / issuer | Visa Signature, issued via Coastal Community Bank |

| Foreign transaction fee | $0 (estimated — none advertised) |

| Cash back redemption | Statement credit, spending account, or auto-invest into brokerage |

| Credit needed | Good to excellent (est. 690+) |

| Extra cards | Add family members / authorized users (up to 5) |

How the rewards actually work

3% cash back on everything

Most cash-back cards pay 1–2% on general spend and reserve their higher rates for narrow categories like groceries or gas. The Robinhood Gold Card flips that model: it pays a flat 3% on every purchase, with no categories to track and no rotating calendars. Groceries, gas, dining, streaming, insurance, utilities — all earn the same 3%. That flat rate is the card’s single biggest selling point and is unusually generous for a product with no separate annual card fee.

One caveat: extremely high monthly spend may be reviewed, and Robinhood reserves the right to adjust earning for outlier accounts, so treat “unlimited” as generous but not literally boundless. For normal household budgets, though, the 3% applies cleanly.

5% on travel booked through the Robinhood portal

Book flights, hotels, or rental cars through the Robinhood travel portal and the rate jumps to 5% cash back. This works like the travel portals from Chase or Capital One: you shop inside Robinhood’s booking tool, pay with the card, and the elevated rate posts automatically. The trade-off is the usual one — portal inventory and pricing may not always match booking direct, so compare the total cost before you trade flexibility for the extra 2%.

Invest your cash back automatically

This is the feature that sets the Robinhood Gold Card apart from every mainstream cash-back card. Instead of a statement credit that vanishes into your balance, you can route rewards into your Robinhood brokerage or retirement account and auto-invest them into stocks, ETFs, or crypto. Turn on the setting and every dollar of cash back is put to work. Over years, reinvested rewards compounding in the market can meaningfully outgrow the same dollars taken as a plain credit — a genuine differentiator for buy-and-hold investors.

The Robinhood Gold requirement — the real cost

The card advertises “no annual fee,” and that is technically true of the card. But you cannot hold it without an active Robinhood Gold subscription, which runs $5 per month or $50 per year. That is the real cost of entry, so factor it into any rewards math.

The good news is that Gold bundles far more than card access. Depending on current terms, membership typically includes an elevated APY on uninvested brokerage cash, a matching bonus on IRA contributions, larger instant deposits, Level II market data, and lower margin rates. If you already pay for Gold for those reasons, the card’s rewards are effectively “free” 3% on top. If you would only subscribe for the card, do the break-even first.

The math is simple. Versus a solid no-fee 2% card, the Gold Card’s extra 1% needs to cover the $50 annual Gold fee. That means you need roughly $5,000 of annual spend just to break even on the subscription — before Gold’s other perks are counted. Spend $20,000 a year and the extra 1% is worth about $200, comfortably clearing the fee. Spend $2,000 a year and a free 2% card likely wins.

The metal card and other perks

The Robinhood Gold Card ships as a weighty stainless-steel card — a premium touch usually reserved for cards with triple-digit annual fees. Beyond looks, useful practical perks include the ability to add family members or authorized users (reportedly up to five cards), Visa Signature benefits, and app-native controls for freezing the card, viewing virtual card numbers, and tracking rewards in real time. There is no separate foreign transaction fee advertised, which makes it reasonable for travel abroad when paired with the 3% base rate.

Approval and credit — what you need

Getting the card is a two-step gate. First, you generally need to be a Robinhood Gold member and, historically, come off a waitlist as the company scaled the rollout. Second, approval involves a real credit check. Robinhood does not publish a hard cutoff, but a good-to-excellent score (roughly 690 and up) gives you the best odds, consistent with other premium flat-rate cards.

If your score is not there yet, it is worth a short runway before applying. Paying down revolving balances, avoiding new hard pulls, and correcting report errors can move the needle in a few statement cycles — our guide on how to improve your credit score in 2026 walks through the fastest levers. It is also worth knowing that some “buy now, pay later” activity is starting to appear on credit files, so if you use those plans, read how BNPL affects your credit score before you apply for any new card.

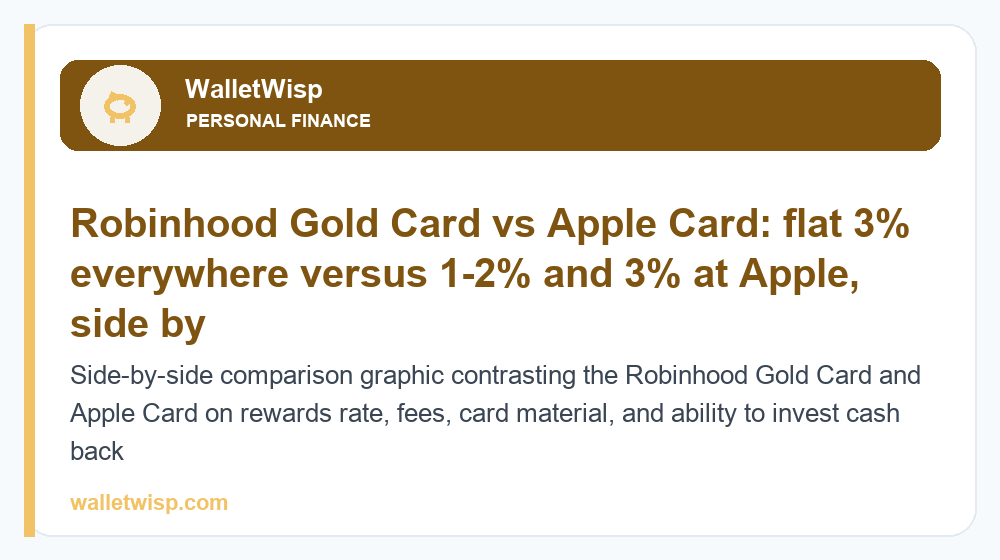

Robinhood Gold Card vs Apple Card

The Apple Card is the most natural comparison: both are no-annual-fee, tech-company cards with metal designs and slick app experiences. But their reward structures are very different. The Apple Card pays 3% only at Apple and a rotating list of partner merchants, 2% when you pay with Apple Pay, and just 1% on the physical titanium card. The Robinhood Gold Card pays a flat 3% everywhere — no Apple Pay requirement — but locks that rate behind the Gold subscription.

| Feature | Robinhood Gold Card | Apple Card |

|---|---|---|

| Base rewards rate | 3% on everything | 1% physical card / 2% Apple Pay |

| Top rate | 5% travel (portal) | 3% at Apple & select partners |

| Card fee / requirement | $50/yr Gold membership | No fee, no subscription |

| Card material | Stainless steel | Titanium |

| Invest cash back | Yes — into brokerage/crypto | Into a savings account (no investing) |

| Foreign transaction fee | $0 (estimated) | $0 |

| Network | Visa Signature | Mastercard |

| Best for | Investors / high spenders on Gold | Apple ecosystem, no-fee simplicity |

Bottom line: for everyday spending outside the Apple ecosystem, the Robinhood Gold Card’s flat 3% simply out-earns the Apple Card — as long as your spending clears the $50 Gold hurdle. If you want zero subscriptions and mostly buy Apple products or pay with Apple Pay, the Apple Card is the lower-commitment pick.

Pros and cons

Pros

- Flat 3% cash back on all purchases with no categories to manage

- 5% on travel booked through the Robinhood portal

- Cash back can be auto-invested into stocks, ETFs, or crypto

- No separate annual card fee and a premium metal design

- No foreign transaction fee (estimated) for spending abroad

- Family/authorized-user cards available

Cons

- Requires a paid Robinhood Gold membership ($5/mo or $50/yr)

- Light spenders may not clear the ~$5,000 break-even vs a free 2% card

- 5% travel rate is tied to Robinhood’s portal, not open booking

- Historically gated behind a waitlist and a credit check

- Ecosystem lock-in — value is highest only if you use Robinhood investing

Who the Robinhood Gold Card is worth it for

The card makes the most sense for three groups. First, existing Robinhood Gold members who are already paying $50/year for the APY, IRA match, or trading perks — for them the 3% is nearly free money. Second, higher spenders (roughly $15,000+ a year) who will easily out-earn the subscription cost even without Gold’s other benefits. Third, hands-off investors who love the idea of turning routine spending into automatically invested dollars that compound over time.

It is a weaker fit for light spenders, people who do not use Robinhood for investing, or anyone who wants to avoid subscriptions entirely — a free flat 2% card is simpler and cheaper for them. And regardless of which card you choose, keep chasing the easy wins elsewhere: rotating your idle cash into a high-yield account or grabbing a sign-up offer from our roundup of the best bank account bonuses this month can add more to your bottom line than an extra 1% of card rewards.

Frequently Asked Questions

Does the Robinhood Gold Card have an annual fee?

No, the card itself has no annual fee. However, you must maintain an active Robinhood Gold subscription to hold it, which costs $5 per month or $50 per year, so that is the effective cost of ownership.

How much cash back does the Robinhood Gold Card earn?

It earns a flat 3% cash back on essentially all purchases and 5% on travel booked through the Robinhood travel portal. There are no bonus categories to track — the 3% applies to everyday spending across the board.

Can I really invest my cash back?

Yes. You can route your cash back into your Robinhood brokerage or retirement account and auto-invest it into stocks, ETFs, or crypto, rather than taking it as a statement credit. This is the card’s signature feature for long-term investors.

What credit score do I need to be approved?

Robinhood does not publish a hard cutoff, but a good-to-excellent score (roughly 690 or higher) gives you the strongest approval odds. Approval involves a credit check, so it is worth cleaning up your report before applying.

Is the Robinhood Gold Card a metal card?

Yes. It is a stainless-steel metal card weighing around 17 grams — a premium touch normally found on cards that charge triple-digit annual fees, offered here with only the Gold membership requirement.

Robinhood Gold Card vs Apple Card — which is better?

For general spending, the Robinhood Gold Card’s flat 3% beats the Apple Card’s 1–2% (3% only at Apple and partners), provided your spending clears the $50 Gold fee. The Apple Card wins if you want no subscription and live inside the Apple ecosystem.

Is there a foreign transaction fee?

No foreign transaction fee is advertised, which — combined with the flat 3% back — makes it a reasonable card to use abroad. Always confirm the current terms in the app before international travel, as fees and rates can change.

Is the Robinhood Gold Card worth it in 2026?

It is worth it if you already pay for Robinhood Gold, spend enough to clear the roughly $5,000 annual break-even versus a free 2% card, or want to auto-invest your rewards. For light spenders or non-Robinhood users, a no-fee flat-rate card is usually the better value.

")

{kind=link}