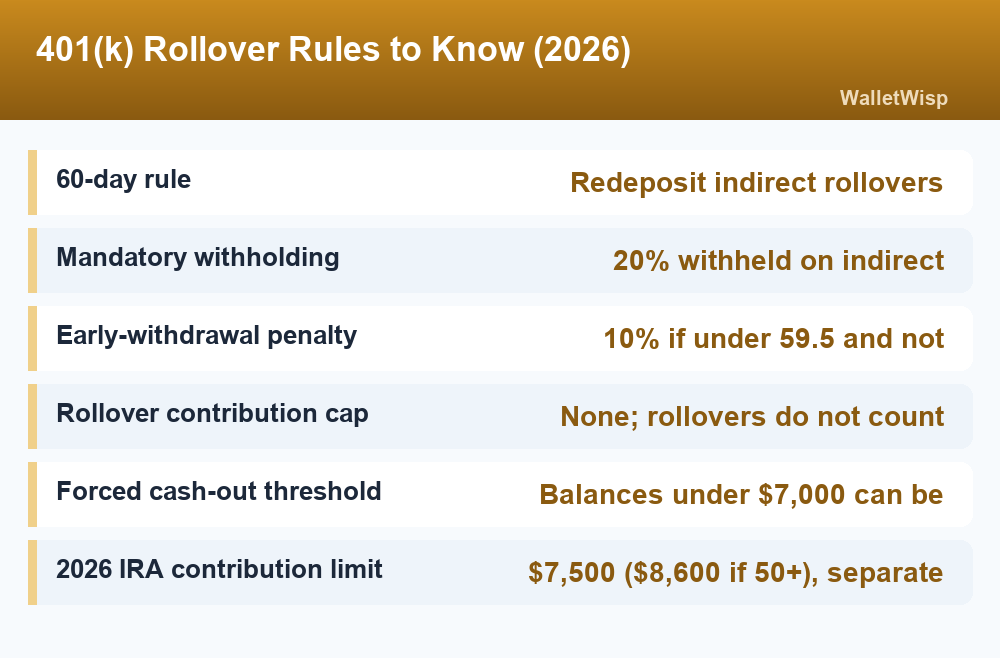

A 401k rollover moves the money from an old employer’s retirement plan into an IRA or a new employer’s 401(k) without triggering taxes, as long as you do it the right way. The safe method is a direct rollover, where your old plan sends the money straight to the new account and nothing is withheld or taxed. The route to avoid is the indirect rollover, where the plan mails a check to you: it must withhold 20% up front, and you then have only 60 days to redeposit the full amount or the IRS treats the shortfall as a taxable, possibly penalized, withdrawal.

This guide walks through every step of rolling an old 401(k) into an IRA in 2026, explains when a new 401(k) makes more sense, and shows exactly how to dodge the withholding and penalty traps that catch people who change jobs.

What a 401(k) rollover actually does

When you leave a job, your old 401(k) does not disappear. The account stays invested, but you lose the ability to make new contributions and you may face higher fees or a limited menu of funds. A rollover simply relocates that balance into an account you control, keeping its tax-deferred (or Roth) status intact.

The key thing to understand is that a properly executed rollover is not a withdrawal. You are not spending the money or cashing out. You are moving it from one qualified retirement account to another, which the tax code allows without any tax bill. Rollover dollars also do not count against your annual contribution limits, so moving a $150,000 balance does not use up any of your 2026 IRA or 401(k) contribution room.

You generally have four choices for an old 401(k):

- Leave it in the old plan. Allowed if the balance is above $7,000. Simple, but you keep the old plan’s fees and fund choices and add another account to track.

- Roll it into your new employer’s 401(k). Keeps everything in one workplace plan and preserves some 401(k)-only benefits.

- Roll it into an IRA. The most flexible option, with the widest investment selection and often lower costs.

- Cash it out. Almost always the worst choice. You owe income tax plus a 10% penalty if you are under 59 and a half.

Note the $7,000 threshold: under current rules, if your balance is below that amount your former employer can force you out of the plan, either cutting you a check or automatically rolling the money into an IRA on your behalf. If you get a letter about a small balance, act before the plan decides for you.

Direct vs. indirect rollover: the difference that saves you thousands

How the money physically moves is the single most important decision in a 401k rollover. There are two methods, and they carry very different levels of risk.

A direct rollover (also called a trustee-to-trustee transfer) sends the funds straight from your old plan to the new IRA or 401(k). The check is made payable to the new custodian, not to you, so no tax is withheld and no 60-day clock ever starts. An indirect rollover pays the money to you first. Your old plan is required by law to withhold 20% for taxes, and you must deposit the entire original balance into a new account within 60 days.

| Feature | Direct rollover | Indirect rollover |

|---|---|---|

| How the money moves | Plan sends funds straight to the new account | Plan pays a check to you first |

| Mandatory withholding | None (0%) | 20% withheld from a 401(k) payout |

| Deadline to complete | No 60-day clock | 60 calendar days to redeposit |

| Tax if done correctly | $0 | $0, but only if you replace the withheld 20% |

| Once-per-year limit | Not applicable | Only restricts IRA-to-IRA moves, not 401(k)-to-IRA |

| Risk level | Low | High |

The 20% withholding trap, with numbers

Say you have $100,000 in an old 401(k) and choose an indirect rollover. Your plan sends you a check for $80,000 and forwards $20,000 to the IRS as withholding. To complete a fully tax-free rollover, you must deposit the entire $100,000 into your new IRA within 60 days, which means covering that missing $20,000 out of your own pocket. You get the $20,000 back later as a tax refund, but only if you had the cash to replace it now.

If you can only deposit the $80,000 you received, the IRS treats the remaining $20,000 as a distribution. That $20,000 becomes taxable income for the year, and if you are under 59 and a half, it also gets hit with a 10% early-withdrawal penalty of $2,000. The lesson is simple: always ask for a direct rollover and let the money move institution to institution.

Rollover to an IRA vs. a new employer 401(k)

Once you have decided to roll over rather than cash out, the next question is where the money should land. Both destinations preserve the tax treatment, but they suit different situations.

Rolling into an IRA usually gives you the most control:

- A far wider menu of investments: individual stocks, ETFs, index funds, and bonds instead of a short list of plan options.

- Often lower expense ratios and account fees, especially at low-cost brokerages.

- Easier consolidation if you have several old 401(k)s from past jobs.

- The ability to do Roth conversions on your own timetable.

Rolling into your new 401(k) can be the better move when:

- You value simplicity and want a single workplace account.

- You may want to use the “rule of 55,” which lets you take penalty-free withdrawals from a 401(k) at the job you leave at age 55 or later. IRAs do not offer this.

- You want stronger federal creditor protection, which employer plans generally provide.

- You plan to use the backdoor Roth strategy, since a pre-tax IRA balance can complicate the pro-rata tax calculation. Keeping pre-tax money in a 401(k) sidesteps that.

For most people who have left a job and want flexibility and lower costs, an IRA wins. If you are weighing the account types themselves, our guide to traditional vs. Roth IRAs in 2026 breaks down which one fits your tax situation.

How to roll over a 401(k) to an IRA, step by step

The process is more paperwork than difficulty. Here is the full sequence.

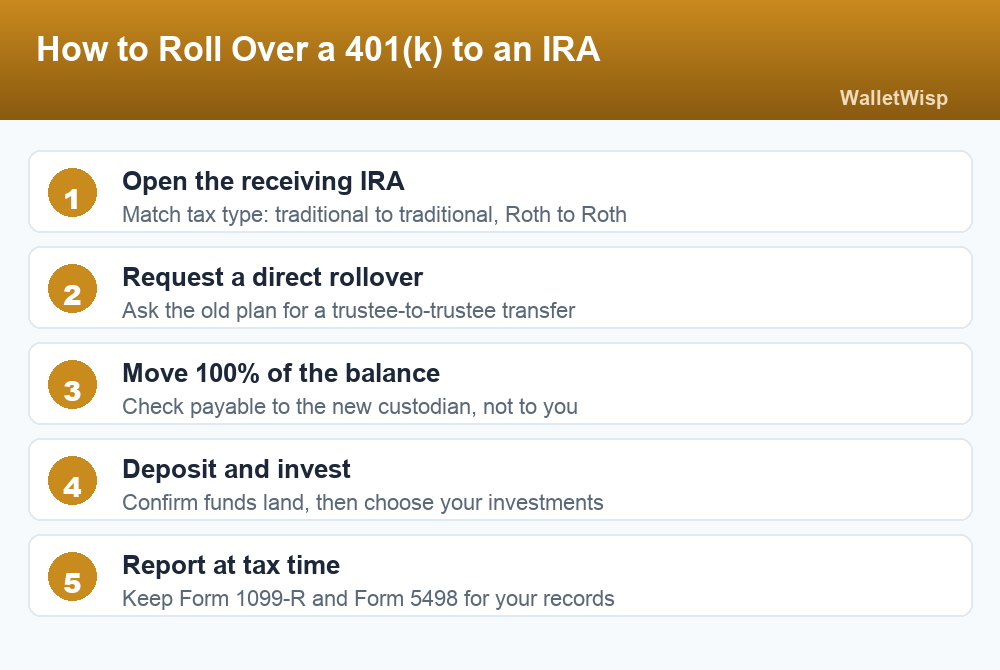

1. Open the receiving IRA first

Set up an IRA at a brokerage before you touch the old plan. Match the tax type: a traditional 401(k) rolls into a traditional IRA, and a Roth 401(k) rolls into a Roth IRA. If you are new to these accounts, our Roth IRA guide for beginners covers how to open and fund one.

2. Call your old plan and request a direct rollover

Contact the 401(k) administrator (the phone number is on your statements) and specifically ask for a direct or trustee-to-trustee rollover. Give them the new IRA account number and the custodian’s name. Insist the check be made payable to the custodian for your benefit, not to you personally.

3. Choose 100% of the balance and confirm the destination

Elect to move the entire balance unless you have a specific reason not to. Double-check the mailing or wiring instructions so the funds cannot be misrouted and accidentally become a taxable payout.

4. Deposit the funds and invest them

Rolled-over cash often arrives as an uninvested balance. It will sit in cash earning little until you actually buy investments, so once the money lands, choose your funds and put it to work.

5. Report the rollover at tax time

Early the following year you will receive Form 1099-R from the old plan and Form 5498 from the new custodian. A correctly done direct rollover is reported on your return but is not taxed. Keep both forms with your records.

Most direct rollovers finish within two to four weeks. If a check is mailed to your new custodian, the process can take a little longer, but you are still protected as long as it is payable to the custodian rather than to you.

Traditional or Roth? Rollover tax treatment

Whether a rollover is tax-free depends on the tax character of the account you are leaving and the one you are moving into. Matching pre-tax to pre-tax, and Roth to Roth, keeps the move tax-free. Mixing them can create a taxable event.

| From account | To account | Taxed now? |

|---|---|---|

| Traditional 401(k) | Traditional IRA | No |

| Traditional 401(k) | New employer 401(k) | No |

| Roth 401(k) | Roth IRA | No |

| Traditional 401(k) | Roth IRA | Yes, counts as a Roth conversion |

| After-tax 401(k) | Roth IRA | No, though any earnings portion is taxed |

A note on Roth conversions

Moving a traditional (pre-tax) 401(k) directly into a Roth IRA is not just a rollover, it is a Roth conversion. The entire converted amount is added to your taxable income for the year, but from then on the money grows and can be withdrawn tax-free in retirement. This can be a smart play in a low-income year, such as a gap between jobs, when the tax hit is smaller. Just make sure you can pay the resulting tax bill from outside the retirement account, since using the retirement money itself to cover the tax defeats the purpose and can add penalties.

Remember that a rollover moves your existing balance and does not touch your annual contribution room. You can still make a fresh 2026 IRA contribution on top of a rollover, up to the yearly cap. See our breakdown of 2026 IRA contribution limits for the exact figures.

How to avoid taxes and penalties

Nearly every rollover mistake falls into a handful of buckets. Steer clear of these and your 401k rollover will be completely tax-free:

- Always choose a direct rollover. It eliminates the 20% withholding and the 60-day deadline in one move.

- Never let the check be payable to you. If it is made out to your IRA custodian “for benefit of” you, it is a direct rollover even if it passes through your mailbox.

- If you are stuck with an indirect rollover, replace the withheld 20%. Deposit the full original balance within 60 days and reclaim the withholding as a refund later.

- Match the tax type. Pre-tax to pre-tax, Roth to Roth, unless you deliberately want a taxable conversion.

- Do not cash out to “hold” the money. A withdrawal before 59 and a half triggers income tax plus a 10% penalty, and you permanently lose that retirement growth.

- Watch for company stock. If your 401(k) holds employer shares that have appreciated a lot, a special rule called net unrealized appreciation may lower your tax bill. Talk to a tax pro before rolling those shares over.

- Do not procrastinate on a small balance. Sub-$7,000 accounts can be forced out by the old plan, so handle them before that happens.

Handled correctly, a rollover costs you nothing in taxes and keeps decades of compounding on track. The paperwork takes an afternoon; getting it wrong can cost thousands. When in doubt, pick the direct route and confirm the check is never payable to you.

Frequently Asked Questions

How long do I have to roll over my 401(k)?

With a direct rollover there is no deadline, because the money never comes to you. With an indirect rollover, where you receive the funds, you have 60 calendar days from the date you get the check to redeposit the full amount into a new retirement account.

Will a 401(k) rollover be taxed?

A direct rollover between accounts of the same tax type, such as a traditional 401(k) to a traditional IRA, is not taxed at all. You only owe tax if you convert pre-tax money to a Roth account or fail to complete an indirect rollover within 60 days.

What is the 20% withholding on a 401(k) rollover?

If you take an indirect rollover, your old plan must legally withhold 20% of the distribution for federal taxes. To avoid tax, you have to deposit the entire original balance, including that withheld 20%, within 60 days and recover the withholding as a refund later. A direct rollover avoids the withholding entirely.

Can I roll over my 401(k) while still employed?

Usually not, unless you are 59 and a half or older, in which case many plans allow an in-service rollover. Otherwise you generally must leave the job before you can roll over that employer’s plan.

Does a rollover count toward my IRA contribution limit?

No. Rollover dollars are not contributions, so they do not count against your annual IRA limit. You can roll over any amount and still make your full separate 2026 contribution on top of it.

Can I roll a traditional 401(k) into a Roth IRA?

Yes, but it counts as a Roth conversion. The full amount you move is added to your taxable income for the year. In exchange, that money then grows and can be withdrawn tax-free in retirement, which can be worthwhile in a lower-income year.

What happens if I miss the 60-day deadline?

The distribution becomes taxable income for the year, and if you are under 59 and a half, it also faces a 10% early-withdrawal penalty. The IRS grants waivers only in limited hardship situations, so the direct rollover method is far safer.

Should I roll over my 401(k) or leave it where it is?

Rolling into an IRA usually gives you lower fees and more investment choices, while a new 401(k) offers simplicity and certain protections like the rule of 55. Leaving it in the old plan is fine if the fees are low, but consolidating makes your retirement money easier to manage.

")

{kind=link}