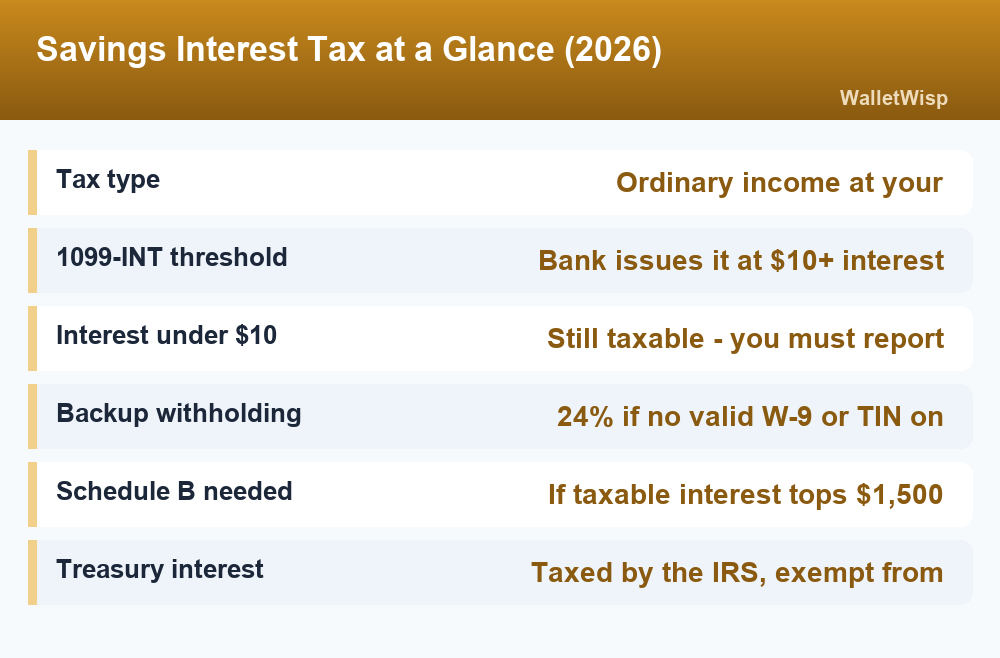

Savings account interest is taxed as ordinary income in the year you earn it, at the same marginal tax rate that applies to your paycheck. Your bank reports it to you and the IRS on Form 1099-INT once you earn $10 or more, but you owe tax on every dollar of interest even if you earn less than that and never receive a form. There is no special low rate for interest the way there is for long-term capital gains or qualified dividends.

That single rule covers high-yield savings accounts, money market accounts, and certificates of deposit. Treasuries, I bonds, and municipal bonds follow slightly different rules, which we cover below. Here is exactly how it works in 2026, what you owe at each income level, and the legitimate ways to keep more of your interest.

How savings account interest is taxed

Interest is treated as ordinary income, so it stacks on top of your wages and is taxed at your top marginal bracket. If you are in the 22% bracket and earn $400 of interest, you owe roughly $88 in federal tax on it. The money is taxed in the year it is credited to your account, not the year you withdraw it, so leaving interest sitting in the account does not delay the tax bill.

Interest is taxable in the year the bank posts it to your account, even if you never touch it. A few key points:

- It is fully taxable at the federal level. Regular savings, high-yield savings, money market accounts, and CDs all count.

- Most states tax it too. If your state has an income tax, your bank interest is generally taxable there as well. Only the handful of states with no income tax skip it.

- There is no minimum “free” amount. The $10 threshold only controls whether the bank mails a form, not whether the income is taxable.

- Bonuses count as interest. Account-opening bonuses are usually reported in Box 1 of your 1099-INT and taxed like any other interest.

Chasing a top rate on a high-yield savings account is still worth it even after tax. A 4% APY taxed at 22% still leaves you with an after-tax yield above 3%, which beats leaving cash in a checking account earning nothing.

When you get a 1099-INT (and what if you earn under $10)

Banks and credit unions must send you Form 1099-INT by January 31 if you earned $10 or more in interest during the prior year. You will also see it in your online banking tax-documents section. The most important boxes are:

- Box 1 – Interest income from savings, CDs, and money market accounts.

- Box 2 – Early withdrawal penalty (this is deductible – see the CD section).

- Box 3 – Interest on U.S. Savings Bonds and Treasury obligations (federally taxable, state-exempt).

- Box 4 – Federal income tax withheld through backup withholding.

- Box 8 – Tax-exempt interest, such as from municipal bonds.

If you earned less than $10, you usually will not get a form – but the interest is still taxable and you are still required to report it. Add up the small amounts from your year-end statements and include them. The IRS receives copies of all 1099-INTs and runs automated matching, so leaving off reported interest is a common trigger for a CP2000 notice.

2026 federal tax brackets: the rate on your interest

Because interest is ordinary income, the rate you pay is simply your marginal bracket. The 2026 federal income tax brackets (for income earned in 2026 and filed in early 2027) are below.

| Rate | Single | Married filing jointly |

|---|---|---|

| 10% | $0 – $12,400 | $0 – $24,800 |

| 12% | $12,400 – $50,400 | $24,800 – $100,800 |

| 22% | $50,400 – $105,700 | $100,800 – $211,400 |

| 24% | $105,700 – $201,775 | $211,400 – $403,550 |

| 32% | $201,775 – $256,225 | $403,550 – $512,450 |

| 35% | $256,225 – $640,600 | $512,450 – $768,700 |

| 37% | Over $640,600 | Over $768,700 |

The 2026 standard deduction is $16,100 for single filers, $32,200 for married couples filing jointly, and $24,150 for heads of household. Your interest is taxed at the rate for the bracket your last dollar of income falls into.

Marginal-rate examples

Say you keep $10,000 in a savings account earning 4% APY. That is about $400 of interest for the year. Your federal tax on that $400 depends only on your bracket:

- 12% bracket: about $48 in tax, leaving $352.

- 22% bracket: about $88 in tax, leaving $312.

- 24% bracket: about $96 in tax, leaving $304.

- 32% bracket: about $128 in tax, leaving $272.

Scale that up and the tax matters more. On $50,000 of CDs paying 4.5% – roughly $2,250 of interest – a 24% filer owes about $540 in federal tax, plus state tax if applicable. Interest never pushes your entire income into a higher bracket; only the portion of income above each threshold is taxed at the higher rate.

When banks withhold tax on your interest (backup withholding)

Normally your bank pays you interest in full and you settle the tax when you file. But the bank must apply backup withholding at 24% and send it to the IRS if:

- You did not give the bank a correct Taxpayer Identification Number (usually your Social Security number) on a W-9.

- The IRS notified the bank that your reported name and TIN do not match.

- The IRS told the bank you underreported interest or dividends in the past.

Withheld amounts show up in Box 4 of your 1099-INT and count as a credit against your total tax bill, just like paycheck withholding – so you are not taxed twice. The fix for ongoing backup withholding is to give your bank an updated, correct W-9. Most people who keep their account information current never see backup withholding at all.

How CDs, Treasuries, and bonds are taxed

Not every interest-bearing account follows the plain savings-account rule. The table below summarizes the 2026 treatment, and the notes that follow explain the wrinkles.

| Account type | Federal tax | State/local tax | When taxed |

|---|---|---|---|

| Savings / HYSA / money market | Ordinary income | Taxable | Year credited |

| Certificate of deposit (CD) | Ordinary income | Taxable | Year credited, even if not withdrawn |

| Treasury bills, notes, bonds | Ordinary income | Exempt | Year credited (T-bills at maturity) |

| Series I / EE savings bonds | Ordinary income | Exempt | Deferred until redeemed (or maturity) |

| Municipal bonds | Exempt | Exempt if in-state | Reported but usually untaxed |

CDs

CD interest is taxed as it is credited, not when the CD matures. For a multi-year CD that compounds annually, you get a 1099-INT and owe tax each year, even though you cannot touch the money without a penalty. If you break a CD early, the early-withdrawal penalty appears in Box 2 and is deductible as an adjustment to income on Schedule 1 – you do not have to itemize to claim it. Spreading maturities to build a CD ladder can smooth out when that interest lands, but it does not change the fact that each year’s credited interest is taxable that year.

Treasuries

Interest from U.S. Treasury bills, notes, and bonds is subject to federal income tax but exempt from state and local income tax. That exemption is a real edge if you live in a high-tax state like California or New York – a Treasury paying the same headline rate as a CD can deliver a higher after-tax yield. For a Treasury bill, the “interest” is the difference between the discounted purchase price and the face value you receive at maturity, and it is taxed in the year the bill matures.

I bonds and EE savings bonds

Series I and EE savings bonds let you defer federal tax until you redeem the bond or it stops earning interest (up to 30 years), and the interest is always exempt from state and local tax. If you use the proceeds for qualified higher-education expenses and meet income limits, some or all of the interest may be federally tax-free under the education exclusion.

Municipal bonds

Interest from municipal bonds is generally exempt from federal income tax, and exempt from state tax too if you buy bonds issued in your own state. It still gets reported (Box 8 of the 1099-INT and line 2a of Form 1040), and it can affect how much of your Social Security is taxable, but you usually pay no tax on it. Munis mainly make sense for high earners in top brackets.

Ways to reduce the tax on your interest

You cannot make ordinary savings interest tax-free, but you can shift where your cash lives or use accounts that shelter the earnings.

- Use a Traditional or Roth IRA. Interest earned inside an IRA is not taxed each year. In a Roth IRA, qualified withdrawals come out completely tax-free. The 2026 IRA contribution limit is $7,500, plus a $1,100 catch-up if you are 50 or older.

- Max out an HSA. A health savings account (HSA) is the most tax-efficient place to hold interest-bearing cash: contributions are deductible, growth is untaxed, and withdrawals for medical costs are tax-free. The 2026 limits are $4,400 for self-only coverage and $8,750 for family coverage, plus $1,000 more if you are 55+.

- Hold Treasuries instead of CDs if you live in a high-tax state, to skip the state tax on the interest.

- Consider municipal bonds or muni money market funds if you are in the 32% bracket or higher and want federally tax-exempt income.

- Buy I bonds to defer the federal tax until you cash out, which can be years down the road.

Keeping only your emergency fund and short-term cash in a taxable savings account, while routing longer-term savings into tax-advantaged accounts, is the simplest way to shrink the annual interest tax.

Don’t forget state tax and the 3.8% surtax

If your state has an income tax, your bank and CD interest is generally taxable there at your state rate on top of the federal tax. And higher earners face an extra layer: the Net Investment Income Tax (NIIT) adds 3.8% on investment income, including interest, once your modified adjusted gross income tops $200,000 (single) or $250,000 (married filing jointly). Those thresholds are not adjusted for inflation, so more savers drift into NIIT territory over time.

One planning note: you generally owe estimated taxes if you expect to owe $1,000 or more when you file and withholding does not cover it. If a large CD or Treasury position throws off significant interest, consider making quarterly estimated payments to avoid an underpayment penalty.

Frequently Asked Questions

Do I have to report interest under $10 if I didn’t get a 1099-INT?

Yes. The $10 figure is only the point at which the bank is required to mail a form. All interest is taxable regardless of amount, so total up the small amounts from your statements and report them on your return.

What tax rate do I pay on savings account interest?

You pay your ordinary income tax rate – the same marginal bracket as your wages, ranging from 10% to 37% in 2026. There is no reduced rate for interest the way there is for long-term capital gains.

Is high-yield savings interest taxed differently than regular savings?

No. A high-yield savings account is taxed exactly like a standard savings account – as ordinary income. It simply generates more interest, so the dollar amount of tax is larger.

When do I pay tax on CD interest – each year or at maturity?

Each year, as the interest is credited. Even on a multi-year CD you cannot access early, you owe tax annually on the interest posted that year and will receive a 1099-INT for it.

Is Treasury or savings-bond interest taxed by my state?

No. Interest from U.S. Treasuries, I bonds, and EE savings bonds is exempt from state and local income tax, though it is still subject to federal tax. That state exemption can meaningfully boost your after-tax yield.

Do I need to file Schedule B for my interest?

You must file Schedule B with your Form 1040 if your total taxable interest (or ordinary dividends) exceeds $1,500 for the year. Below that, you report the total directly on line 2b of Form 1040.

Why did my bank withhold 24% of my interest?

That is backup withholding, usually triggered by a missing or incorrect Social Security number on file, or an IRS notice. It appears in Box 4 and counts as a credit against your tax bill. Update your W-9 with the bank to stop it.

How can I avoid paying tax on savings interest?

You cannot make taxable-account interest disappear, but you can earn interest inside tax-advantaged accounts like an IRA or HSA, use municipal bonds for federally exempt income, or hold Treasuries to avoid state tax. Cash held in a Roth IRA or HSA can grow with no annual interest tax at all.

")

{kind=link}