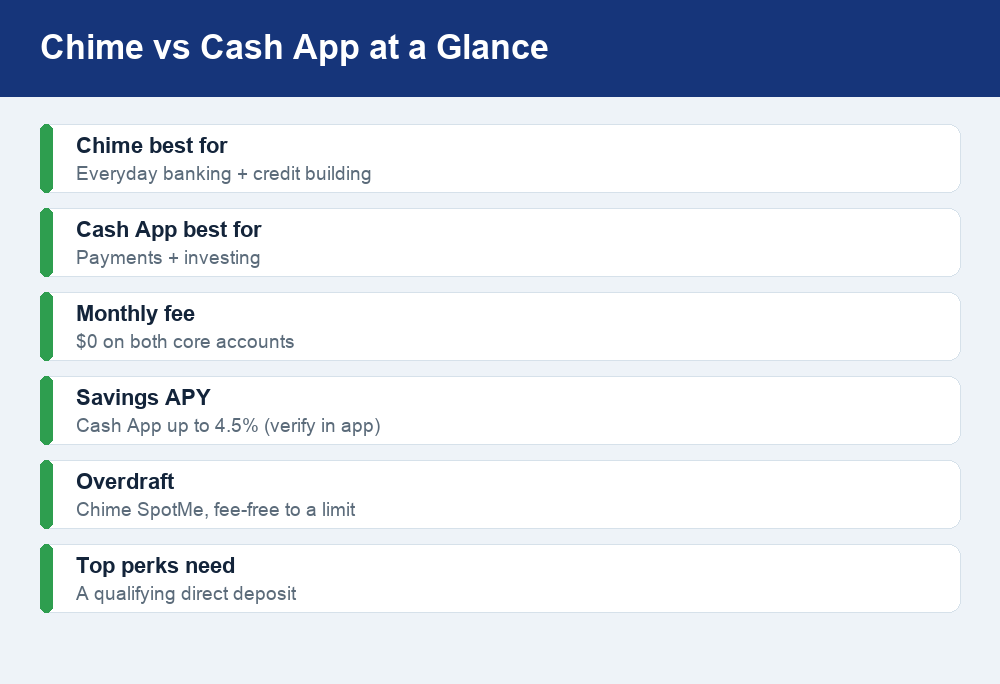

Chime and Cash App both live on your phone and both come with a debit card, but they are built for different jobs. Chime works best as a near-complete replacement for a traditional checking and savings account, with tools designed to help you avoid overdraft fees and build credit. Cash App is stronger as a payments and investing hub, where you can send money to friends, buy Bitcoin or stocks, and earn a competitive savings rate. The “better” app depends on whether you want a primary bank account or a flexible money tool that sits alongside one.

Quick answer: Choose Chime if you want a fee-friendly primary account with early direct deposit, fee-free overdraft coverage, and a secured card that helps build credit. Choose Cash App if your priority is sending and receiving money, investing in stocks or Bitcoin, and earning a higher savings rate. Both unlock their best features only after you set up a qualifying direct deposit, and both hold your cash at FDIC-insured partner banks rather than being banks themselves.

What Chime is (and isn’t)

Chime is a financial technology company, not a bank. It partners with FDIC-member banks to hold your money, which means eligible deposits are insured through those partners up to the standard federal limits. In everyday use, though, it feels like a full-service checking and savings account. You get a fee-free Checking Account, an optional Savings Account, a Visa debit card, and a large fee-free ATM network.

Where Chime stands out is the “avoid-fees, build-credit” toolkit. SpotMe lets eligible members overdraw their account up to a limit without an overdraft fee. The Credit Builder is a secured Visa credit card with no annual fee and no interest in the traditional sense, designed to help you build payment history without the risk of running up revolving debt. And early direct deposit can push your paycheck to you sooner than a typical bank would. Chime is not an investing platform, so you cannot buy stocks or crypto inside the app.

What Cash App is (and isn’t)

Cash App started as a peer-to-peer payments app and grew into a broader money platform. At its core it lets you send and receive money using a $Cashtag, split bills, and pay people instantly. Add the free Cash Card, a customizable Visa debit card, and you can spend your balance anywhere Visa is accepted and tap into “Boosts,” which are instant discounts at select merchants.

On top of payments, Cash App layers investing. You can buy stocks and exchange-traded funds, often in small fractional amounts, and you can buy, hold, and send Bitcoin. It also offers a savings feature that can pay a high APY when you meet the requirements, plus Cash App Borrow, a short-term loan feature offered to eligible users. Like Chime, Cash App is a fintech that works with partner banks for the banking side, so it is not a bank itself. If you are weighing it against another popular payments app, our breakdown of Cash App versus PayPal covers where each one wins for sending money.

Chime vs Cash App: side-by-side comparison

Here is how the two apps line up on the features most people care about. Remember that rates, limits, and fees change, so treat the numbers as a starting point and confirm the current details inside each app before you commit.

| Feature | Chime | Cash App |

|---|---|---|

| Best for | Everyday banking + credit building | Payments + investing |

| Core purpose | Checking & savings replacement | Send money, invest, spend |

| Monthly account fee | $0 for the core account | $0 for the core account |

| Debit card | Visa debit card | Cash Card (Visa debit) |

| Savings / APY | Savings Account offered (verify current rate) | Savings up to 4.5% APY with qualifying deposit |

| Overdraft | SpotMe, fee-free up to a limit | No SpotMe-style overdraft; Borrow if eligible |

| Investing | None built in | Stocks, ETFs, and Bitcoin |

| Credit building | Credit Builder secured card | No dedicated credit-builder product |

| Early direct deposit | Yes, up to two days early | Yes, up to two days early |

| FDIC insurance | Through partner banks | Through partner banks |

| Top perks require | Qualifying direct deposit | Qualifying direct deposit |

Fees: what you’ll actually pay

Both apps keep the core account free, with no monthly maintenance fee and no minimum balance to open. That is a big part of their appeal versus legacy banks. Still, “free” has edges. With Chime, out-of-network ATM withdrawals can carry a fee, and cash deposits at retail partners may cost you depending on where you load money. With Cash App, standard transfers to your linked bank are free but slow; an Instant transfer to a debit card charges a small percentage fee, and buying or selling Bitcoin can include a fee plus a price spread. Neither app charges you simply to hold an account, but read the in-app fee schedule so you are not surprised at the ATM or the cash register.

Savings and APY

If earning interest is your goal, Cash App has the more eye-catching headline: its savings feature can pay up to 4.5% APY, but that top rate is tied to meeting a qualifying direct deposit requirement, and the balance that earns the rate may be capped. Always confirm the current APY and the qualifying rules in the app, because promotional savings rates move with the market.

Chime also offers a Savings Account with automatic-savings features like round-ups and a percentage of each paycheck swept into savings. Chime does not always advertise a single flashy rate the way Cash App does, so if a high yield is your deciding factor, check the live number first. Our guide to Chime high-yield savings in 2026 walks through how the automatic-savings tools work and what to watch for. The bottom line: whichever app you pick, the advertised APY is a moving target, so verify it at the source rather than trusting an old screenshot.

Overdraft: SpotMe vs Borrow

This is one of the clearest differences. Chime’s SpotMe is a fee-free overdraft feature: eligible members can overdraw their Checking Account up to a set limit on debit-card purchases and cash withdrawals without paying an overdraft fee. The limit starts small and can grow over time based on account activity and direct deposits. It is meant as a cushion for the last few dollars before payday, not a loan. Our deeper explainer on how Chime SpotMe works covers eligibility and how limits increase.

Cash App does not offer a SpotMe-style overdraft. Instead, some users are offered Cash App Borrow, a short-term loan of a small amount that must be repaid, typically with a fee and within a set window. Borrow is not available to everyone, and it functions more like a small advance than a free overdraft buffer. If you routinely need a few extra dollars to bridge to payday without a fee, Chime’s SpotMe is the friendlier design.

Investing: only one app does it

If you want to invest, Cash App wins by default because Chime has no investing product. Inside Cash App you can buy fractional shares of stocks and ETFs, often starting with just a dollar, and you can buy and hold Bitcoin. That makes Cash App a reasonable starter platform for someone who wants to dip a toe into the market while keeping everything in one app. Keep expectations realistic: investing carries risk, crypto is especially volatile, and a payments app is not a substitute for a dedicated brokerage or retirement account if you are investing serious money. For long-term, tax-advantaged saving, look at an IRA or 401(k) instead, and confirm any contribution limits at IRS.gov.

Building credit: Chime’s edge

Chime’s Credit Builder is a secured Visa credit card with no annual fee and no minimum security deposit beyond the money you move into it. You spend only what you have loaded, and Chime reports your payment activity to the major credit bureaus, which can help you build a positive history over time. Because you cannot spend more than you set aside, it sidesteps the interest-and-debt spiral that trips people up on traditional credit cards.

Cash App does not have a dedicated credit-building product. If improving your credit score is a top priority, that tilts the decision toward Chime. As always, building credit is a slow game: on-time payments and low utilization over months and years are what move the needle, not any single app feature.

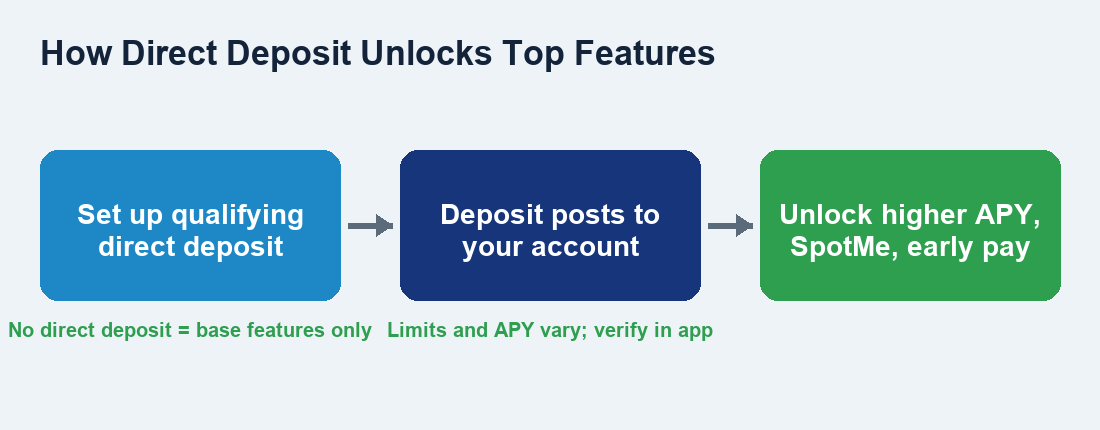

Direct deposit and early pay

Both apps let you receive your paycheck through direct deposit and can make your funds available up to two days early, depending on when your employer or payer submits the deposit. Early pay is one of the most-loved features of both platforms, and it is also the key that unlocks their best perks. On Cash App, a qualifying direct deposit is what turns on the higher savings APY and improves access to features like Borrow. On Chime, direct deposits are what enable and grow your SpotMe limit and unlock the fuller feature set. If you never set up direct deposit, you will only ever see the base version of each app.

Is your money safe? FDIC and scam awareness

Neither Chime nor Cash App is a bank. Both are fintech companies that place your deposits with FDIC-insured partner banks, so eligible balances are protected up to the standard federal insurance limits if a partner bank fails. That protection covers bank failure; it does not cover money you send to a scammer. Investing balances and Bitcoin are not FDIC-insured and can lose value.

Both apps, and Cash App in particular, are frequent targets for scams. Be skeptical of anyone promising to “flip” your cash into more money, of “customer support” numbers you find through a random search, and of anyone pressuring you to send a payment to claim a prize or fix a problem. Neither company will contact you out of the blue to ask for your PIN, password, sign-in code, or a payment. Treat a P2P payment like handing over cash: once it is sent to a stranger, it is usually gone. Only send money to people you know and trust, and enable every security setting the app offers, including a PIN or biometric lock and transaction alerts.

Which one is best for you?

Pick Chime if you want a primary account to replace a traditional bank, value fee-free overdraft coverage, want to build or rebuild credit, and like automatic savings tools. It is the better fit for someone whose main goal is to manage everyday money without fees and avoid overdraft charges.

Pick Cash App if your day-to-day revolves around sending and receiving money, you want to invest in stocks or Bitcoin from the same app, and you want to chase a higher savings APY. It shines as a flexible money tool, especially alongside a separate checking account, rather than as your only account.

Plenty of people use both: Chime as the account where their paycheck lands and their bills clear, and Cash App for splitting dinner, paying friends, and small investing. Since both core accounts are free, running the two side by side is a legitimate strategy rather than a compromise.

Frequently asked questions

Is Chime or Cash App a real bank?

Neither one is a bank. Both are financial technology companies that partner with FDIC-member banks to hold your deposits. Your eligible balance is insured through those partner banks up to the standard federal limits, but the fintech itself is not the bank of record.

Which has the higher savings rate?

Cash App advertises a savings feature that can pay up to 4.5% APY when you meet a qualifying direct deposit requirement, which is typically higher than what Chime promotes. Rates change often, so check the current APY and the qualifying rules inside each app before deciding, because the headline number can shift with the market.

Can I build credit with Cash App like I can with Chime?

Not directly. Chime offers the Credit Builder secured card, which reports your payment activity to the credit bureaus to help you build history. Cash App does not have a dedicated credit-building product, so if raising your credit score is the goal, Chime is the stronger choice.

Do I have to use direct deposit?

You can use either app without direct deposit, but you will miss the best features. A qualifying direct deposit is what unlocks Chime’s SpotMe overdraft coverage and larger limits, and it is what enables Cash App’s top savings APY and easier access to features like Borrow. Setting up direct deposit is the single biggest way to get more out of either app.

Which is safer from scams?

The security of your account depends more on your habits than on the app. Both platforms use industry-standard protections, but scammers target their users heavily. Turn on a PIN or biometric lock, enable transaction alerts, never share a login code or PIN, and only send money to people you know. No legitimate representative from either company will ask you to send them a payment or read them a security code.

The bottom line

Chime and Cash App are not really competing for the same job. Chime is the better everyday bank replacement, built around avoiding fees, covering small overdrafts, and building credit. Cash App is the better payments-and-investing tool, built around moving money and putting a little into stocks or Bitcoin. Match the app to your main goal, unlock the perks with a qualifying direct deposit, verify current rates and limits in the app before you rely on them, and stay alert to scams. For many people, the smartest answer is not one or the other but using each for what it does best.

{kind=link}