Chime vs SoFi comes down to one question: do you want a fee-free spending account built for getting paid early and rebuilding credit, or a full digital bank with a higher savings APY and a bigger welcome bonus? Chime wins for its overdraft cushion (SpotMe up to $200), its dedicated Credit Builder card, and simple no-balance-required banking, while SoFi wins for higher APY (up to roughly 3.80% typical in 2026 with direct deposit), extended FDIC coverage, and one-stop money management. Neither charges monthly maintenance fees, and both offer early direct deposit up to two days ahead of payday.

The rest of this guide breaks down every category that matters in 2026 — fees, APY, overdraft, early pay, credit building, sign-up bonuses, and FDIC safety — and ends with a clear recommendation based on how you actually bank.

Chime vs SoFi at a glance

Both are app-first, branch-free, and fee-light, but they are structured differently. The single biggest distinction: SoFi is a chartered bank (SoFi Bank, N.A.), while Chime is a fintech that partners with FDIC-member banks to hold your money. That difference shapes the APY, the overdraft rules, and the deposit insurance below.

| Feature | Chime | SoFi |

|---|---|---|

| Type | Fintech + partner banks | Chartered bank (SoFi Bank, N.A.) |

| Monthly fee | $0 | $0 |

| Minimum balance | $0 | $0 |

| Savings APY (typical 2026) | ~2.00% | Up to ~3.80% with direct deposit* |

| Checking APY | None (no interest) | ~0.50% with direct deposit* |

| Overdraft | SpotMe up to $200, no fee | Up to $50 coverage, no fee |

| Early direct deposit | Up to 2 days early | Up to 2 days early |

| Credit-builder product | Chime Credit Builder Visa (secured) | No dedicated secured builder card |

| Sign-up / referral bonus* | ~$100 referral (varies) | Up to ~$300 with direct deposit |

| Fee-free ATMs | 60,000+ (MoneyPass, Visa Plus) | 55,000+ (Allpoint) |

| FDIC insurance | Up to $250k via partner banks | Up to $250k direct; up to ~$2M via network |

*APY and bonus figures are typical 2026 estimates and change with the rate environment and current promotions. Always confirm the live rate and offer terms before opening.

Fees: what each account actually costs

This is close to a tie, and it is the reason both apps are popular with people escaping big-bank fees. Neither Chime nor SoFi charges a monthly maintenance fee, an overdraft fee, a minimum-balance fee, or a foreign-transaction fee on debit purchases.

Where small costs can creep in:

- Out-of-network ATMs. Chime charges around $2.50 per withdrawal outside its fee-free network; SoFi similarly charges for ATMs outside the Allpoint network. Stick to in-network machines and you pay nothing.

- Cash deposits. Chime lets you deposit cash at retail partners, but some retailers charge their own fee. SoFi does not natively support over-the-counter cash deposits the same way, which matters if you handle a lot of cash.

- Wire transfers. SoFi supports outgoing domestic wires (sometimes with a fee); Chime does not offer traditional wires, which can be a dealbreaker for larger one-off payments.

Bottom line: for everyday debit spending, both are effectively free. SoFi is the more flexible choice if you occasionally need wires; Chime is friendlier if you deposit physical cash.

APY: where SoFi pulls clearly ahead

If you keep a meaningful savings balance, SoFi is the stronger earner. Because SoFi holds a bank charter, it competes directly with high-yield savings accounts and has historically offered a top-tier APY on savings when you set up a qualifying direct deposit. In 2026 that rate sits in the ~3.80% range (down from the 4%+ peaks of prior years as benchmark rates eased), plus a small APY on the checking balance.

Chime’s Savings Account pays a flat rate in the ~2.00% area and skips the direct-deposit hoops, but it simply is not designed to be a rate-chaser’s account — it is a place to auto-save round-ups and a slice of each paycheck. If maximizing yield is your goal, read our Chime high-yield savings breakdown to see how its Round Ups and Save When I Get Paid features work before you compare the headline numbers.

On a $10,000 balance, the gap between ~2.00% and ~3.80% is roughly $180 per year in interest — modest but real, and it grows with your balance. For big emergency-fund or savings balances, SoFi is the better home.

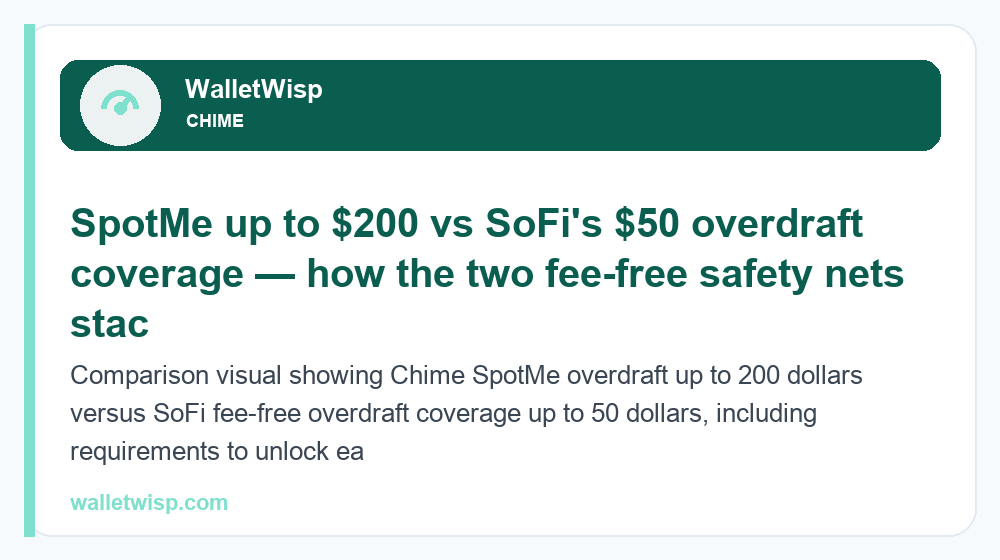

Overdraft: SpotMe vs SoFi overdraft coverage

This is the category where Chime genuinely leads. Both apps let you overspend without the classic $35 overdraft fee, but the coverage amounts are very different.

Chime SpotMe covers debit card purchases and ATM withdrawals with no fee. New users typically start with a $20 limit, which can grow up to $200 based on your direct-deposit history and account activity. There is no interest and no mandatory tip — Chime simply recovers the amount from your next deposit.

SoFi overdraft coverage is also fee-free, but the ceiling is lower — up to $50 — and it requires at least $1,000 in qualifying direct deposits in the prior 30 days to unlock. It is a safety net, not a spending cushion.

| Overdraft detail | Chime SpotMe | SoFi overdraft coverage |

|---|---|---|

| Maximum limit | Up to $200 | Up to $50 |

| Starting limit | Often $20 | Up to $50 once eligible |

| Overdraft fee | $0 | $0 |

| Interest / tip | None (optional tip) | None |

| Requirement to unlock | Qualifying direct deposit history | $1,000+ direct deposit / 30 days |

| Covers ATM withdrawals | Yes | Purchases (varies) |

| How the limit grows | With usage & deposit history | Fixed cap at $50 |

If you occasionally run your balance to zero before payday, SpotMe’s larger, usage-based limit is the more useful cushion. SoFi’s overdraft is fine as a backstop but was never meant to bridge a real cash gap.

Early direct deposit: a tie

Both apps advertise getting your paycheck up to two days early, and both deliver it the same way — by posting your employer’s ACH deposit as soon as the payment file arrives rather than waiting for the official settlement date. The actual number of days depends on when your payroll provider submits the file, not on the app.

Government benefits, tax refunds, and many gig-platform payouts also qualify. In practice, most direct-deposit users see funds one to two days early on both Chime and SoFi, so this feature should not be your deciding factor.

Credit building: Chime Credit Builder vs SoFi

Chime has a clear, purpose-built advantage here. The Chime Credit Builder Visa is a secured card with no annual fee, no interest, and no credit check to apply. You move money into a Credit Builder account, spend on the card, and Chime reports your on-time payments to the major credit bureaus — a straightforward way to build history without the risk of revolving interest. For a full walkthrough of how it reports and how fast scores tend to move, see our Chime Credit Builder card guide.

SoFi does not offer an equivalent secured builder card. It has a rewards credit card, but that is a traditional unsecured product that requires a credit approval and is aimed at people who already have decent credit — not at someone trying to establish or rebuild a score. SoFi’s strength is on the other side of the credit journey: personal loans, student-loan refinancing, and investing, all inside one app.

So if your primary goal is building or repairing credit safely, Chime is the obvious pick. If you already have healthy credit and want borrowing plus investing under one roof, SoFi fits better.

Sign-up and referral bonuses

SoFi generally runs the more lucrative promotion. New members who set up a qualifying direct deposit can typically earn a tiered welcome bonus of up to about $300, with smaller amounts for smaller deposit thresholds. Chime’s headline incentive is usually a referral bonus of around $100, paid to both the new user and the referrer once the new account receives a qualifying direct deposit within the promo window.

| Bonus detail | Chime | SoFi |

|---|---|---|

| Typical bonus size | ~$100 (referral) | Up to ~$300 (tiered) |

| How it’s earned | Referral + qualifying direct deposit | Qualifying direct deposit tier |

| Direct deposit required | Yes | Yes |

| Best for | Anyone with a referral link | People moving their whole paycheck |

Bonuses change frequently, so treat these as typical figures and confirm the current offer and its exact direct-deposit requirements before you commit. A bonus is a nice one-time perk, but the ongoing APY and fee structure matter far more over a year.

FDIC insurance and safety

Your money is protected at both, but through different mechanisms. Chime is not itself a bank; it places your funds with partner banks (such as The Bancorp Bank and Stride Bank), where they are FDIC-insured up to the standard $250,000 per depositor. SoFi holds a bank charter and insures deposits directly up to $250,000 — and through its expanded deposit network, eligible balances can be covered well beyond that (commonly cited up to around $2 million for individual accounts).

For most people, $250,000 of coverage is plenty. If you regularly hold six figures in cash, SoFi’s extended coverage program is a meaningful edge. Either way, keep your login credentials secure and enable two-factor authentication, since app-based fraud — not bank failure — is the realistic risk.

Which should you choose? Recommendation by use case

There is no single winner — the right pick depends on your situation:

- Choose Chime if you want to rebuild or establish credit, need a larger fee-free overdraft cushion (SpotMe up to $200), deposit cash regularly, or simply want a clean everyday spending account with no minimums and no rate hoops.

- Choose SoFi if you keep a substantial savings balance and want the higher ~3.80% APY, want your checking, savings, loans, and investing in one app, need occasional wires, value extended FDIC coverage, or want the larger welcome bonus.

- Use both if you want the best of each: SoFi as your high-yield savings hub and Chime for its Credit Builder card and SpotMe overdraft. Many people run exactly this combo.

If you are still weighing app-based accounts more broadly, it is also worth seeing how Chime stacks up against peer-to-peer options in our Chime vs Cash App comparison before you settle on where your paycheck lands.

Frequently Asked Questions

Is Chime or SoFi better for building credit?

Chime is better for building credit thanks to its Credit Builder Visa, a secured card with no annual fee, no interest, and no credit check that reports on-time payments to the bureaus. SoFi has no comparable secured builder product.

Does SoFi or Chime have the higher APY in 2026?

SoFi has the higher APY, typically around 3.80% on savings with a qualifying direct deposit in 2026, versus roughly 2.00% on Chime’s savings account. Rates change with the market, so verify the current number before opening.

How does SpotMe compare to SoFi overdraft?

SpotMe covers up to $200 with no fee and grows with your usage and deposit history, while SoFi’s fee-free overdraft coverage caps at $50 and requires $1,000+ in monthly direct deposits. SpotMe is the larger cushion.

Do both Chime and SoFi offer early direct deposit?

Yes. Both post eligible direct deposits up to two days early by releasing funds when the payroll file arrives rather than on the official settlement date. The exact timing depends on your employer’s payroll provider.

Are Chime and SoFi FDIC insured?

Both protect your money with FDIC insurance up to $250,000. Chime does so through partner banks since it is a fintech, while SoFi is a chartered bank and can extend coverage well beyond $250,000 through its deposit network.

Which has better sign-up bonuses, Chime or SoFi?

SoFi usually offers the larger bonus — up to about $300 in tiers based on your direct-deposit amount. Chime’s main incentive is a referral bonus around $100 that pays out after a qualifying direct deposit. Offers change often.

Can I use both Chime and SoFi at the same time?

Yes, and many people do. A common setup uses SoFi for high-yield savings and everyday banking, plus Chime for its Credit Builder card and SpotMe overdraft. There is no penalty for holding both accounts.

Is SoFi a real bank and Chime is not?

Correct. SoFi holds a national bank charter (SoFi Bank, N.A.), so it is a bank. Chime is a financial technology company that partners with FDIC-member banks to hold and insure your deposits, but it is not itself a bank.

{kind=link}