The advertised X Money 6% APY is a promotional, teaser-style rate on the balance you hold inside Elon Musk’s X Money account, not a guaranteed long-term yield from a chartered bank. X Money is the payments and stored-value product built into the X app (formerly Twitter), operated with money-transmitter licenses and a partner bank rather than being a bank itself. If the roughly 6% figure holds, it would beat most competitors on paper, but it typically comes with conditions, caps, and rate-change risk you need to read carefully before moving real money.

Below is a plain-English breakdown of what X Money actually is, how a 6% yield can be offered, whether your cash is FDIC-insured, the fees, eligibility, and how it stacks up against Cash App, Chime, and a traditional high-yield savings account in 2026.

What is X Money?

X Money is the in-app financial layer of X, part of Elon Musk’s long-stated goal of turning the platform into an “everything app” for messaging, content, and money. In practice it bundles a few familiar fintech pieces: a digital wallet, peer-to-peer (P2P) transfers between X users, the ability to load and cash out funds, and a linked debit card for spending. The company has pursued state money-transmitter licenses across most of the US and announced a payments partnership with Visa to power instant funding and P2P features.

Crucially, X Money is a fintech app, not a bank. It resembles the model used by Cash App, Venmo, and Chime: a technology company handles the app and user experience while a chartered partner bank actually holds the deposits and provides FDIC coverage. That distinction matters for the 6% APY, for insurance, and for how much protection you really have.

How the X Money 6% APY works

The X Money 6% APY is best understood as a promotional yield on your wallet balance, designed to pull users into the ecosystem and encourage them to keep cash inside X rather than in an outside bank. High headline rates like this are almost always funded by one of three things: partner-bank interest-sharing, the fintech’s own marketing budget as a customer-acquisition cost, or returns on the pooled deposits held at the partner bank. Because the rate is promotional, it can be adjusted or ended with notice, unlike a fixed CD.

Annual percentage yield (APY) is the real, compounded return over a year. On a 6% APY, $1,000 held for a full year earns about $60 before any conditions; $10,000 earns roughly $600. But teaser rates typically attach strings such as a balance cap (the top rate may only apply up to a set amount, with lower or zero yield above it), direct-deposit or activity requirements, a promotional window, or eligibility tied to a paid X subscription tier. Always confirm the exact terms in the app before assuming you will earn the full advertised rate on your whole balance.

What a 6% APY could earn you (illustrative estimate)

| Balance held | Est. annual earnings at 6% APY | Est. earnings at 4.5% APY | Est. earnings at 0.40% (big-bank avg) |

|---|---|---|---|

| $500 | ~$30 | ~$22.50 | ~$2.00 |

| $2,000 | ~$120 | ~$90 | ~$8.00 |

| $5,000 | ~$300 | ~$225 | ~$20.00 |

| $10,000 | ~$600 | ~$450 | ~$40.00 |

These figures are simplified estimates assuming the rate applies to the full balance for a full year with no cap; real earnings depend on the actual terms, any balance limit, and how long the promotional rate lasts.

Is X Money FDIC-insured? Partner-bank status explained

This is the most important safety question, and the honest answer is: your money is only FDIC-insured if, and to the extent that, X’s partner bank holds it in an eligible deposit account in your name (or through a pass-through arrangement). X Money itself, as a money transmitter, is not a bank and cannot directly insure deposits. Coverage is provided by the underlying chartered bank, and the standard FDIC limit is $250,000 per depositor, per insured bank, per ownership category.

Two cautions apply. First, funds you hold as a stored balance in a payments app are not automatically insured the way a bank checking or savings account is; insurance usually requires the money to be swept to the partner bank. If cash simply sits in the app’s transmitter float, it may not be covered against the fintech’s failure. Second, “FDIC-insured” protects you if the bank fails, not if you get scammed, send money to the wrong person, or lose access to your account. Before funding X Money, verify in the disclosures exactly which bank holds deposits and whether pass-through insurance applies to your balance.

The X Money debit card

The X Money debit card is a linked card (reported to run on the Visa network) that lets you spend your wallet balance in stores and online and, in many fintech setups, withdraw cash at ATMs. Like Cash App’s card and Chime’s Visa debit, it draws directly from your available balance rather than extending credit, so there is no interest on purchases and no credit check to get one.

Typical debit-card features to expect from a product like this include instant virtual card issuance for online use, mobile-wallet compatibility (Apple Pay / Google Pay), and in-app controls to freeze the card. Watch for out-of-network ATM fees, any card issuance or replacement fee, and foreign-transaction costs, since these vary by program and are where fintech cards often differ from a plain bank account.

X Money fees to watch for

Fintech wallets usually advertise “no monthly fee” but recoup costs through specific transaction fees. Based on how comparable services (Cash App, Venmo, Chime) are structured, here are the fee categories to check inside X Money before you rely on it:

- Monthly maintenance: commonly $0 for a basic account, though the top APY may require a paid X Premium subscription.

- Instant transfers/cash-out: many apps charge a percentage fee (often ~0.5%–1.75%) to move money instantly to an external debit card, while standard ACH transfers are free but slower.

- ATM withdrawals: free at in-network ATMs; out-of-network machines may add a flat fee plus the operator’s charge.

- Card purchases: normally free for the cardholder.

- Foreign transactions & currency conversion: possible added percentage.

None of these should surprise you if you read the fee schedule first. The single biggest “hidden cost” with any high-APY wallet is opportunity cost: if the rate drops after a promo window and you leave cash parked, you may quietly earn less than a stable online bank would pay.

Eligibility: who can open X Money in 2026

Exact requirements are set by X and its partner bank, but a product like this generally expects you to:

- Be a US resident, at least 18 years old, with a valid Social Security number or ITIN for identity verification (KYC).

- Have an X account in good standing; the highest APY tiers may require an active X Premium subscription.

- Pass standard identity checks and live in a state where X holds the necessary money-transmitter license (rollouts are usually state-by-state).

- Link a funding source such as an external bank account or debit card.

If you are outside the US, availability in 2026 is likely limited or unavailable, since money-transmitter licensing and bank partnerships are country-specific.

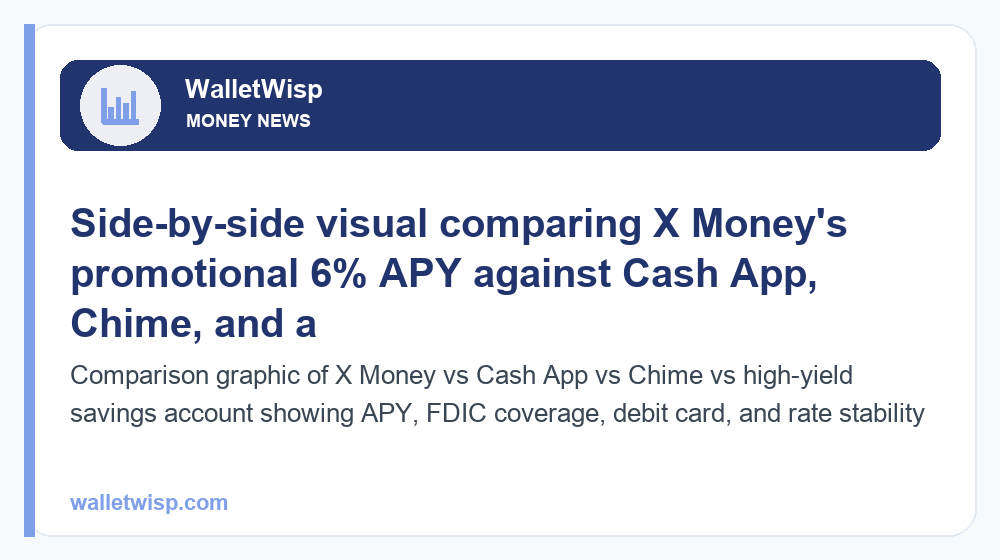

X Money vs Cash App vs Chime vs a high-yield savings account

The right comparison depends on what you actually want the money to do. X Money leans on social payments plus a headline yield; Chime leans on everyday banking with early direct deposit; Cash App blends P2P, investing, and a savings feature; and a dedicated high-yield savings account (HYSA) leans on rate stability and pure safety. Here is a side-by-side using typical 2026 ranges.

| Feature | X Money | Cash App | Chime | Online HYSA |

|---|---|---|---|---|

| Advertised savings APY | ~6% (promotional, est.) | Up to ~4.5% (with conditions) | ~2%–3.75% (with direct deposit) | ~4%–5% (varies) |

| Is it a bank? | No — money transmitter + partner bank | No — partner banks | No — partner banks | Yes — chartered bank |

| FDIC coverage | Via partner bank (verify pass-through) | Via partner bank | Via partner bank | Direct, up to $250k |

| Debit card | Yes (Visa, reported) | Yes (Cash Card) | Yes (Visa) | Sometimes |

| Rate stability | Low (promo, can change) | Medium | Medium | Higher |

| Main draw | Social P2P + high headline yield | P2P, investing, Bitcoin | Early paycheck, no-fee banking | Safe, competitive, boring |

If your priority is the highest reliable yield on savings you rarely touch, compare X Money’s promo rate against the current leaders in our roundup of the best high-yield savings rates for July 2026. If you want steady no-fee banking with early direct deposit instead of a teaser rate, read our breakdown of Chime high-yield savings in 2026. And if you already live in a payments app, our guide to Cash App’s 4.5% APY savings shows the conditions a similar high-yield offer usually carries.

Risks of X Money to weigh in 2026

A 6% headline is attractive, but treat it with healthy skepticism:

- Rate risk: promotional APYs can be cut with little notice once the customer-acquisition push cools off. Do not build a budget around 6% lasting forever.

- Insurance nuance: a stored balance is not automatically the same as an insured bank deposit. Confirm the sweep and pass-through details.

- Concentration and account-lock risk: tying your money, identity, and social account to one platform means a suspension or dispute could freeze funds you need. Keep an emergency buffer elsewhere.

- Newness: a young product has less track record on customer service, dispute resolution, and outages than an established bank.

- Scam exposure: P2P payments are usually irreversible; FDIC insurance never covers money you were tricked into sending.

Is X Money worth it? The bottom line

The X Money 6% APY can be worth chasing for a portion of your cash if you verify three things: that the rate genuinely applies to your balance (not just a tiny cap), that your funds are FDIC-insured through the named partner bank, and that any subscription cost to unlock the rate does not erase the extra interest. For heavy X users who want social payments plus a yield boost, it is a reasonable place to park spending money and a modest savings cushion.

For your core emergency fund and long-term savings, a stable, established high-yield savings account is still the safer home in 2026. A sensible approach is to use X Money for what it is good at, social payments and an opportunistic yield on a limited balance, while keeping the bulk of your safety net in a proven, directly-insured account. Read the terms, confirm the insurance, and never let one flashy rate concentrate all your cash in a single app.

Frequently Asked Questions

Is the X Money 6% APY real or a scam?

It is a real, advertised promotional rate rather than a scam, but it is a teaser-style yield that can carry balance caps, subscription requirements, or a limited promo window. Always confirm the exact terms in the X app before assuming you will earn 6% on your full balance for the long term.

Is money in X Money FDIC-insured?

Only through X’s chartered partner bank, and typically only when your funds are swept to that bank under a pass-through arrangement. X itself is a money transmitter, not a bank, so verify in the disclosures which bank holds deposits and whether your specific balance qualifies for the $250,000 FDIC limit.

Do I need X Premium to get the X Money 6% APY?

Possibly. High-yield fintech tiers often require a paid subscription or activity conditions like direct deposit. If a subscription is required, subtract its annual cost from your expected interest to see whether the 6% still comes out ahead for your balance size.

How is X Money different from a bank?

X Money is a fintech wallet that partners with a bank, similar to Cash App or Chime, rather than being a chartered bank itself. Deposits, insurance, and interest ultimately flow through the partner bank, so your protection depends on that arrangement, not on X directly.

Can I get a debit card with X Money?

Yes, X Money offers a linked debit card (reported to run on Visa) that spends directly from your wallet balance, with no credit check and no interest on purchases. Watch for out-of-network ATM fees, replacement fees, and any foreign-transaction charges.

Is X Money better than Cash App or Chime?

It depends on your goal. X Money advertises a higher headline APY, but Chime is stronger for no-fee everyday banking and early direct deposit, and Cash App adds investing and Bitcoin. For pure rate stability and safety, a dedicated high-yield savings account often wins.

Can people outside the US use X Money?

In 2026, availability is largely US-focused because money-transmitter licensing and bank partnerships are country-specific. International rollout, if it happens, would require separate local licensing, so non-US users should not assume access or the same 6% offer.

Will the X Money 6% APY last?

There is no guarantee. Promotional rates are commonly reduced once the initial growth push slows, so treat 6% as a possibly temporary bonus rather than a permanent yield. Keep your core emergency fund in a stable account and revisit the rate periodically.

{kind=link}