In 2026, money market accounts (MMAs) and high-yield savings accounts (HYSAs) pay almost identical rates, both typically landing in the 4.00%-4.50% APY range at online banks and credit unions. Neither one reliably earns more than the other, because both track the same short-term interest rates. The real difference is access: money market accounts often come with checks and a debit card, while high-yield savings accounts usually move money only through transfers. Choose based on how you plan to use the cash, not on a fraction-of-a-percent rate gap.

Below, we break down exactly how the two accounts compare in 2026, how much you would actually earn on common balances, and which type fits different savings goals. Both are safe, both are liquid, and both beat the near-zero rates that big traditional banks still pay on standard savings.

Money Market vs High-Yield Savings: The Core Difference

A high-yield savings account is a savings account offered mostly by online banks that pays a much higher rate than a standard brick-and-mortar savings account. A money market account is a deposit account that blends savings and checking features, often adding check-writing and a debit card on top of a competitive rate.

The names cause confusion. A money market account (MMA) is a federally insured bank or credit union deposit account. It is not the same as a money market fund, which is an investment product sold by brokerages, is not FDIC insured, and can lose value. This article is about money market accounts, the insured kind.

Here is what matters in 2026: the Federal Reserve’s benchmark rate sits in the mid-3% to low-4% area after the cuts of 2024 and 2025, so the top savings and money market yields have settled around 4%. Because both account types are priced off those same short-term rates, their APYs move together. When one bank raises its HYSA rate, its MMA rate usually follows, and vice versa.

What they have in common

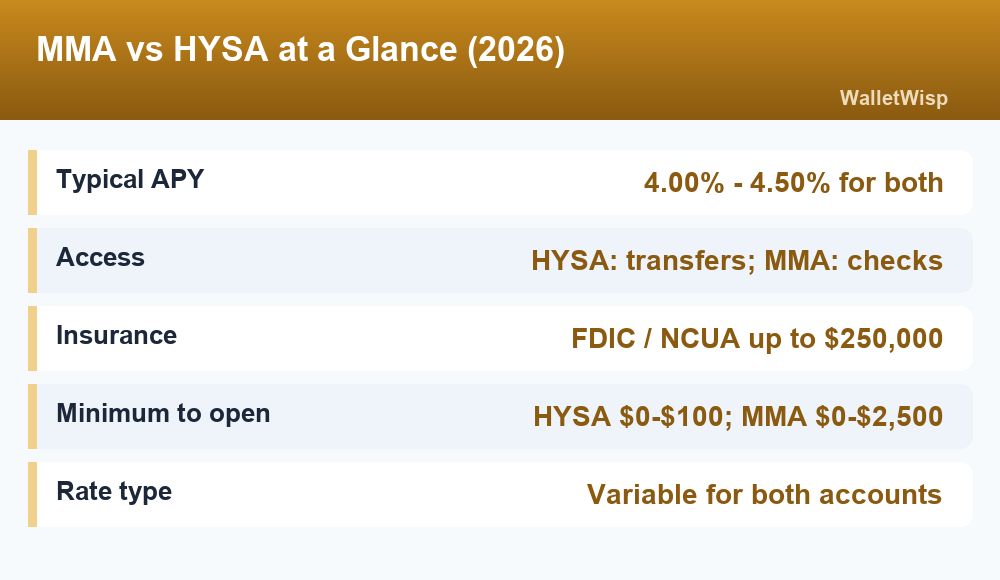

- Similar APYs. Both cluster around 4.00%-4.50% at the most competitive online institutions in 2026.

- Federal insurance. Bank accounts carry FDIC coverage; credit union accounts carry NCUA coverage. Both protect up to $250,000 per depositor, per institution, per ownership category.

- Variable rates. Neither locks your rate. Both can rise or fall as the Fed adjusts policy.

- Liquidity. You can withdraw your money without the penalties that come with a CD.

Where they differ

- Access. MMAs frequently include paper checks and a debit or ATM card. Most HYSAs do not, so you transfer to a linked checking account first.

- Minimums. Many HYSAs have no minimum at all. MMAs are more likely to require a minimum balance to open or to earn the top tier.

- Fees. MMAs are somewhat more likely to charge a monthly fee if you fall below a balance threshold.

2026 Head-to-Head Comparison Table

The table below summarizes how a typical online high-yield savings account stacks up against a typical online or credit-union money market account in 2026. Individual banks vary, so always confirm the current terms before you open.

| Feature | High-Yield Savings (HYSA) | Money Market (MMA) |

|---|---|---|

| Typical 2026 APY | 4.00% – 4.50% | 4.00% – 4.50% |

| Check-writing | Rarely | Often included |

| Debit / ATM card | Sometimes | Commonly included |

| Minimum to open | $0 – $100 | $0 – $2,500 |

| Minimum to earn top APY | Usually none | Sometimes a tier applies |

| Monthly maintenance fee | Usually none | Possible if under a balance |

| Federal insurance | FDIC / NCUA to $250,000 | FDIC / NCUA to $250,000 |

| Rate type | Variable | Variable |

| Best for | Emergency fund, pure saving | Savings you may spend from |

If you want to see current live rates before committing, our roundup of the best high-yield savings rates for July 2026 tracks the top nationally available offers and updates as banks adjust.

Which One Actually Earns More in 2026?

Because the APYs are so close, the account that earns more is simply whichever one carries the higher rate on the day you open it and keeps that edge over time. There is no structural reason a money market account beats a high-yield savings account or the reverse. In any given month, some banks lead with their MMA, others lead with their HYSA.

What matters far more than the account label is the size of the rate itself. The gap between a top online account at 4.40% and a legacy megabank savings account at 0.01% is enormous. On $10,000, that is roughly $440 a year versus about $1. Chasing the difference between 4.40% and 4.45% is not worth the effort; escaping a 0.01% account is.

Earnings on common balances

Here is what you would earn in a year at two representative 2026 yields. Because APY already accounts for compounding, these figures reflect a full year at a steady rate.

| Balance | At 4.00% APY (1 year) | At 4.40% APY (1 year) |

|---|---|---|

| $1,000 | $40 | $44 |

| $5,000 | $200 | $220 |

| $10,000 | $400 | $440 |

| $25,000 | $1,000 | $1,100 |

| $50,000 | $2,000 | $2,200 |

Notice how small the 0.40-point difference is: only $40 a year on $10,000. That is why access, fees, and convenience should usually decide your choice, not a minor rate edge.

How to Choose Between an MMA and a HYSA

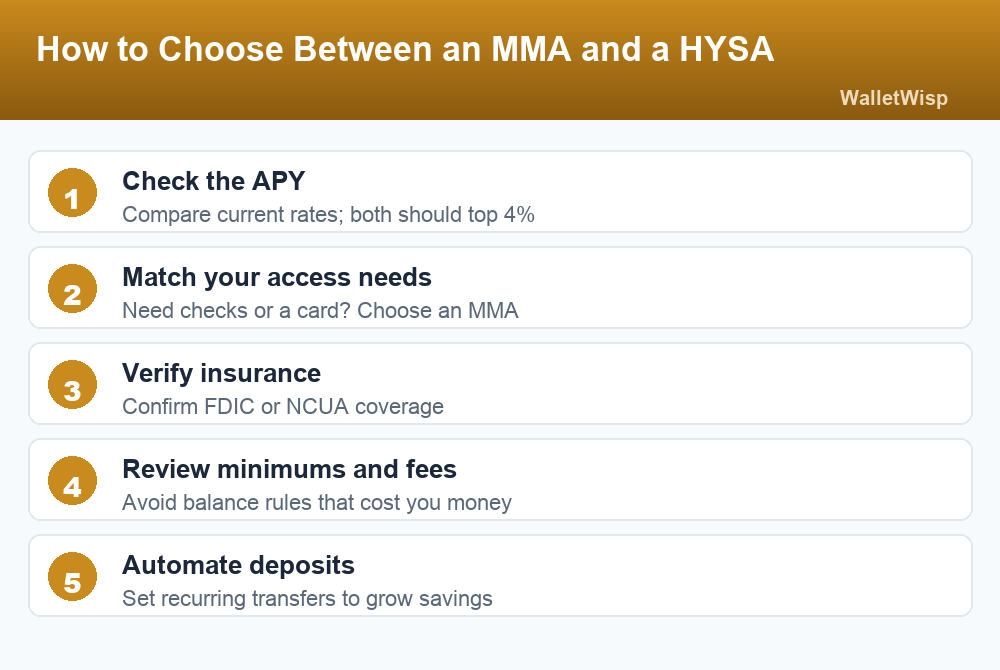

Start with how you intend to touch the money. If the cash is a pure cushion you rarely spend, a high-yield savings account keeps it slightly out of reach, which is a feature for an emergency fund. If you want to write an occasional check or swipe a card straight from the account, a money market account gives you that flexibility without sacrificing yield.

Pick a high-yield savings account if you

- Are building an emergency fund or a sinking fund for a specific goal.

- Want zero minimums and zero monthly fees.

- Do not need checks or a debit card attached to the savings.

- Prefer a simple, single-purpose place to park cash and let it grow.

Pick a money market account if you

- Want to spend directly from savings a few times a month.

- Like having checks for rent, contractors, or large one-off payments.

- Keep a larger balance that easily clears any minimum requirement.

- Value a debit or ATM card for occasional access without a transfer.

Some people use both. A common setup is a no-fee HYSA for the untouchable emergency fund and an MMA for near-term money like a home-repair or tax reserve that you may need to spend on short notice. If you bank with a fintech, compare those options against app-based savings too; our guide to Chime high-yield savings in 2026 shows how a mobile-first account stacks up on rate and access.

Rate Variability: Why Both Can Change Overnight

Neither account guarantees a rate. Both are variable, meaning the bank can raise or lower the APY at any time, usually following the Fed. That is different from a certificate of deposit, which locks your rate for a set term.

In practice, online banks move their savings and money market rates within days of a Fed decision. Through 2026, most forecasts point to a relatively stable to modestly lower path, but nothing is promised. If you want part of your cash shielded from falling rates, a CD or a CD ladder can lock a yield for months or years. Our walkthrough on how to build a CD ladder in 2026 explains how to blend locked and liquid savings so you keep access while protecting some of your return.

A simple way to think about it

- Need the money soon or unsure: HYSA or MMA, both fully liquid.

- Won’t touch it for months and want rate protection: a CD or CD ladder.

- Want the best of both: keep a liquid HYSA or MMA plus a short ladder.

Safety: FDIC and NCUA in 2026

Both account types are among the safest places to keep money. Bank deposits are insured by the FDIC, and credit union deposits by the NCUA, each covering up to $250,000 per depositor, per institution, per ownership category. That coverage is identical whether the account is called high-yield savings or money market.

Two safety reminders for 2026:

- Confirm the insurance. Before opening any online or fintech account, verify it is FDIC or NCUA insured. Some fintech apps hold your money at partner banks; make sure the pass-through coverage is clearly stated.

- Mind the money market fund distinction. A money market account is insured. A money market fund from a brokerage is not, and its value can dip below the amount you put in, even if only briefly.

If your balance exceeds $250,000, spread it across multiple insured institutions or ownership categories so every dollar stays covered.

The Bottom Line

In the money market vs high-yield savings debate for 2026, there is no clear winner on rate; both pay roughly 4.00%-4.50% and move together. The account that fits you comes down to access and cost. Choose a high-yield savings account for a clean, no-fee place to grow an emergency fund, and a money market account when you want checks or a card to spend from savings directly. Whichever you pick, the important move is getting your cash out of a near-zero legacy account and into an insured, competitive one, then setting up automatic transfers so the balance grows on its own.

Frequently Asked Questions

Is a money market account better than a high-yield savings account?

Neither is universally better. In 2026 they pay nearly the same APY, so the choice depends on access. A money market account often adds checks and a debit card, while a high-yield savings account is a simpler, usually fee-free place to save. Pick based on how you plan to use the money.

Which pays a higher interest rate in 2026?

It varies by bank, not by account type. Some institutions lead with their money market rate, others with their high-yield savings rate, and both typically fall in the 4.00%-4.50% range. Compare the exact APY at the specific bank rather than assuming one category always pays more.

Are money market accounts and high-yield savings accounts FDIC insured?

Yes, when held at an FDIC member bank, both are insured up to $250,000 per depositor, per institution, per ownership category. At a credit union, the same coverage comes from the NCUA. Just confirm the institution is insured before you deposit.

Can I lose money in a money market account?

Not in an insured money market account at a bank or credit union, as long as you stay within coverage limits. You can lose value in a money market fund, which is an uninsured brokerage investment. The two are different products with similar names, so check which one you are opening.

How often do these rates change?

Both are variable and can change at any time, usually shortly after the Federal Reserve adjusts its benchmark rate. Online banks often update within days of a Fed decision. If you want a fixed rate, a CD locks your yield for a set term instead.

Do I need a large balance to open one?

Many high-yield savings accounts have no minimum. Money market accounts are more likely to require a minimum to open or to earn the top rate, sometimes up to $2,500. Always read the terms so you avoid a monthly fee for falling below a threshold.

Can I write checks or use a debit card with these accounts?

Money market accounts commonly include checks and a debit or ATM card. High-yield savings accounts usually do not, so you move money to a linked checking account first. If direct spending from savings matters to you, that access is the main reason to choose a money market account.

Should I use a CD instead?

Use a CD if you can leave the money untouched and want to lock the rate against future cuts. Use a high-yield savings or money market account when you need liquidity. Many savers combine both: a liquid account for near-term cash and a CD ladder for money they can commit longer.

")

{kind=link}