A Health Savings Account (HSA) is a tax-advantaged account you can only open when you have a qualifying high-deductible health plan, and it is the single most tax-friendly account in the entire US tax code: the money can go in tax-free, grow tax-free, and come out tax-free when you spend it on medical care. That combination is what people mean when they talk about the HSA “triple tax advantage.”

Quick answer: An HSA gives you three separate tax breaks that no other account combines: your contributions are pre-tax or tax-deductible, your balance grows tax-free, and withdrawals for qualified medical expenses are never taxed. To contribute you must be covered by a qualifying high-deductible health plan (HDHP) and have no disqualifying coverage. Unused money rolls over every year and stays yours for life, so many people use an HSA as a stealth retirement account. The IRS sets the annual contribution limits, so verify the 2026 figures at IRS.gov before you fund it.

What is a health savings account?

An HSA is a personal savings and investment account earmarked for health costs. You put money in, the balance sits there earning interest or investment returns, and you pull money out to pay for doctor visits, prescriptions, dental work, and dozens of other qualified expenses. What makes it different from an ordinary savings account is the tax treatment and one key eligibility rule: you can only contribute when you are enrolled in a qualifying high-deductible health plan.

Crucially, an HSA belongs to you, not your employer. If you change jobs, get laid off, or retire, the account and every dollar in it goes with you. That portability is one of the biggest reasons HSAs have become a cornerstone of long-term financial planning rather than just a way to pay this year’s copays.

Who is eligible? The HDHP rule

Eligibility is the part people trip over, so it is worth slowing down. To open and contribute to an HSA, you generally must meet all of these conditions:

- You are covered by a qualifying high-deductible health plan (HDHP). The IRS defines the minimum deductible and maximum out-of-pocket amounts that make a plan “HSA-qualified,” and those thresholds are updated annually.

- You have no disqualifying coverage. Being enrolled in Medicare, being covered by a general-purpose FSA, or having a second non-HDHP health plan can all make you ineligible to contribute.

- You are not claimed as a dependent on someone else’s tax return.

An important nuance: eligibility is judged month by month. If you lose HDHP coverage partway through the year, you simply stop contributing for the months you no longer qualify. And once you enroll in Medicare, you can no longer add new money to an HSA, though you can keep spending the balance you already built. Because the exact deductible and out-of-pocket numbers change each year, confirm your plan actually qualifies by checking your plan documents or IRS.gov rather than assuming.

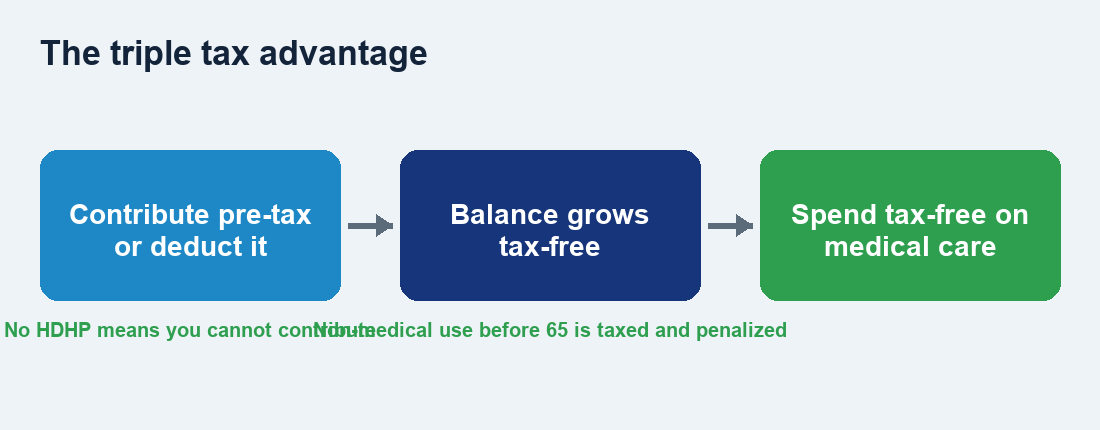

The triple tax advantage explained

Most tax-advantaged accounts give you one tax break. A traditional 401(k) lets money go in pre-tax but taxes withdrawals. A Roth IRA is funded with after-tax dollars but withdrawals are tax-free. An HSA is the rare account that stacks all three benefits at once:

- Tax-free going in. Contributions are either pre-tax (when made through payroll) or tax-deductible (when you contribute on your own), which lowers your taxable income for the year.

- Tax-free growth. Any interest, dividends, or investment gains inside the account are never taxed as they accumulate.

- Tax-free coming out. When you withdraw money to pay for a qualified medical expense, that withdrawal is completely tax-free, no matter how much the account has grown.

Payroll contributions carry a bonus: money routed straight from your paycheck into an HSA also typically avoids Social Security and Medicare (FICA) taxes, a break you do not get with an IRA. That is why funding your HSA through your employer’s payroll system, when available, is usually the most tax-efficient route.

2026 contribution limits (verify at IRS.gov)

The IRS sets separate annual contribution limits for self-only HDHP coverage and family coverage, and it raises them most years to keep pace with inflation. People who are 55 or older are also allowed an additional catch-up contribution on top of the standard limit. Because these figures are adjusted annually and any specific dollar amount can be out of date within months, we are deliberately not printing exact numbers here.

Before you fund your account for the year, look up the current amounts at IRS.gov or inside your HSA provider’s app, which will usually flag if you are on track to over-contribute. Contributing more than the legal limit triggers an excise tax until you remove the excess, so it is worth getting right. If you are married and both spouses have their own HDHP coverage, pay special attention, because family-limit rules can be easy to misread.

| Contribution detail | What to know for 2026 |

|---|---|

| Self-only coverage limit | Set by the IRS — verify at IRS.gov |

| Family coverage limit | Set by the IRS — verify at IRS.gov |

| Catch-up (age 55+) | Extra amount on top — verify at IRS.gov |

| Contribution deadline | Generally the tax-filing deadline for the year |

| Employer contributions | Count toward your annual limit |

One planning tip: HSA contributions fit neatly inside a normal monthly budget. If you follow a framework like the 50/30/20 budgeting rule, funding your HSA can live alongside your other savings goals rather than competing with them, since the tax deduction effectively lowers the real cost of every dollar you set aside.

What counts as a qualified medical expense?

The list of qualified expenses is broad and defined by the IRS in Publication 502. It generally includes doctor and specialist visits, hospital care, prescription drugs, dental and orthodontic work, vision care and glasses, mental health treatment, and many over-the-counter items such as pain relievers and first-aid supplies. Menstrual products and certain at-home medical devices also qualify.

A few things to keep in mind. Health insurance premiums are usually not a qualified expense, with specific exceptions such as Medicare premiums, COBRA coverage while you are unemployed, and long-term care insurance. Cosmetic procedures and general wellness purchases typically do not qualify. And you do not have to spend HSA money in the same year you incur the expense; as long as the expense happened after you opened the account, you can reimburse yourself years later. Keep every receipt, because the burden of proof is on you if the IRS ever asks. When you are unsure whether something qualifies, check Publication 502 at IRS.gov rather than guessing.

Using an HSA as a stealth retirement account

Here is where the HSA gets genuinely powerful. Because unused funds roll over year after year with no expiration, you are not forced to spend the money. Savvy savers do the opposite: they pay small medical bills out of pocket, leave the HSA balance invested, and let decades of tax-free growth compound. The account quietly becomes one of the best retirement vehicles available.

The strategy works because of what happens at age 65. After you turn 65, you can withdraw HSA money for any reason with no penalty. If you use it for a non-medical purpose, the withdrawal is simply taxed as ordinary income, exactly like a traditional IRA distribution. If you use it for medical costs, which tend to rise in retirement, it stays completely tax-free. In effect, an HSA after 65 behaves like a traditional IRA at worst and a Roth IRA at best, giving you flexibility no other account matches.

To use an HSA this way, look at how your provider handles the cash portion of your balance. Many keep a chunk in cash earning interest before you can invest the rest, so it is worth comparing that rate against what you could earn elsewhere; our roundup of the best high-yield savings rates is a useful benchmark for whether your idle HSA cash is pulling its weight. Above the cash threshold, most HSA custodians let you invest in mutual funds or ETFs, which is where the long-term, tax-free compounding really happens.

HSA vs FSA: what is the difference?

HSAs are frequently confused with Flexible Spending Accounts (FSAs). Both let you set aside pre-tax money for medical costs, but the similarities largely end there. The biggest practical difference is what happens to unused money: an FSA is generally “use it or lose it” at year-end (employers may offer a small carryover or grace period), while an HSA balance rolls over in full and belongs to you permanently.

| Feature | HSA | FSA |

|---|---|---|

| Requires an HDHP | Yes | No |

| Unused funds at year-end | Roll over in full | Often forfeited (limited carryover) |

| Who owns the account | You — fully portable | Employer — tied to your job |

| Can you invest the balance? | Usually yes | No |

| Change contributions mid-year | Anytime | Usually only at enrollment |

| Flexibility after age 65 | Withdraw for any reason | Not applicable |

For most people who qualify, the HSA wins on flexibility and long-term value. An FSA can still make sense if you do not have HDHP coverage or you know you will spend the money on predictable costs within the year, but it lacks the rollover and investment features that make the HSA so useful.

Mistakes and scams to watch for

An HSA is a legitimate, IRS-sanctioned account, but a few pitfalls can cost you. First, avoid over-contributing; if you exceed the annual limit, remove the excess before the deadline to sidestep an ongoing excise tax. Second, resist the urge to raid the account for non-medical costs before 65, which triggers both income tax and an additional penalty (verify the current penalty rate at IRS.gov). Third, keep meticulous records of every qualified expense you plan to reimburse later.

Be wary of unsolicited offers promising to “unlock” or “cash out” your HSA for a fee, or apps that ask for your HSA login to “maximize” your account. Real HSA custodians are banks and established financial institutions; you open an account directly, not through a pushy middleman. And never let a medical provider pressure you into paying with a high-interest credit card when your HSA can cover the cost tax-free. If you are already carrying medical debt, our guide to improving your credit score in 2026 walks through handling that debt without derailing your finances.

Frequently asked questions

What happens to my HSA if I switch jobs or lose my HDHP?

The account stays yours no matter what. You keep every dollar and can continue spending it on qualified expenses. The only change is that you cannot make new contributions during any month you are not covered by a qualifying HDHP. If you regain HDHP coverage later, you can resume contributing.

Can I have both an HSA and a 401(k) or IRA?

Yes. An HSA does not count against your 401(k) or IRA contribution limits; they are entirely separate. Many financial planners suggest capturing your employer 401(k) match first, then funding your HSA, because of its unmatched triple tax advantage, before returning to max out other retirement accounts.

Do I lose my HSA money at the end of the year like an FSA?

No. This is the defining difference between the two accounts. HSA funds roll over indefinitely with no expiration, which is exactly what makes the account so effective for long-term saving and investing.

What are the 2026 HSA contribution limits?

The IRS sets separate limits for self-only and family coverage and adjusts them annually, with an extra catch-up amount for people 55 and older. Because the figures change each year, look up the exact 2026 numbers at IRS.gov or in your HSA provider’s app before you contribute.

Can I use my HSA to pay for my spouse’s or child’s medical bills?

Yes. You can use your HSA tax-free for qualified medical expenses of your spouse and any tax dependents, even if they are not covered by your HDHP. The account holder’s eligibility is what determines whether you can contribute, but the money can be spent on your family’s qualified care.

The bottom line

An HSA is one of the few accounts that lets you win on taxes three times over, going in, while it grows, and coming back out for medical care. Pair it with a qualifying high-deductible health plan, contribute what you can within the IRS limits, and, if your budget allows, invest the balance and pay small bills out of pocket so the account can compound into a powerful stealth retirement fund. Just confirm your eligibility and the current-year contribution figures at IRS.gov, keep your receipts, and steer clear of anyone offering a shortcut. Used well, the HSA quietly does more tax-saving work than almost anything else in your financial toolkit.

")

{kind=link}