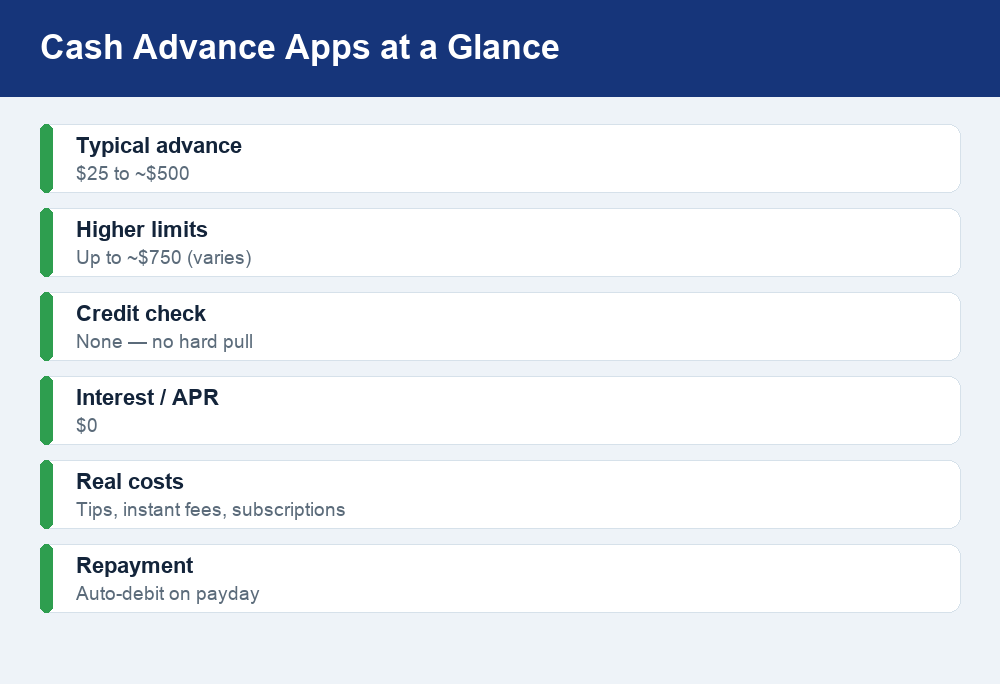

Cash advance apps let you tap a small slice of your paycheck early — usually $25 to a few hundred dollars, and up to roughly $750 with a few apps — with no interest and no hard credit check. Instead of charging APR, they make money from optional tips, instant-transfer fees, or a monthly subscription, so the “free” advance is rarely completely free.

Quick answer: The best-known cash advance apps in 2026 include Dave, Earnin, Brigit, MoneyLion and Current, plus overdraft-style features like Chime SpotMe and short-term loans like Cash App Borrow. Advance amounts vary by app and your account history, and none of them run a hard credit inquiry. There is no set interest rate, but watch for tips, express fees and subscriptions — and never treat an advance as a fix for a shrinking budget. Always confirm the current limits and fees inside each app before you borrow.

How cash advance apps work

A cash advance app (also called a paycheck advance or earned-wage access app) fronts you money you have technically already earned but have not yet been paid. You connect a bank account or your payroll, the app estimates how much of your pay is “safe” to advance, and you get a small amount deposited — often within a day, or within minutes if you pay for instant delivery. When your next paycheck lands, the app automatically debits what you borrowed.

The key difference from a payday loan is the pricing model. A traditional payday lender charges a fee that works out to a triple-digit APR. Most cash advance apps skip interest entirely and instead lean on one of three revenue sources: an optional “tip” the app suggests at checkout, an express or instant-transfer fee if you want the money right away, or a flat monthly membership. Because there is no interest and no hard credit pull, these apps are easy to qualify for — but “easy” is not the same as “free,” and the small charges can add up fast if you use them every pay period.

Eligibility usually depends on things like how long your account has been open, whether you receive regular direct deposits, and your recent account activity — not your FICO score. That is why people with thin or damaged credit often turn to them. Just know that approval and your available amount are never guaranteed; they can change month to month based on your income and repayment history.

What to compare before you pick one

All cash advance apps sound similar in the ads, but the details decide whether one is genuinely useful or quietly expensive. Focus on five things:

- Maximum advance: Many apps start you low (think $25 to $100) and raise your limit as you build history. A few advertise up to around $500–$750, but that top figure is a ceiling, not what you will get on day one.

- Speed and instant fees: Standard transfers are typically free but can take one to three business days. Want it in minutes? Most apps charge an express fee — a small dollar amount that recurs every time you rush a transfer.

- Cost model: Decide whether you would rather pay a monthly subscription (predictable, but you pay even in months you do not borrow) or an optional tip plus express fee (pay-per-use, but easy to overpay).

- Repayment terms: Almost all of these apps auto-debit on your payday. Confirm the date and make sure the withdrawal will not trigger an overdraft on your own bank account.

- Extras and eligibility: Some apps bundle budgeting tools, credit-building features, or a checking account. Others require you to bank with them to get the highest limits.

Because these terms change often, treat every “up to $750” or “no fees” claim as something to verify in the app itself before you commit.

How the main cash advance apps differ

Here is a plain-English comparison of the most popular options in 2026. Amounts and fees are approximate and change frequently, so use this as a starting point and confirm current terms directly with each provider.

| App | Typical advance | Main cost model | Worth knowing |

|---|---|---|---|

| Dave | Up to a few hundred dollars (grows with history) | Small monthly membership + optional tip; express fee for instant | Includes budgeting tools and a spending account |

| Earnin | Based on hours worked, up to a daily/pay-period cap | Optional tip + optional instant fee; no subscription | Best suited to hourly workers with steady schedules |

| Brigit | Up to a few hundred dollars | Monthly subscription; express fee for instant delivery | Bundles budgeting and credit-building features |

| MoneyLion | Varies with account activity | Instant-transfer fee and/or membership tiers | Full mobile banking plus advances in one app |

| Current | Cited up to ~$750 | Advertised with no mandatory fees | Advance is tied to holding a Current account |

| Chime SpotMe | Overdraft-style cushion, not a loan | No fees; optional tip | Requires qualifying direct deposits to unlock |

| Cash App Borrow | Short-term loan (a different product) | Flat finance charge, not a tip | Availability and amount vary by user |

Two of these deserve a caveat because they are not classic paycheck advances. Chime’s overdraft-style feature is closer to fee-free overdraft protection than a loan — our guide to how Chime SpotMe works breaks down the direct-deposit requirements and how your limit grows. And Cash App’s borrowing feature is a small short-term loan with a flat charge rather than an optional tip; if that is what you are considering, read our full walkthrough of Cash App Borrow in 2026 so the finance charge does not surprise you.

The real risks of cash advance apps

Cash advance apps are marketed as a friendly favor, but they carry real downsides worth taking seriously.

The fees are small until they are not. A $3 express fee and a $2 tip feel trivial on a single $100 advance. But if you tip and rush every pay period, you might pay $10 or more a month for the convenience of borrowing your own money — and on a small advance repaid in two weeks, those fees can translate into an effective cost far higher than the “no interest” label suggests. Consumer advocates have pointed out that voluntary tips and express fees, annualized, can rival payday-loan APRs.

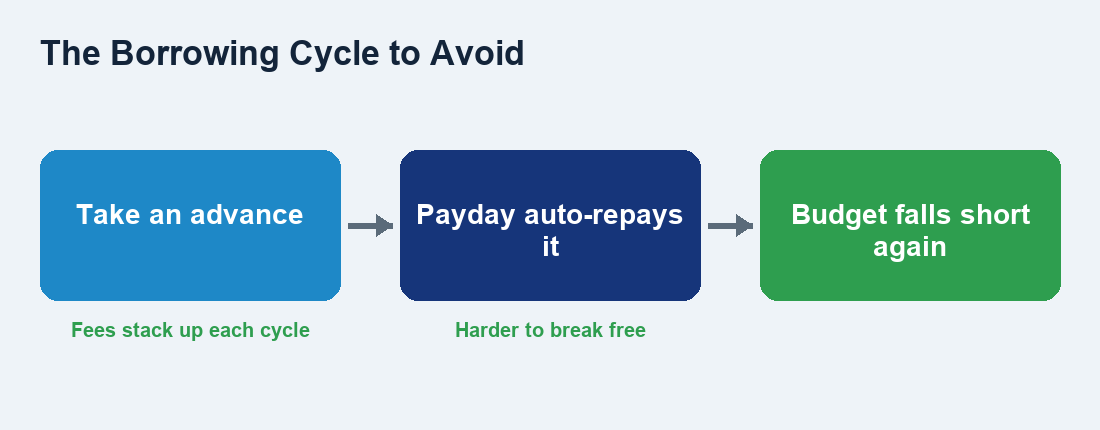

The borrowing cycle is the bigger trap. The moment the app debits your full advance on payday, your paycheck is smaller than usual — which makes it more likely you will come up short again and reach for another advance. That loop can quietly turn a one-time cushion into a monthly habit. If you find yourself advancing every cycle, that is a signal your budget is stretched, not a sign the app is helping. Our guide to breaking the paycheck-to-paycheck cycle covers the budgeting moves that actually reduce your reliance on advances.

Overdraft risk on your own account. Because repayment is automatic, a debit that hits before your deposit clears can bounce and trigger a $35 overdraft fee at your bank — wiping out any savings the “free” advance offered.

Watch for scams and copycats. Only download apps from the official App Store or Google Play, and never pay an upfront “processing fee” to unlock an advance — legitimate apps deduct their costs from the advance or on payday, not before. Any lookalike app demanding gift cards, wire transfers, or a fee to “release” your money is a scam.

Cheaper alternatives to consider first

Before you make advance apps a routine, it is worth knowing what else exists. Depending on your situation, one of these may cost less or leave you in a stronger spot:

- A fee-free overdraft feature. Some checking accounts cover small shortfalls with no fee if you meet a direct-deposit requirement — often cheaper than a paid express transfer.

- An employer earned-wage program. If your job offers on-demand pay through your payroll provider, it is frequently free and repaid straight from your check.

- A small credit-union loan or PAL. Many credit unions offer Payday Alternative Loans with capped fees and longer repayment terms than a two-week advance.

- A 0% credit card intro window. For planned expenses (not emergencies you cannot repay), a card you pay off in full avoids fees entirely.

- Asking for a bill extension. Utilities, landlords and lenders sometimes grant a few extra days at no cost — cheaper than any advance.

Cash advance apps are best used the way a spare tire is used: occasionally, to get through a genuine bump, not as your everyday ride.

Frequently asked questions

Do cash advance apps check your credit?

No. The apps in this guide do not run a hard credit inquiry, so applying will not ding your score. They look at factors like direct-deposit history and account activity instead. That is also why they cannot help you build credit the way a loan or credit card that reports to the bureaus can.

Can I really borrow up to $750?

A few apps, including Current, have been cited for advances up to around $750, but that is a maximum, not a starting amount. New users usually begin with a much smaller limit that increases over time as you repay on schedule. Your actual amount depends on your income and history, so check the figure inside the app rather than relying on the headline number.

Are cash advance apps actually free?

Rarely 100% free. There is no interest, but most apps earn money from optional tips, instant-transfer fees, or a monthly subscription. You can often avoid fees by choosing the standard (slower) transfer and skipping the tip, but if you need the money instantly or the app requires a membership, expect to pay a few dollars each time.

Will using one hurt my credit score?

Using the advance itself will not hurt your score, since these apps generally do not report to the credit bureaus. The indirect risk is overdrafting your bank account when the automatic repayment hits, which can lead to bank fees and, if left unpaid, collection activity that does affect your standing.

How fast does the money arrive?

Standard transfers typically take one to three business days and are usually free. If you need funds within minutes, most apps offer an instant option for an express fee. If you can wait, choosing the free standard transfer is the cheapest way to use these apps.

The bottom line

Cash advance apps like Dave, Earnin, Brigit, MoneyLion and Current can be a low-drama way to cover a short gap without interest or a credit check — and a couple advertise advances as high as $750. The catch is that “no interest” does not mean no cost: tips, express fees and subscriptions add up, and automatic payday repayment can nudge you into borrowing again and again. Use them sparingly, choose the free transfer option when you can, verify the current limits and fees in the app before you tap Borrow, and put your energy into the budgeting and alternatives that shrink your need for an advance in the first place.

")

{kind=link}