")

Yes, the Chime Credit Builder Visa can build your credit. It is a secured credit card that reports your on-time payments to all three major credit bureaus, and it does this without an annual fee, without interest, and without a traditional hard credit check to apply.

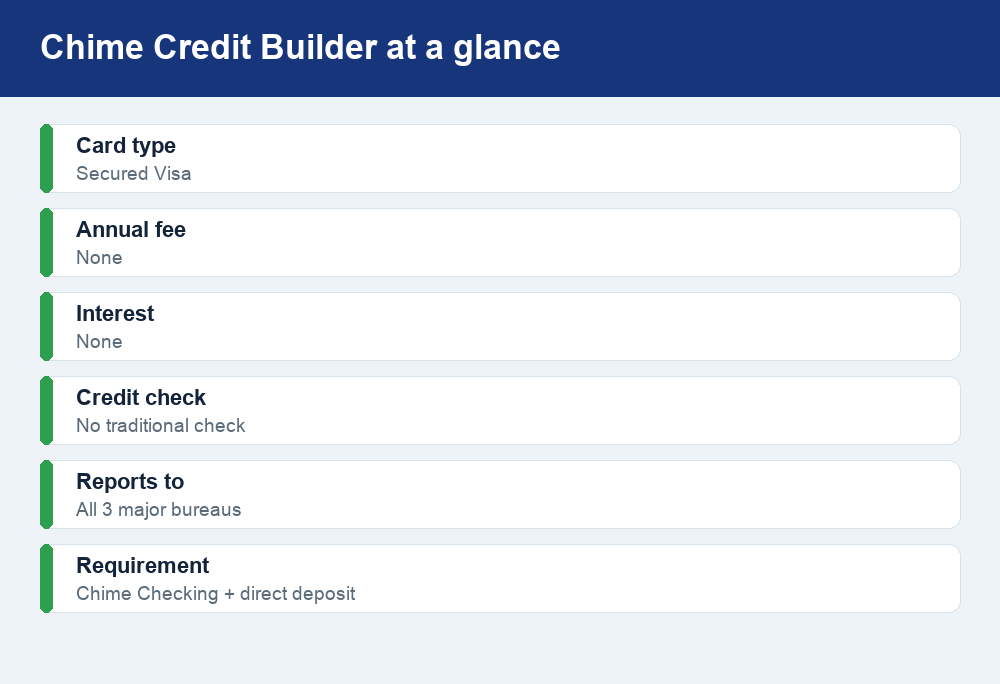

Quick answer: The Chime Credit Builder card is a secured Visa tied to your Chime Checking Account. Instead of a fixed deposit, you move money from checking into a secured account, and that amount becomes your spending limit. Chime reports your payment activity to Equifax, Experian, and TransUnion, so paying on time helps build credit history. There is no annual fee, no interest, and no minimum security deposit in the usual sense. Always confirm current terms at chime.com.

What is the Chime Credit Builder card?

The Chime Credit Builder Visa is a secured credit card built for one main purpose: helping people establish or rebuild credit history. Unlike a rewards card that hands out points and tempts you to spend, this card is deliberately simple. It is designed so that responsible everyday use turns into a positive credit record over time.

What makes it different from a standard credit card is how the “credit” part works. With most cards, the issuer extends you a line of credit and charges interest if you carry a balance. With the Chime Credit Builder card, you are essentially spending money you have already set aside. You move funds from your Chime Checking Account into a linked secured account, and that money backs your purchases. Because you fund it yourself, Chime does not need to run a traditional credit check to approve you, which is a big deal for people with thin credit files or past credit trouble.

Three features stand out compared to many secured cards on the market:

- No annual fee. You are not paying a yearly charge just to hold the card.

- No interest. Because you spend money you have already moved into the secured account, there is no revolving balance accruing interest.

- No minimum security deposit in the traditional sense. You are not forced to lock up a fixed amount like $200 or $500 upfront; instead, the amount you transfer becomes your available-to-spend limit.

How the Chime Credit Builder card works, step by step

The mechanics feel familiar if you have used a debit card, but the credit-reporting layer is what sets it apart. Here is the typical flow:

- Open and qualify. You generally need a Chime Checking Account with a qualifying direct deposit before you can access the Credit Builder card. This is the eligibility gate, so setting up direct deposit is usually the first practical step.

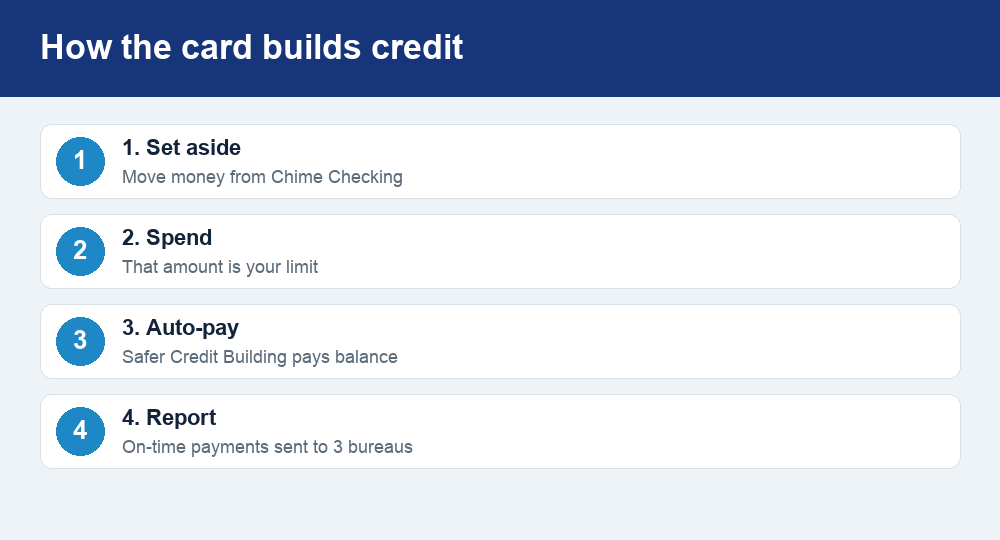

- Move money in. You transfer money from your Chime Checking Account into the secured Credit Builder account. There is no set minimum in the way a classic secured card demands, and the amount you move becomes your spending limit.

- Spend like a normal card. You use the Visa card at stores and online. Purchases draw against the money you set aside, so you can only spend what you have already added.

- Chime reports your activity. Each month, Chime reports your payment behavior to Equifax, Experian, and TransUnion. On-time payments are what build a positive history.

- Your balance gets paid. You can pay manually, or you can turn on the “Safer Credit Building” feature, which automatically pays your balance using the money you set aside. That automation is designed so you do not accidentally miss a payment.

The “Safer Credit Building” setting is arguably the smartest part of the design. Missed payments are one of the fastest ways to damage a credit score, and this feature removes most of that risk by paying the balance from money you have already committed. For a fuller game plan on raising your number over time, our guide on how to improve your credit score in 2026 pairs well with using a card like this.

Does the Chime Credit Builder card actually build credit?

Yes, it can, and the reason is mechanical rather than magical. Credit scores are largely driven by your payment history and how much of your available credit you use. Because Chime reports the Credit Builder card to all three major bureaus, the account shows up on your credit reports and your on-time payments become part of your record.

Payment history is the single largest factor in most credit-scoring models, so consistently paying on time is exactly what this card is built to help you do. The card does not guarantee a specific score increase, and no honest company can promise an exact number of points. Results depend on your overall credit profile, other accounts, and how you use the card. But the foundation, on-time reporting to all three bureaus, is the right one.

A quick reality check: building credit is a slow, steady process. You will not see meaningful changes overnight. Think in terms of months of consistent, on-time activity, not days.

How it differs from a normal secured credit card

Both this card and a traditional secured card use your own money as backing, but the details differ in ways that matter for your wallet. The table below lays out the main contrasts.

| Feature | Chime Credit Builder | Typical traditional secured card |

|---|---|---|

| Security deposit | Move money from Chime Checking; that amount is your limit | Fixed upfront deposit, often $200 minimum |

| Credit check to apply | No traditional credit check | Often a hard credit inquiry |

| Interest | None | APR applies if you carry a balance |

| Annual fee | None | Varies; some charge a fee |

| Reports to all 3 bureaus | Yes | Usually, but confirm per issuer |

| Account requirement | Chime Checking + qualifying direct deposit | Usually a standalone card |

The biggest practical difference is flexibility. A traditional secured card usually locks up a fixed deposit and charges interest if you carry a balance. The Chime card lets your set-aside amount flex with what you move over, avoids interest entirely, and skips the annual fee. The trade-off is that it lives inside the Chime ecosystem, so you need a Chime Checking Account and a qualifying direct deposit to use it.

Pros and cons of the Chime Credit Builder card

No product is perfect for everyone. Here is a balanced look before you decide.

Pros

- No annual fee and no interest. You are not paying to hold the card or to carry a balance.

- No traditional credit check to apply, which helps people with limited or damaged credit get started.

- Reports to all three bureaus, so responsible use shows up broadly.

- “Safer Credit Building” automation reduces the risk of missed payments.

- No fixed minimum deposit, so you control how much you set aside.

Cons

- Requires a Chime Checking Account with a qualifying direct deposit. If your paycheck is not set up for direct deposit, this is a hurdle.

- You can only spend money you have already moved over, so it does not extend true credit to bridge a shortfall.

- It builds credit but does not earn rewards the way many mainstream cards do.

- Terms and eligibility can change, so you should verify current details at chime.com before applying.

Tips to maximize the credit-building benefit

Owning the card is only half the equation. How you use it determines how much it helps.

- Always pay on time. Payment history carries the most weight in credit scoring. Turning on “Safer Credit Building” so the balance is paid automatically from your set-aside money is the simplest way to never slip.

- Keep utilization low. Utilization is how much of your available limit you are using. A common rule of thumb is to keep it well under 30 percent, and lower is generally better. If you moved over $300, try not to let your reported balance creep near that cap.

- Use it regularly, but modestly. Small, routine purchases like a streaming subscription or a tank of gas keep the account active and generate the on-time payment history you want, without overspending.

- Do not close it prematurely. The length of your credit history matters. Keeping the account open and in good standing over time helps more than opening and closing accounts.

- Check your credit reports. Confirm your Chime activity is reporting correctly. You are entitled to free reports, and reviewing them helps you catch errors early.

If you like keeping your money inside one app, it is worth understanding the rest of the Chime toolkit too. Our explainer on how Chime SpotMe works covers the fee-free overdraft feature, and if you want your set-aside cash to earn while you build credit, see our look at Chime’s high-yield savings account.

Watch out for scams and lookalikes

Because Chime is popular, it attracts imposters. Chime will never ask for your password, PIN, or one-time verification code over the phone, text, or social media. If someone contacts you claiming to be Chime support and asks you to move money, share a code, or “verify” your account through a link, treat it as a scam. Only download the Chime app from official app stores, and only enter your login details at chime.com or in the app you installed. When in doubt, close the message and reach out through the contact options listed inside the official app.

Frequently asked questions

Does the Chime Credit Builder card require a credit check?

No. There is no traditional credit check to apply, which is one reason it is accessible to people with limited or damaged credit. You do, however, generally need a Chime Checking Account with a qualifying direct deposit to be eligible.

How quickly will my credit score go up?

There is no fixed timeline, and no card can promise a specific point increase. Credit building is gradual and depends on your whole credit profile. Consistent on-time payments over several months are what move the needle, so patience and consistency matter most.

Is there a minimum deposit to open the card?

Not in the traditional sense. Instead of locking up a fixed deposit, you move money from your Chime Checking Account into the secured Credit Builder account, and that amount becomes your available-to-spend limit. You decide how much to set aside.

Will I pay interest or an annual fee?

No. The card charges no interest and no annual fee. Because you spend money you have already moved into the secured account, there is no revolving balance to accrue interest. Always confirm the latest terms at chime.com, since features and fees can change.

Can I use the card anywhere?

It is a Visa card, so you can use it at merchants that accept Visa, in stores and online. Just remember you can only spend the money you have already transferred into the secured account, so add funds before you plan to make purchases.

The bottom line

The Chime Credit Builder Visa is a genuinely useful tool for building or rebuilding credit, especially if you already bank with Chime. By reporting on-time payments to all three bureaus with no annual fee, no interest, and no traditional credit check, it lowers the barriers that keep many people out of the credit system. Its automation feature makes missed payments far less likely, which is exactly what a credit-building card should do. To get the most from it, pay on time, keep your utilization low, and use it consistently over the long haul. And because features and eligibility rules can shift, always verify the current terms directly at chime.com before you apply.

{kind=link}