")

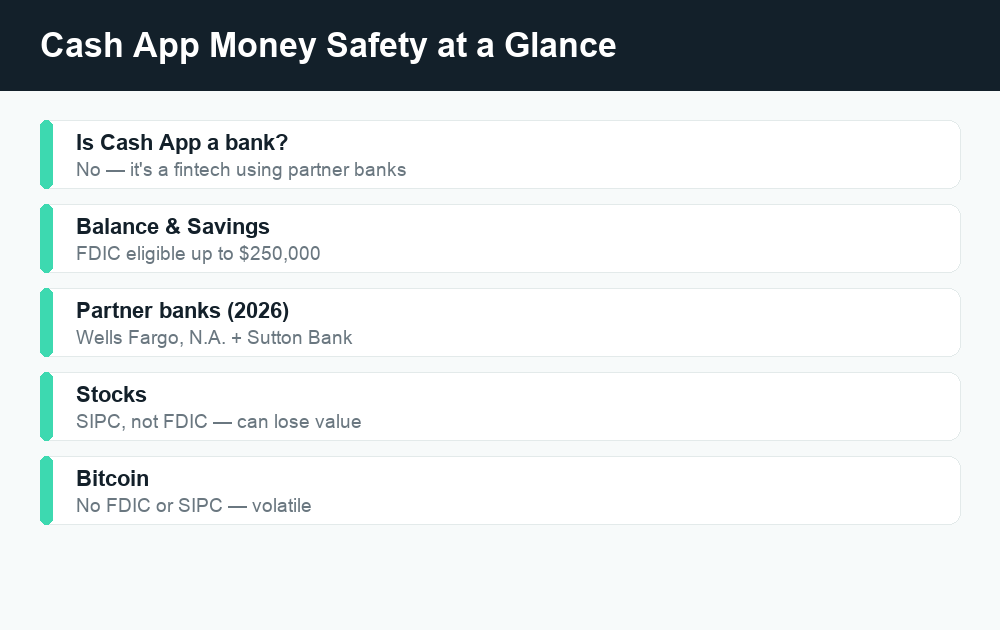

If you’re wondering is Cash App FDIC insured, here’s the short version: yes — the cash in your Cash App balance and Cash App Savings is eligible for FDIC insurance up to $250,000, but only through Cash App’s partner banks, and only if you’ve activated your free Cash App Card. Cash App itself is a financial technology company, not a bank, so the actual insurance comes from the FDIC-member banks that hold your money behind the scenes.

That distinction matters more than most people realize. The protection is real, but it does not cover everything inside the app — your stocks and your Bitcoin are not FDIC insured at all. Below, we’ll break down exactly what’s protected, what isn’t, how the “pass-through” insurance actually works, and the practical steps you can take to keep your money safe.

Quick answer: Cash App is not a bank, but the money in your Cash App balance and Cash App Savings is covered by FDIC pass-through insurance — up to $250,000 per person — through its partner banks (currently Wells Fargo Bank, N.A. and Sutton Bank, both FDIC members), as long as you’ve activated your Cash App Card. Stocks held through Cash App Investing and Bitcoin are not FDIC insured and can lose value.

Is Cash App FDIC insured? The honest answer

Cash App is a product of Block, Inc. (the company formerly known as Square). It is a “fintech” — a financial technology company — not a chartered bank. On its own, a fintech app cannot hold FDIC insurance, because the FDIC only insures deposits held at member banks.

So how can your Cash App money be insured? Through an arrangement called pass-through FDIC insurance. When you load money into Cash App, that money doesn’t sit inside the app like a video-game balance. It gets placed on deposit at one or more real, FDIC-member partner banks. Because those banks are insured, the protection “passes through” to you, the individual customer — provided certain conditions are met.

The key takeaways:

- Your stored cash balance and Cash App Savings are eligible for FDIC coverage up to $250,000, held through partner banks.

- You generally need to have activated your Cash App Card for the pass-through insurance on your balance to apply. If you’ve never ordered or activated the card, confirm your coverage status in the app.

- Investing and Bitcoin are different products with their own (non-FDIC) protections, which we’ll cover below.

What “FDIC insured” actually means

The Federal Deposit Insurance Corporation (FDIC) is a U.S. government agency created during the Great Depression. It insures deposits at member banks so that if an insured bank fails, eligible depositors are protected — currently up to $250,000 per depositor, per insured bank, per ownership category.

A few things FDIC insurance is — and isn’t:

- It protects against bank failure, not against you losing money to a scam, a bad investment, or a payment you sent to the wrong person.

- It covers deposit products — checking, savings, money market deposit accounts, and CDs. It does not cover investments like stocks, bonds, mutual funds, or crypto.

- The $250,000 limit is per bank. If you hold money at the same bank both directly and indirectly (for example, through Cash App’s partner bank and a personal account at that same bank), the totals can count together toward one limit.

This is why understanding which bank holds your Cash App money is more than a trivia question.

Which banks insure Cash App money?

Cash App works with FDIC-member partner banks to hold customer funds and issue the Cash App Card. As of 2026, Cash App’s banking services are provided through Wells Fargo Bank, N.A. and Sutton Bank, both FDIC members. The Cash App Card is issued by Sutton Bank, and balances are held at partner banks where pass-through FDIC insurance can apply.

Partner-bank relationships can change over time, so the most reliable place to confirm the current banks is Cash App’s own disclosures inside the app and on cash.app. If you happen to already bank directly with one of these institutions, keep the $250,000-per-bank rule in mind, because deposits at the same bank can be aggregated for insurance purposes.

What’s covered vs. what’s not

This is the single most important table in this article. Not everything inside Cash App is a “deposit,” and the protections vary a lot by product.

| Inside Cash App | FDIC insured? | What protects it |

|---|---|---|

| Cash App balance (stored cash) | Yes (pass-through, with activated Cash App Card) | FDIC, via partner banks, up to $250,000 |

| Cash App Savings | Yes (pass-through) | FDIC, via partner banks, up to $250,000 |

| Stocks (Cash App Investing) | No | SIPC coverage of the brokerage; value can still rise or fall |

| Bitcoin | No | No FDIC or SIPC; price is volatile and can drop |

| Money in transit / pending | Depends | Confirm status in-app; see our pending-payment guide |

Covered: your cash balance and savings

The dollars you keep in your Cash App balance and in Cash App Savings are the part that benefits from FDIC pass-through insurance. If a partner bank holding that money were to fail, eligible funds would be protected up to the $250,000 limit. This is the same federal protection a traditional checking or savings account gets.

Not covered: stocks

When you buy stocks through Cash App Investing, you’re using a brokerage service (Cash App Investing LLC, a registered broker-dealer and member of FINRA/SIPC), not a bank. Brokerage accounts are protected by SIPC, not the FDIC. SIPC protects against the failure of the brokerage firm itself (for example, if the firm goes under and your shares go missing) — but it does not protect you from investment losses. If a stock you bought drops in value, that’s normal market risk, and no insurance covers it.

Not covered: Bitcoin

Bitcoin held in Cash App is not a bank deposit and not a security, so it has neither FDIC nor SIPC coverage. Crypto is volatile, and its price can fall sharply. Treat any Bitcoin balance as an investment you could lose, not as insured savings.

How Cash App’s pass-through insurance actually works

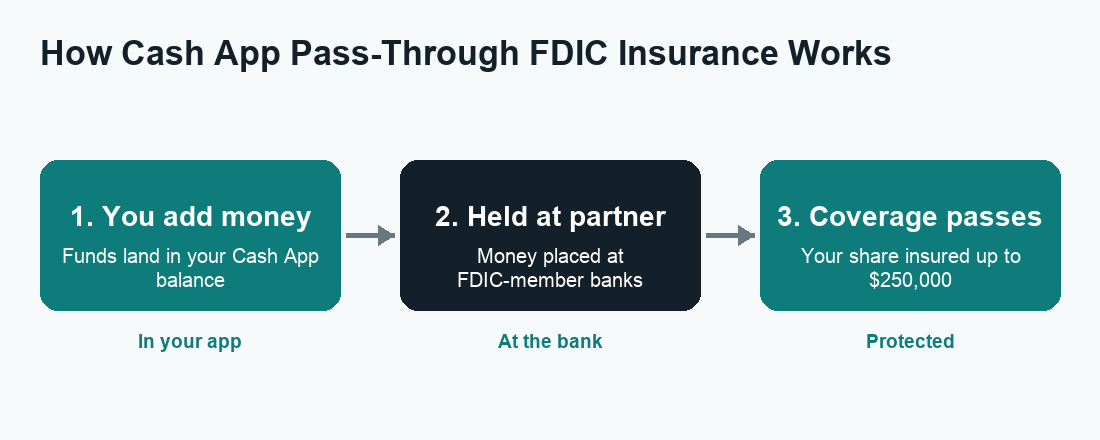

It helps to picture the flow of your money in three stages:

- You add or receive money. Funds land in your Cash App balance.

- Cash App places those funds with partner banks. Your money is held in deposit accounts at FDIC-member banks, often in pooled “for-benefit-of” (FBO) accounts that track how much belongs to each customer.

- Insurance passes through to you. Because the FDIC looks through to the individual owner of the funds, your share is eligible for the standard $250,000 of coverage — as if you held the money at that bank directly.

For pass-through insurance to work, the records must clearly show that the money is held for individual customers and how much each person owns. Cash App and its partner banks handle that record-keeping. The main thing on your end is having an activated Cash App Card, which is the trigger that establishes the bank relationship for your balance.

A quick word on what FDIC insurance does NOT save you from

Even with full FDIC coverage on your balance, that insurance only kicks in if a bank fails. It will not refund you if:

- You send money to a scammer or the wrong person.

- Someone gains access to your account and drains it.

- You authorize a payment you later regret.

For everyday safety, the bigger risk by far is fraud — not a partner bank collapsing. That’s where the next sections come in.

How to keep your money safe in Cash App

FDIC insurance is your safety net for the rare event of bank failure. These habits protect you from the far more common threats. Here’s a practical checklist:

- Turn on the Security Lock. Require a PIN, Touch ID, or Face ID for every payment in your in-app security settings.

- Enable login and payment notifications. Getting a text or email for each sign-in and transaction means you’ll spot anything unauthorized fast.

- Only send money to people you know and trust. Cash App payments are like cash — fast and often hard to reverse. If a “deal” pushes you to pay a stranger, walk away.

- Never share your PIN, sign-in code, or full card number. Cash App support will never ask for these. Anyone who does is a scammer.

- Use the verified support channels only. Search for support inside the app or on the official cash.app site. Fake “Cash App support” phone numbers and social-media accounts are a common scam.

- Don’t keep your life savings in any payment app. Even though balances are FDIC eligible, a high-yield bank or insured brokerage may be a better home for large sums you don’t need day to day.

- Move large balances to a linked bank. If you’re holding well over what you need for spending, cash out to your bank account.

Watch for these scam red flags

Most “Cash App is not safe” stories are really fraud stories. The protection on your money is solid; the danger is being tricked into sending it. Be suspicious of anyone who contacts you out of the blue asking you to send a payment to “verify your account,” “claim a prize,” or “fix” a problem — and of any too-good-to-be-true giveaway. When in doubt, stop and confirm through official channels.

Cash App vs. Venmo vs. Zelle: how insurance compares

Cash App isn’t unique here. Most peer-to-peer apps are fintechs that rely on partner banks for FDIC pass-through insurance on stored balances. The general picture:

| App | Stored balance FDIC eligible? | How money is held |

|---|---|---|

| Cash App | Yes (pass-through, with activated card) | Partner banks (Wells Fargo, Sutton Bank) |

| Venmo | Yes (pass-through, generally with the Venmo Debit Card / direct deposit set up) | Partner bank(s) |

| Zelle | N/A — no stored balance | Moves money bank-to-bank; nothing is “held” in Zelle |

Zelle is the odd one out: it doesn’t hold a balance at all, so there’s nothing to insure — money moves directly between linked bank accounts (which are themselves FDIC insured at your bank). If you want to dig deeper, see our guides on Venmo fees and whether Zelle is safe. Always confirm each app’s current terms, since partner banks and activation rules change.

Should you trust Cash App with your money?

For everyday spending, sending, and modest savings, Cash App’s setup is genuinely safe: your cash balance and savings are eligible for the same $250,000 FDIC protection a bank account gets, just delivered through partner banks. The realistic risks aren’t about that insurance — they’re about scams, account takeover, and the fact that stocks and Bitcoin inside the app can lose value.

The smart approach is simple: use Cash App for what it’s great at (fast, free person-to-person payments and a debit card), keep your balance modest, lock down your account security, and house large savings in a dedicated insured account. Do that, and “is my money safe in Cash App?” becomes an easy yes.

Frequently asked questions

Is Cash App FDIC insured up to $250,000?

Yes. The money in your Cash App balance and Cash App Savings is eligible for FDIC pass-through insurance up to $250,000 per person, held through partner banks, provided you’ve activated your Cash App Card. Stocks and Bitcoin are not covered by FDIC insurance.

Is Cash App a real bank?

No. Cash App is a financial technology company (a product of Block, Inc.), not a chartered bank. It partners with FDIC-member banks — currently Wells Fargo Bank, N.A. and Sutton Bank — which hold customer funds and provide the banking services behind the app.

What happens to my Cash App money if the bank fails?

If a partner bank that holds your funds were to fail, your eligible balance would be protected by FDIC pass-through insurance up to the $250,000 limit, the same as a traditional bank deposit. FDIC insurance only applies to bank failure, not to scams or unauthorized transfers.

Is my Bitcoin on Cash App insured?

No. Bitcoin is neither FDIC insured nor SIPC protected. It’s a volatile asset whose price can rise or fall significantly, so only hold what you’re prepared to see drop in value.

Are stocks I buy on Cash App insured?

Stocks bought through Cash App Investing are covered by SIPC, not the FDIC. SIPC protects against the failure of the brokerage firm — it does not protect you from normal investment losses if a stock’s price falls.

Do I need to activate my Cash App Card to be insured?

Generally, yes. Activating your free Cash App Card is what establishes the partner-bank relationship that makes pass-through FDIC insurance apply to your balance. If you’ve never activated a card, confirm your current coverage status inside the app.

How is Cash App’s insurance different from Zelle’s?

Cash App holds a stored balance that’s FDIC eligible through partner banks. Zelle doesn’t hold any balance — it moves money directly between linked bank accounts, which are insured at your own bank. There’s simply nothing for Zelle to insure on its end.

How can I keep my Cash App money safest?

Turn on the in-app Security Lock and notifications, never share your PIN or sign-in codes, only pay people you trust, use official support channels, and move large savings to a dedicated bank or insured account rather than leaving big sums in any payment app.

Last updated: June 2026. Fees, limits, and features can change — always confirm current details in the app. WalletWisp is an independent guide and is not affiliated with any app mentioned. This article is general information, not financial advice.

Related: Cash App fees explained, Why is my Cash App payment pending?, and more Cash App guides.

")

")

{kind=link}