If a stranger, a “bank fraud department,” or anyone pressuring you for speed asks you to send money through Cash App, Venmo, or Zelle, stop — it is almost certainly a scam. Peer-to-peer (P2P) payments are usually instant and irreversible, so once the money leaves your account, getting it back is hard and often impossible.

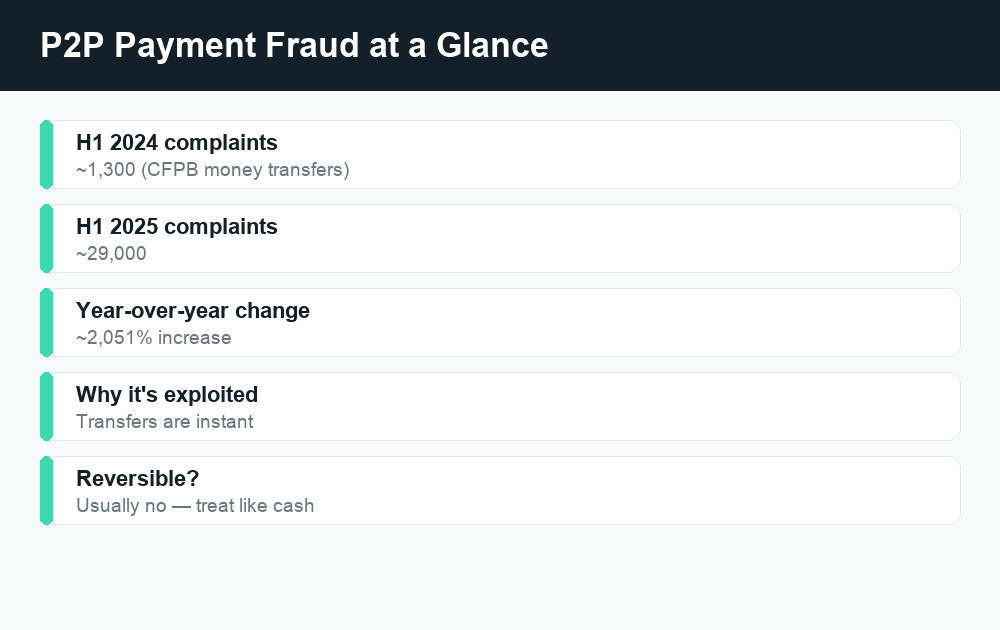

Quick answer: P2P payment fraud has exploded — complaints filed with the Consumer Financial Protection Bureau (CFPB) under domestic money transfers jumped to roughly 29,000 in the first half of 2025, up from about 1,300 a year earlier, a roughly 2,051% increase. Scammers exploit the fact that Zelle, Cash App, and Venmo transfers clear instantly and can’t be reversed. Protect yourself by treating these apps like cash: never pay strangers, always verify requests independently, and never act under pressure. If you’re scammed, contact the app and your bank immediately, then file reports with the FTC and CFPB.

Peer-to-peer payment apps have become the default way millions of Americans split rent, pay a babysitter, or send a friend gas money. They’re fast, free, and convenient. But that same speed is exactly what fraudsters love — and the numbers show they’ve noticed. This guide walks through the most common P2P scams circulating in 2026, the red flags that should make you stop cold, simple rules to keep your money safe, and the steps to take if you’ve already lost money.

Why P2P scams are surging

The scale of the problem is hard to overstate. Complaints filed with the CFPB under the domestic money-transfers category climbed to roughly 29,000 in the first half of 2025, compared with about 1,300 in the same period of 2024. That’s an increase of approximately 2,051% year over year — a more than twentyfold jump in a single year.

The core reason scammers favor these apps is structural: most P2P transfers are instant and irreversible. Unlike a credit card charge, which you can dispute, or a check, which can take days to clear, a Zelle, Cash App, or Venmo payment to a stranger typically can’t be clawed back once you hit send. There’s no “undo” button. Fraudsters engineer their entire playbook around getting you to push money out before you have time to think.

It’s worth being clear about how these networks differ, because the rules around fraud reimbursement aren’t identical:

| App | Linked to | Speed | Reversible? |

|---|---|---|---|

| Zelle | Your bank account directly | Usually instant | No, once sent |

| Cash App | Cash balance, linked bank/card | Instant (standard) | No, once sent |

| Venmo | Venmo balance, linked bank/card | Instant or 1–3 days | No, once sent |

One critical distinction: federal protections that cover unauthorized transactions generally do not cover payments you were tricked into making yourself. If a scammer hacks your account and sends money without your permission, that’s an unauthorized transaction and you may have recourse. But if a con artist convinces you to send the money — even under false pretenses — many platforms treat it as an authorized payment, and reimbursement is far less certain. Policies are evolving and vary by provider, so always check the app’s current help center and your bank’s terms. The safest assumption is simple: treat every P2P payment as final.

The most common P2P payment scams

Scams mutate constantly, but nearly all of them fall into a handful of recognizable patterns. Learn these and you’ll spot most fraud before it costs you.

1. Impersonation scams (bank, government, or utility)

This is one of the most damaging categories. A caller, texter, or emailer pretends to be from your bank’s “fraud department,” the IRS or Social Security Administration, your power company, or even a well-known retailer. The hook is usually urgency and fear: there’s “suspicious activity” on your account, you “owe back taxes,” or your electricity will be “shut off within the hour” unless you pay immediately.

The fraudster then instructs you to “protect” your money by moving it via Zelle or sending a payment through Cash App. Here’s the truth: no legitimate bank, government agency, or utility will ever ask you to send money to yourself or to them through a P2P app to “verify” or “secure” your account. The IRS does not demand payment by Cash App or Venmo. The Social Security Administration will not call to threaten you. If you get a call like this, hang up and call the organization back using the number on the back of your card, your paper bill, or the official website (such as IRS.gov or SSA.gov) — never a number the caller gives you.

2. The “accidental payment” or overpayment trick

You receive an unexpected payment, then a frantic message: “Sorry, I sent that to the wrong person — can you send it back?” It feels like the honest thing to do. But the original “payment” is often fraudulent — funded by a stolen card or hacked account. When the real owner reports it, the platform claws back that money, but the funds you sent from your own balance are gone for good. You’re left covering the loss.

Never return money from an unexpected payment by sending a new payment. If money truly arrives by mistake, contact the app’s support and let them reverse it. Don’t act as the middleman.

3. Fake marketplace buyers and sellers

Whether you’re buying concert tickets, a puppy, or a used couch on social media or a classifieds site, P2P payments are a magnet for scams. A fake seller takes your Cash App or Zelle payment and vanishes — no product ever ships. A fake buyer may “overpay” and ask for the difference back (see the overpayment trick above), or send a fake payment-confirmation screenshot and pressure you to ship before the money actually lands.

The rule of thumb: P2P apps offer little to no buyer protection for goods. Venmo and Cash App have specific protected-purchase or “business” payment options in some cases, but a standard person-to-person payment to a stranger you met online carries essentially no safety net. For anything meaningful, use a payment method with real buyer protection, and never ship or release goods based on a screenshot alone — confirm the money is actually in your account.

4. Romance and investment scams (“pig butchering”)

These are the slow, devastating ones. A stranger builds a relationship with you over weeks or months — a romantic interest from a dating app, or a friendly “wrong number” text that turns into daily chats. Eventually they introduce a “can’t-miss” investment, often involving crypto, and walk you through sending money via P2P apps or a crypto exchange. The fake platform shows your “balance” growing, which encourages you to send more. When you try to withdraw, you’re hit with “taxes” or “fees” — and then the money, and the person, disappear.

The grim nickname “pig butchering” refers to “fattening up” the victim with affection and fake gains before the slaughter. Red flag: anyone you’ve only met online who steers the conversation toward money or investing is a scammer, no matter how genuine they seem. Never invest because someone you met online told you to.

5. “Send to yourself” verification scams

A scammer posing as customer support or your bank claims they need you to “verify” your account by sending yourself a payment, entering a code, or approving a request. In reality, those steps move money to the scammer or hand over access to your account. Sending money to “yourself” to prove anything is never a real security step. Likewise, never share a one-time passcode (OTP) sent to your phone — those codes exist precisely to keep other people out of your account.

Red flags that should make you stop

Most scams share the same DNA. If you notice any of these, pause and verify before sending a cent:

- Urgency and pressure. “Act now,” “your account will be locked,” “the deal expires in 10 minutes.” Real institutions give you time.

- Unusual payment demands. Being told to pay a bill, fine, or tax specifically by Cash App, Venmo, Zelle, gift cards, or crypto is a near-certain sign of fraud.

- Requests to keep it secret or to not tell your bank or family.

- An inbound contact you didn’t initiate — a call, text, or DM claiming to be support, your bank, or a government agency.

- “Send money to yourself” or “verify with a code.” Legitimate verification never works this way.

- An offer too good to be true — guaranteed returns, free money, or a price far below market.

- A relationship that turns to money. Anyone online who eventually asks for funds or investment.

How to protect yourself: simple rules

You don’t need to be a security expert to stay safe. A handful of habits will block the vast majority of P2P fraud.

- Treat P2P payments like cash. If you’d hesitate to hand a stranger a stack of $20 bills, don’t send them a P2P payment. There’s no take-backs.

- Only pay people you know and trust. Use these apps for friends, family, and known merchants — not strangers from the internet.

- Verify every request independently. Got a “fraud alert” call? Hang up and call the number on your card. Got a payment request from a friend that feels off? Text or call them directly to confirm — their account may be hacked.

- Never share codes or login details. No real company will ask for your OTP, PIN, or password.

- Double-check the recipient. Confirm the username, phone number, or email before sending. P2P payments to the wrong person are usually unrecoverable too.

- Turn on every security feature. Enable a PIN or biometric lock on the app, set up account alerts, and use a strong, unique password plus two-factor authentication.

- Slow down. Scammers weaponize urgency. Giving yourself even five minutes to think breaks most schemes.

What to do if you’ve been scammed

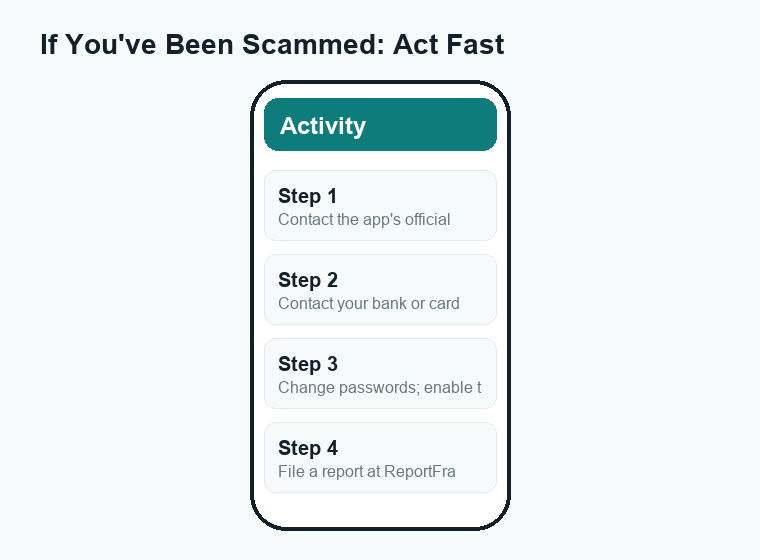

If you realize you’ve sent money to a scammer, act fast — speed occasionally helps, even though recovery is never guaranteed. Be honest with yourself about the odds: because P2P transfers are designed to be final, getting your money back is often difficult and sometimes impossible. Still, take every step below, because it can help in some cases and it builds a record that aids investigators.

- Contact the payment app immediately. Report the fraud through Cash App, Venmo, or Zelle’s official help channels (in-app or on their verified websites) and ask them to attempt a reversal or freeze. Do not search for “support numbers” online — fake support lines are themselves a common scam.

- Contact your bank or card issuer right away. If the payment was funded by your bank account or card, your bank may be able to help, especially if the transaction was unauthorized. Ask about disputing the charge and securing your account.

- Change your passwords and secure your accounts. If you shared any login details or codes, update your passwords immediately and enable two-factor authentication.

- File a report with the FTC. Report the scam at ReportFraud.ftc.gov. Your report helps law enforcement track patterns even when individual recovery isn’t possible.

- File a complaint with the CFPB. Submit a complaint at consumerfinance.gov. The CFPB forwards complaints to the company and can prompt a formal response.

- Keep records. Save screenshots, transaction IDs, dates, usernames, and any messages. You’ll need them for every report.

A word of realism: many victims do not recover their funds. That’s not a reason to skip reporting — reports help shut down scammers and may be your only path to any resolution — but it is the reason prevention matters so much more than cure with P2P payments.

Frequently asked questions

Can I get my money back after a Zelle, Cash App, or Venmo scam?

Sometimes, but often not. If the transaction was truly unauthorized (someone accessed your account without permission), you may have protection under federal rules and your bank or the app may reimburse you. But if you were tricked into sending the money yourself, it’s usually treated as an authorized payment and recovery is much harder. Reimbursement policies vary by provider and are changing, so report it immediately and check the app’s current help center.

Will my bank or the IRS ever ask me to pay through a P2P app?

No. Legitimate banks, the IRS, the Social Security Administration, and utility companies will never ask you to send money via Cash App, Venmo, Zelle, gift cards, or cryptocurrency to “verify,” “protect,” or “secure” your account, or to pay a debt on the spot. Any such request is a scam. Verify by calling the organization at its official number.

Is it safe to use these apps to buy things from strangers online?

Generally, no. Standard person-to-person payments offer little or no buyer protection, so a scam seller can simply take your money and disappear. For purchases from people you don’t know, use a payment method with real fraud protection, and never release goods or ship an item based on a screenshot — confirm the money is actually in your account first.

Someone sent me money by “accident” and wants it back. What should I do?

Don’t send a new payment to return it. The original payment may be fraudulent and will be clawed back, leaving you out the money you sent. Instead, contact the app’s official support and let them reverse the transaction. Never act as the go-between for an unexpected payment.

What’s the single best way to avoid P2P scams?

Treat every P2P payment like handing over cash: only send to people you know and trust, never pay under pressure, and always verify any unexpected request through a separate, official channel before sending. Slowing down for even a few minutes defeats most scams.

The bottom line

P2P apps are genuinely useful, but the roughly 2,000% spike in complaints is a loud warning: scammers have made these instant, irreversible payments their favorite tool. The good news is that the same handful of red flags — urgency, unusual payment demands, “send to yourself” tricks, and money requests from strangers — show up again and again. Treat every payment like cash, verify independently, and never let anyone rush you. If you do get hit, move fast and report it to the app, your bank, the FTC, and the CFPB, while being realistic that recovery is hard.

For more on staying safe and getting the most from these apps, explore our related WalletWisp guides to Cash App, Venmo, and Zelle, including how to secure your account and use each app’s protective features.

")

")

")

{kind=link}