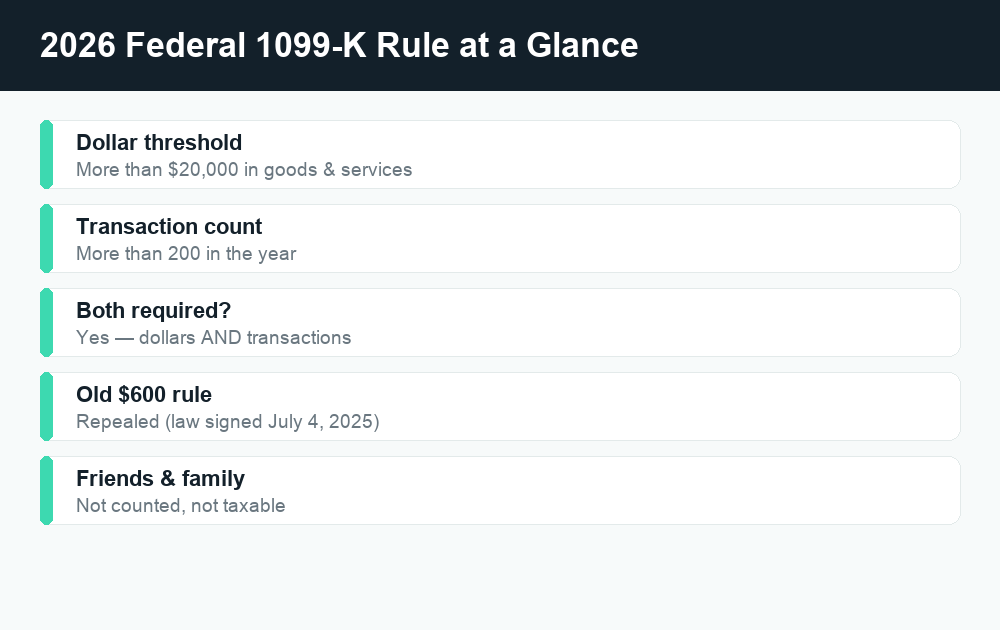

For 2026, most people will not get a federal 1099-K from Cash App, Venmo or PayPal. Thanks to a 2025 law, the old $600 reporting threshold is gone, and the original federal rule is back: an app sends you a 1099-K only when your payments for goods and services top $20,000 AND more than 200 transactions in a year.

Quick answer: The “One Big Beautiful Bill Act” signed July 4, 2025 repealed the $600 1099-K threshold and restored the original federal limit of more than $20,000 in goods-and-services payments AND more than 200 transactions. Personal payments between friends and family — splitting rent, gifts, reimbursements — are not taxable and should not trigger a 1099-K if tagged correctly. Some states still use lower thresholds, so you might get a state 1099-K even under the federal limit. Always verify current rules at IRS.gov.

What changed with the 1099-K rule — and why

A Form 1099-K is an information return that third-party payment platforms — apps like Cash App, Venmo and PayPal, as well as card processors and online marketplaces — file with the IRS and send to you. It reports the gross amount of payments you received for goods and services during the year. It is not a bill, and it does not by itself mean you owe tax.

Back in 2021, the American Rescue Plan Act lowered the reporting threshold dramatically — from the long-standing $20,000-and-200-transactions test down to just $600 with no transaction minimum. The idea was to capture more gig and side-hustle income. But the change caused years of confusion. The IRS repeatedly delayed full enforcement because so many ordinary users feared a flood of forms for casual, non-business activity.

That uncertainty ended in 2025. The “One Big Beautiful Bill Act,” signed July 4, 2025, repealed the American Rescue Plan’s $600 threshold and retroactively restored the original federal threshold. So the rule you may remember from years past is the rule again: a 1099-K is issued only when goods-and-services payments exceed $20,000 and there are more than 200 transactions in the year. Both conditions must be met at the federal level.

The practical takeaway: the vast majority of casual app users — people sending each other money for dinner, rent, or a birthday gift — are well below that bar and will not receive a federal 1099-K.

Who actually gets a 1099-K in 2026?

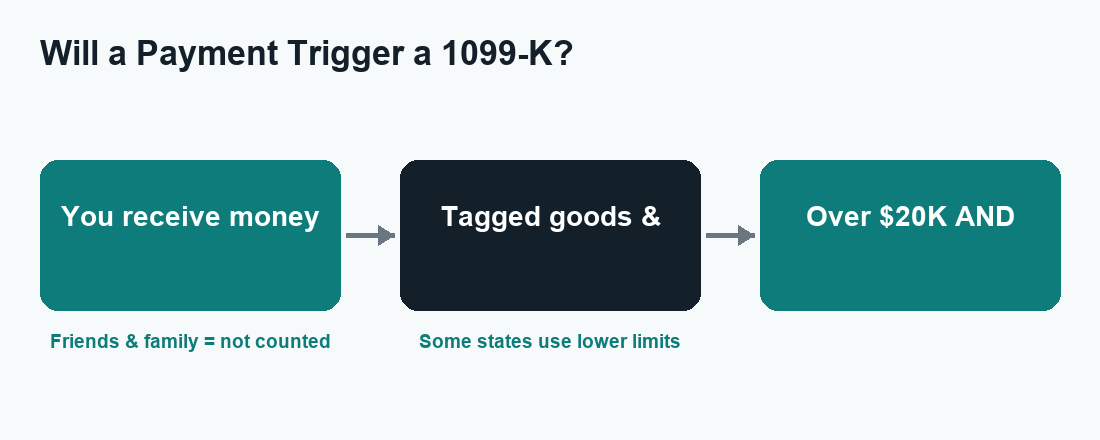

At the federal level, you should expect a 1099-K from a payment app only if both of these are true for the year:

- You received more than $20,000 in payments for goods and services, and

- Those payments came across more than 200 separate transactions.

This typically describes active sellers and businesses — think a busy online store, a reseller moving lots of inventory, or a freelancer collecting many client payments through a single app. If you sold a couple of used items or got reimbursed by friends a handful of times, you are not in this group.

One important nuance: the threshold is generally applied per platform. If you have meaningful business activity spread across several apps, each one tracks its own totals against the $20,000-and-200 test. Reaching the limit on one app does not automatically pull in the others.

Remember: Even if you fall below the threshold and receive no 1099-K, you are still legally required to report taxable income you earned. The form is a reporting tool — not the definition of what counts as income.

Federal vs. state thresholds: why you might still get a form

Here is the part that trips people up. The $20,000-and-200 figure is the federal threshold. Several states set their own, lower thresholds for 1099-K reporting, and payment apps must follow the rules of the state where you live.

That means you could stay under the federal limit and still receive a state 1099-K. Some states have used thresholds as low as $600, while others have landed around $2,500 or used other figures. These rules change, and not every state mirrors the federal number.

| Level | Dollar threshold | Transaction count | Both required? |

|---|---|---|---|

| Federal (2026) | More than $20,000 | More than 200 | Yes |

| Lower-threshold states (examples) | Often $600 or ~$2,500 | Usually none | No (dollar amount alone can trigger) |

Because state rules vary and get updated, do not assume your state matches the federal number. The amounts above are illustrative examples, not a complete or current list. Check your state’s department of revenue (or taxation) website for the threshold that applies to you, and verify the federal rule at IRS.gov.

Goods & services vs. friends & family: the line that matters most

This is the single most important distinction for everyday app users. Payment apps separate two very different kinds of transfers:

- Personal payments (friends & family): Splitting a dinner bill, chipping in for rent, sending a gift, repaying a loan, or reimbursing someone. These are not taxable income and should not count toward a 1099-K when they are tagged correctly.

- Goods & services payments: Money you receive in exchange for selling something or providing a service — these are business-type payments and do count toward the 1099-K thresholds.

The apps decide which bucket a payment falls into based on how it is sent and tagged. On Venmo and PayPal, the sender can choose a “goods and services” option (often tied to purchase protection); otherwise it is treated as a personal transfer. Cash App generally treats activity tied to a business account as goods and services.

Because of this, how a payment is labeled directly affects whether it shows up on a tax form. A reimbursement from a roommate that gets mistakenly flagged as “goods and services” could end up on a 1099-K even though it is not income — which is exactly the kind of error worth catching early.

Simple habits to keep personal and business separate

- Use the right tag. When friends send you personal money, make sure it is sent as a personal/friends-and-family transfer, not “goods and services.”

- Use a business account or profile for selling. If you run a side hustle, keep it on a dedicated business account so personal cash isn’t mixed in.

- Add clear notes. “Rent — June” or “Concert tickets payback” creates a paper trail showing the payment was personal.

- Don’t route business income through a personal handle. Mixing the two is the fastest way to get a confusing form.

What to do if you receive a 1099-K

Getting a 1099-K is not a reason to panic. It is a reminder to report income accurately. Here is a calm, step-by-step approach:

- Check the details. Confirm the name, taxpayer ID, the gross amount and the year are correct.

- Compare it to your own records. The form shows gross payments — before fees, refunds, or the cost of items you sold. Your taxable income is your actual profit, not the gross number.

- Separate personal from business. If personal reimbursements got swept in by mistake, note which amounts are not income.

- Report your real income. You owe tax on your actual profit or earnings, which is often less than the 1099-K total once costs and personal items are removed.

- Keep the form with your tax documents. The IRS already has a copy, so your return should account for it.

If you are unsure how a 1099-K affects your return, a tax professional can help — especially if you sell items, freelance, or run a small business.

If you get a 1099-K in error

Sometimes personal payments get miscategorized, or you receive a form for transactions that weren’t income (for example, selling personal items at a loss). If that happens:

- Contact the payment app first. Ask the platform that issued the form to correct it. The fix usually starts at the source.

- Request a corrected 1099-K if the original is wrong.

- Keep documentation showing the payments were personal or were sales of personal property at a loss.

- Follow IRS guidance for reporting and then backing out amounts that aren’t taxable, so the IRS can match the form to your return. Current instructions are at IRS.gov.

Watch out for 1099-K and “IRS” scams

Tax-season confusion is a magnet for scammers, and the 1099-K changes give them a fresh angle. Keep these rules in mind:

- The IRS does not text, email, or DM you demanding immediate payment or threatening arrest over a 1099-K. Real IRS contact generally starts with a letter by mail.

- No legitimate agency asks you to pay with gift cards, crypto, or a payment app. That request is always a scam.

- Don’t click links in unexpected “1099-K” or “tax due” messages. Go directly to IRS.gov or the app’s official help center instead.

- Your payment app won’t ask for your full Social Security number or password by message. When in doubt, log in through the official app, not a link.

Recordkeeping: your best protection

Whether or not you ever get a 1099-K, good records make tax time painless and protect you if a form shows up unexpectedly. A few minutes of organizing now saves hours later.

| What to keep | Why it matters |

|---|---|

| Transaction history (exported from each app) | Shows totals and lets you separate personal vs. business |

| Notes/memos on payments | Proves a transfer was a gift, reimbursement, or repayment |

| Receipts for items you sold | Establishes your cost so you only pay tax on real profit |

| Records of fees and refunds | Reduces gross 1099-K amounts down to actual income |

| Any 1099-K forms received | Lets you reconcile the form against your return |

Most apps let you download a yearly transaction report. Saving that file each January is one of the easiest financial habits you can build.

Frequently asked questions

Did the $600 1099-K threshold really go away?

Yes. The One Big Beautiful Bill Act, signed July 4, 2025, repealed the American Rescue Plan’s $600 threshold and retroactively restored the original federal rule: a 1099-K is issued only when goods-and-services payments exceed $20,000 and there are more than 200 transactions in a year. Confirm the current rule at IRS.gov before filing.

Will Venmo or Cash App report my payments to friends and family?

Personal payments between friends and family — splitting bills, gifts, reimbursements — are not taxable and should not trigger a 1099-K when tagged correctly. Only payments for goods and services count toward the thresholds. Just make sure personal transfers aren’t mislabeled as “goods and services.”

I’m below the federal threshold — could I still get a 1099-K?

Possibly. Some states set lower thresholds (for example, around $600 or $2,500) than the federal $20,000-and-200 limit, and apps follow the rules of your state. So you could receive a state 1099-K even under the federal limit. Check your state’s tax agency website for details.

Does getting a 1099-K mean I owe taxes?

No. A 1099-K just reports the gross amount you received for goods and services. You owe tax only on your actual profit or income — after subtracting fees, refunds, the cost of items sold, and any personal payments that were swept in by mistake.

What should I do if my 1099-K is wrong?

Contact the payment app that issued it and request a corrected form. Keep records showing which amounts were personal or were sales of personal items at a loss, and follow IRS guidance for reporting and backing out non-taxable amounts. Current instructions are at IRS.gov.

The bottom line

For 2026, the 1099-K picture is far simpler than the $600-threshold years suggested. The original federal limit is back — more than $20,000 and more than 200 transactions — so most casual Cash App, Venmo and PayPal users won’t get a federal form at all. The keys are to keep personal payments tagged correctly, watch for lower state thresholds, remember that a 1099-K isn’t a tax bill, and verify time-sensitive details with the official source at IRS.gov.

For more plain-English money guidance, explore our related WalletWisp guides on PayPal friends-and-family vs. goods-and-services, Venmo and Cash App fees, and how to keep your side-hustle finances organized.

{kind=link}