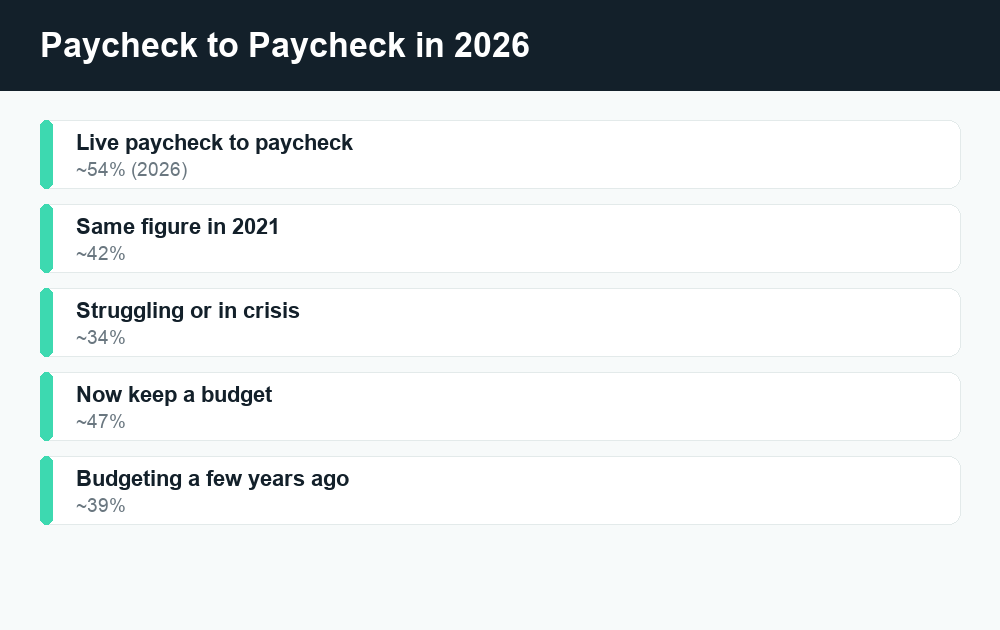

If you finish most months with little or nothing left over, you are far from alone: roughly 54% of Americans report living paycheck to paycheck in 2026, and the way out is not one big win but a handful of small, repeatable habits — track every dollar, build a starter emergency fund, cut your biggest bills, and automate the rest.

Quick answer: Living paycheck to paycheck means your income is fully spent before the next payday, leaving no buffer for surprises. In 2026 about 54% of Americans say they live this way — up from roughly 42% in 2021 — and about 34% describe their finances as struggling or in crisis. The fix is a sequence: see your spending clearly, build a small cash cushion, shrink fixed costs, automate savings, raise income, and knock out high-interest debt. None of these steps require a windfall, and the encouraging news is that more people are budgeting than ever (about 47% in 2026, up from 39%).

What “paycheck to paycheck” actually means

Living paycheck to paycheck simply means that by the time your next paycheck lands, the previous one is gone. It does not necessarily mean you are broke or irresponsible — plenty of higher earners live this way too, because spending tends to rise to match income. What it does mean is that you have little or no buffer between you and an unexpected expense. A car repair, a medical bill, or a single missed shift can turn a normal month into a crisis, often forcing people onto credit cards or short-term loans that make the next month even tighter.

The trend is heading the wrong direction. In 2026 about 54% of Americans report living paycheck to paycheck, up from roughly 42% in 2021. Around 34% go further and describe their finances as struggling or in crisis. Higher prices for essentials — housing, groceries, insurance, and transportation — have squeezed budgets faster than many paychecks have grown, so even people who feel they are “doing everything right” can find themselves with no margin.

There is a genuinely hopeful counter-trend, though: budgeting is on the rise. About 47% of Americans now keep a budget, up from 39% a few years ago. More people are paying attention, and paying attention is the first thing that actually moves the needle. The seven steps below build on each other in roughly the order most experts recommend. You do not have to do all of them at once. Start with step one this week.

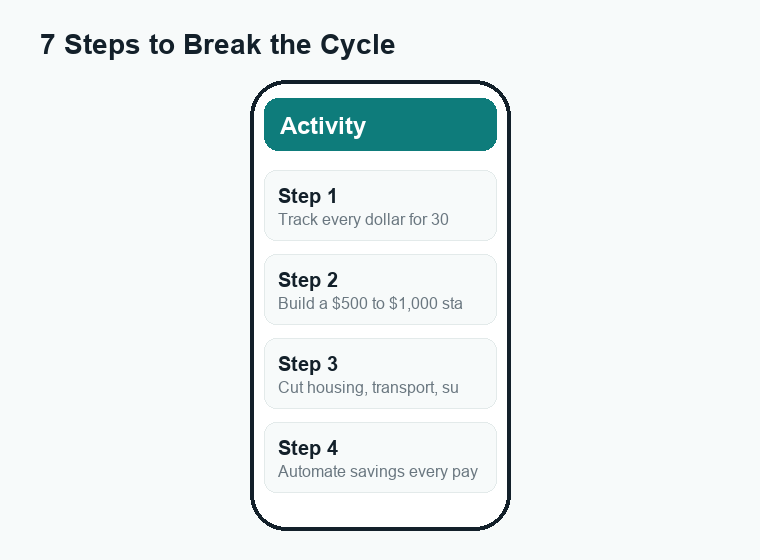

1. Track every dollar for 30 days

You cannot fix a leak you cannot see. Before you cut anything, spend 30 days simply recording where your money goes — every coffee, every subscription, every tank of gas. The point is not to judge yourself; it is to replace your guess about your spending with the truth, which is almost always different.

You have three easy options. First, a free budgeting app that connects to your bank and auto-categorizes transactions. Second, your bank or card app’s built-in spending tracker, which most major banks now offer at no cost. Third, a plain notebook or a simple spreadsheet if you prefer to log purchases by hand — manual tracking is slower but tends to make you more aware in the moment.

After 30 days, group your spending into needs (rent, utilities, groceries, minimum debt payments), wants (dining out, streaming, shopping), and savings. Most people discover at least one or two surprises — a forgotten subscription, or how much “small” purchases add up. That awareness alone often frees up money without any painful sacrifice.

2. Build a starter emergency fund

The single thing that breaks the paycheck-to-paycheck cycle fastest is a small cash cushion. Big goals like “three to six months of expenses” are correct in the long run, but they can feel so far away that people give up. So start smaller: aim for a starter emergency fund of around $500 to $1,000, kept somewhere separate from your checking account so it is not easy to spend by accident.

Why this matters so much: most financial emergencies are not enormous. A flat tire, a co-pay, or a utility deposit often falls in the few-hundred-dollar range. If you can cover those from savings instead of a credit card, you stop the cycle where one bad week snowballs into months of catch-up. Even $20 or $25 per paycheck adds up faster than you would expect, and the psychological relief of having any buffer is real.

Once your starter fund is in place and any high-interest debt is under control, you can gradually build toward the larger three-to-six-month goal. But get the first $500 to $1,000 in place before almost anything else.

3. Attack your three biggest bills

Small cuts help, but the fastest savings usually come from your largest fixed costs. For most U.S. households that means three things: housing, transportation, and recurring subscriptions. A single change to a big bill can free up more cash than weeks of skipping lattes.

Housing. It is your biggest line item for most people. If you rent, it is worth politely asking about renewal terms or comparing nearby options before you re-sign. A roommate, a smaller place, or renegotiating can meaningfully lower the number that dominates your budget.

Transportation. Car payments, insurance, gas, and repairs add up fast. Shopping your auto insurance once a year, combining errands, or — for some households — going from two cars to one can save real money. Even calling your current insurer to ask about discounts can help.

Subscriptions. Streaming, apps, memberships, and “free trials” you forgot to cancel quietly drain accounts. Review your last two or three statements line by line and cancel anything you have not used in the past month. A quick scam-awareness note: cancel subscriptions only through the official app or website, never through a link in a text or email claiming you owe money — those are common phishing attempts.

| Move | Where the savings come from | Effort |

|---|---|---|

| Cancel unused subscriptions | Recurring monthly charges | Low |

| Shop auto insurance yearly | Lower premium for same coverage | Low |

| Negotiate or compare rent | Largest fixed cost | Medium |

| Reduce to one vehicle | Payment, insurance, gas, repairs | High |

| Refinance high-interest debt | Less paid in interest | Medium |

4. Automate your savings

Willpower is unreliable; automation is not. The most effective savers do not decide each month whether to save — they set it up once and let it run. Schedule an automatic transfer from checking to savings for the day after each payday, even if it is a small amount. Because the money moves before you have a chance to spend it, you adjust your habits around what is left.

This is sometimes called “paying yourself first,” and it works precisely because it removes the monthly decision. If your employer offers direct deposit, you can often split it so a set amount goes straight to savings. Start with whatever is comfortable — even $25 a paycheck — and nudge it up by a few dollars whenever you get a raise or pay off a bill. You will barely notice the increases, but your balance will.

5. Increase your income

Cutting costs has a floor — you can only trim so much. Income, in theory, has no ceiling, so raising it is often the most powerful lever, especially if your budget is already tight. There are three realistic paths.

Earn more at your current job. A raise or a shift to a higher-paying role at the same employer is the highest-value move because it compounds over time. If you have not asked for a raise recently and you have a record of solid work, it is worth a respectful conversation.

Pick up a side gig. Rideshare, food delivery, freelancing, tutoring, reselling, or weekend work can add a few hundred dollars a month. Treat that extra money as targeted: send it straight to your emergency fund or your highest-interest debt rather than letting it disappear into everyday spending.

Sell what you no longer use. A one-time declutter-and-sell can fund a starter emergency fund quickly. A scam-awareness reminder for gig and side-income offers: a legitimate job never asks you to pay upfront fees, buy gift cards, or deposit a check and “send part of it back.” If an opportunity promises big money for almost no work, treat it as a red flag.

6. Tackle high-interest debt

High-interest debt — credit cards in particular — is the engine that keeps many people stuck. When a large share of each paycheck goes to interest, you are running just to stay in place. After your starter emergency fund is in place, make extra debt payments a priority, because the guaranteed “return” from eliminating, say, a 20%-plus interest rate is hard to beat anywhere else.

Two well-known payoff methods work; pick the one you will actually stick with:

- Avalanche: pay minimums on everything, then throw every extra dollar at the debt with the highest interest rate. This saves the most money mathematically.

- Snowball: pay minimums on everything, then attack the smallest balance first. You save a little less on interest, but the quick wins keep many people motivated.

If your credit is reasonable, a balance-transfer card or a lower-rate personal loan can sometimes cut your interest costs — just read the terms carefully and watch for transfer fees and the rate after any promotional period ends. And be cautious with “debt relief” companies that charge large upfront fees or promise to erase debt; if you want help, nonprofit credit counseling is a safer place to start. Verify any organization before sharing personal or financial details.

7. Use the right accounts (start with a HYSA)

Where you keep your money matters more than most people realize. A traditional checking or savings account at a big bank often pays almost nothing in interest. A high-yield savings account (HYSA) — typically offered by online banks — pays meaningfully more on the exact same dollars, with no extra effort on your part.

An HYSA is a natural home for your emergency fund: your money stays liquid (you can withdraw it when you need it), it is typically held at an FDIC-insured bank so your balance is protected up to legal limits, and it quietly earns interest while it sits. Keeping that cushion in a separate account also adds a small but useful speed bump between you and impulse spending.

Rates change often, so compare current offers and confirm a few basics before opening one: that the bank is FDIC-insured, that there are no monthly fees or surprise minimums, and that transfers to your checking account are free. Always open accounts directly through the bank’s official website or app — not through a link in an unsolicited message. For a deeper look, see WalletWisp’s guides on choosing a high-yield savings account.

Putting it together: a simple order of operations

If all seven steps feel like a lot, follow this sequence. Track your spending for one month so you know your numbers. Open a separate savings account (ideally an HYSA) and automate a small transfer each payday until you hit a $500–$1,000 starter fund. Trim your three biggest bills to free up cash. Then point that freed-up money at high-interest debt. Finally, work on raising your income and growing your emergency fund toward three to six months of expenses. Progress, not perfection, is the goal — and every step you complete makes the next one easier.

Frequently asked questions

How many Americans live paycheck to paycheck in 2026?

Roughly 54% of Americans report living paycheck to paycheck in 2026, up from about 42% in 2021. Around 34% describe their finances as struggling or in crisis. These figures come from survey data and can vary by source and definition, so treat them as a general picture of a worsening trend rather than an exact count.

What should I do first if I live paycheck to paycheck?

Start by tracking every dollar for 30 days so you can see exactly where your money goes. Once you know your numbers, open a separate savings account and automate even a small transfer each payday toward a $500–$1,000 starter emergency fund. That first cushion does the most to stop one bad week from snowballing.

How much should my starter emergency fund be?

A common starting target is $500 to $1,000, kept separate from your checking account. That range covers most everyday emergencies — a car repair or a medical co-pay — without forcing you onto a credit card. After that, work gradually toward the larger goal of three to six months of essential expenses.

Should I save or pay off debt first?

For most people the answer is “a little of both, in order.” Build the small starter emergency fund first so a surprise does not push you deeper into debt. Then prioritize extra payments on high-interest debt, since eliminating a 20%-plus interest rate is a guaranteed return that is hard to beat. After the high-interest debt is gone, return to growing your savings.

Is a high-yield savings account safe?

An HYSA held at an FDIC-insured bank is protected up to legal limits, and your money stays liquid so you can withdraw it when needed. The main things to check are that the bank is genuinely FDIC-insured, that there are no monthly fees, and that you open the account through the bank’s official website or app. Rates change frequently, so verify current terms before you sign up.

The bottom line

Living paycheck to paycheck is common in 2026 — more than half of Americans are in the same boat — but it is not a life sentence. The way out is a sequence of small, durable habits: see your spending clearly, build a starter cushion, shrink your biggest bills, automate savings, raise your income, and crush high-interest debt while keeping your cash in the right account. Pick one step and start this week; momentum builds faster than you think. For more, explore WalletWisp’s related guides on budgeting apps, high-yield savings accounts, and paying down credit card debt, and always verify time-sensitive details with official sources before you act.

")

{kind=link}