: Earn Up to $3,000")

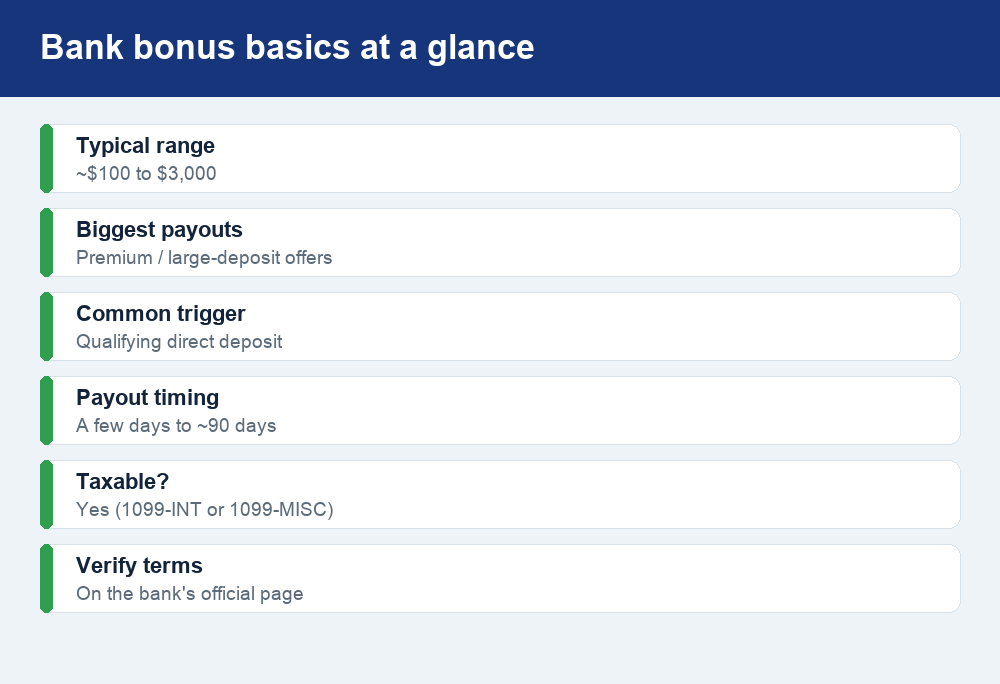

Bank account bonuses are cash rewards banks pay you for opening a new checking or savings account and meeting a few conditions, and in 2026 they commonly run from about $100 on the low end to as much as $3,000 for premium or large-deposit offers. To claim one, you typically open the account, set up a qualifying direct deposit, keep a minimum balance, and leave the account open for a set period.

Quick answer: Banks offer sign-up bonuses to win new customers. Checking bonuses in 2026 typically range from around $100 to $3,000, with the biggest payouts reserved for large deposits or premium accounts. You usually have to receive direct deposits totaling a set amount, hold a minimum balance, and keep the account open for several months. These bonuses are taxable income reported on a 1099-INT or 1099-MISC. Offers change constantly, so always confirm the live terms on the bank’s official page before you apply.

How bank account bonuses work

A bank account bonus is a marketing incentive. Customer acquisition is expensive, and a customer who moves their paycheck and everyday spending to a bank tends to stay for years. Paying you a few hundred dollars up front is often cheaper than advertising, so banks large and small run these promotions almost continuously.

The mechanics are straightforward. You open a specific account through a promotional link or with a promo code, complete the required actions inside a set window, and the bank deposits the bonus into your account. Payouts usually land anywhere from a few days to about 90 days after you finish the requirements, depending on the bank.

Bonuses come in a few flavors. Checking-account bonuses are the most common and generally pay the most, because a checking account is where your direct deposit and daily transactions live. Savings-account bonuses exist too, often tied to depositing and holding a large balance for a period of time. Some banks bundle both, offering a larger combined reward if you open a checking and a savings account together.

It is worth separating a one-time bonus from ongoing interest. A bonus is a fixed cash reward. Interest is what the account pays you month after month on your balance. A checking account with a great bonus may pay little or no interest afterward, which is why many people park their long-term cash in a separate account. If earning steady yield is your priority, compare the payout against the current best high-yield savings rates for July 2026 rather than chasing the headline bonus number alone.

Common requirements to earn a bonus

Almost every offer attaches conditions designed to make sure you actually use the account. Miss any one of them and the bank can legally withhold the bonus, so read the fine print before you commit. Here are the requirement types you will see most often.

| Requirement type | What it usually means | Why it matters |

|---|---|---|

| Qualifying direct deposit | Receive direct deposits totaling a set dollar amount within 60–90 days | The single most common trigger, and the one people most often fail |

| Minimum opening deposit | Fund the account with a required amount when you open it | Larger bonuses often demand larger deposits |

| Minimum balance | Keep your balance at or above a threshold for a stated period | Dropping below it can void the bonus or trigger fees |

| Account-open period | Keep the account open for a set number of months | Closing early may claw back the bonus or add a fee |

| Debit-card or transaction activity | Make a set number of purchases or payments | Some offers replace or add this to the direct-deposit rule |

| New-customer status | You have not held that account (or any account) with the bank recently | Prevents you from claiming the same bonus twice |

The direct-deposit requirement deserves special attention because it trips up the most people. Banks define a qualifying direct deposit narrowly. It usually means payroll or government benefits routed through the ACH network with a specific transaction code. A manual transfer you make from another bank, a mobile-check deposit, or a peer-to-peer payment from an app often does not count, even if the money clearly arrives on schedule. If your income does not come as a traditional paycheck, confirm exactly what the bank will accept before you rely on it.

Bank bonuses are taxable income

This surprises a lot of people: the cash you earn from a bank bonus is taxable. The IRS treats these rewards as interest or miscellaneous income, not as a tax-free gift. Your bank will typically report the amount on a 1099-INT (when it treats the bonus as interest) or a 1099-MISC (when it treats it as other income), and you are expected to report it on your federal return for the year you received it.

A couple of practical notes. First, you generally owe the tax whether or not you receive a form, so keep your own record of any bonus you earn. Second, the bonus is added to your other income and taxed at your ordinary rate, so the after-tax value of a $300 bonus is somewhat less than $300. That does not make bonuses a bad deal, but it is worth factoring in when you compare offers. If you are unsure how a bonus affects your specific situation, a tax professional can help.

How to earn a bonus safely, step by step

The good news is that a legitimate bank bonus from an established, FDIC-insured bank is not a scam or a gimmick. The risk is not that the bank fails to pay you; it is that you miss a requirement and forfeit the reward, or that you rack up fees that eat into it. A methodical approach removes most of that risk.

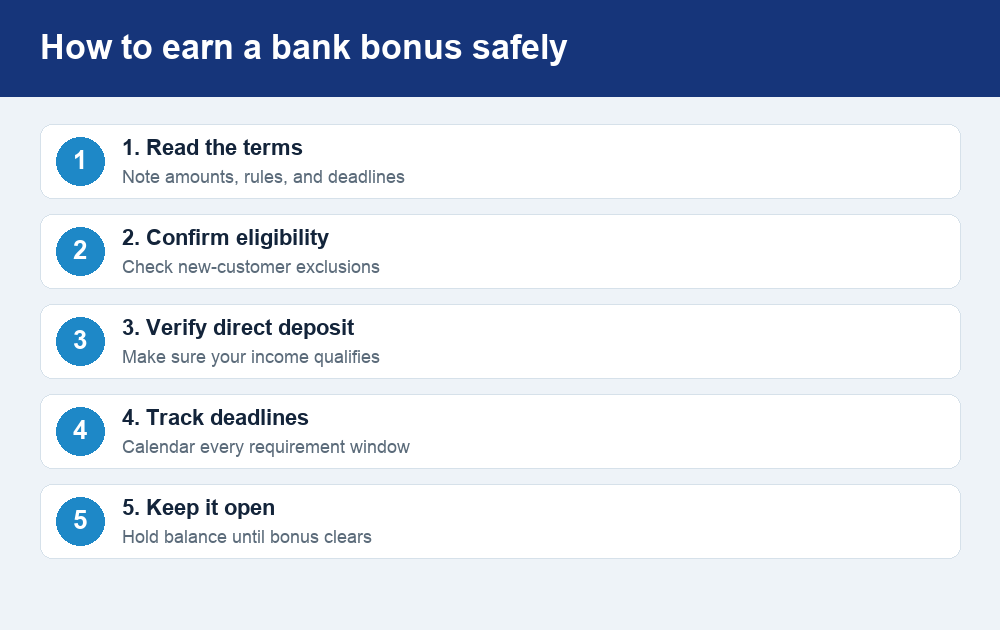

- Read the full offer terms first. Note the exact bonus amount, every requirement, the deadline for each, and the expected payout date. Screenshot or save the terms page.

- Confirm you qualify as a new customer. Many offers exclude people who have held that account recently. Check the exclusion window before applying.

- Verify your direct deposit will count. Ask your employer or the bank whether your specific income type meets the definition. This is the make-or-break step.

- Track the deadlines. Put the direct-deposit deadline, the minimum-balance window, and the account-open date on your calendar so nothing slips.

- Keep the account funded and open. Do not close it or drain it below the minimum until the required period ends and the bonus has posted and cleared.

- Confirm the bonus arrived. If it does not post within the promised window, contact the bank with your saved terms and dates.

Building the habit of tracking deadlines and balances is easier if you already watch your accounts closely. If you do not, a simple system helps; some of the best free budgeting apps for 2026 can send balance alerts and reminders that keep you from accidentally tripping a minimum-balance rule.

Pitfalls and red flags to avoid

Most problems with bank bonuses are self-inflicted and preventable. Watch for these in particular.

- Early-closure fees. Some banks charge a fee (or reverse the bonus) if you close the account within a set window, often 90 to 180 days. Read the account agreement, not just the bonus terms.

- Monthly maintenance fees. An account with a $12 monthly fee quietly erodes your bonus. Check whether the fee is waived by direct deposit or a minimum balance, and make sure you meet the waiver rules.

- Missing the direct-deposit rule. As covered above, this is the top reason people fail to get paid. Do not assume a transfer counts.

- ChexSystems denials. Banks screen applicants through ChexSystems, a reporting agency that tracks past account mishandling such as unpaid overdrafts or accounts closed for cause. A negative record can get your application denied, so opening many accounts carelessly can hurt you.

- Chasing a bonus you cannot afford to fund. A $2,000 bonus that requires a $50,000 deposit held for months only makes sense if that cash would otherwise sit idle. Do not lock up money you need.

- Phishing and fake offers. Only apply through the bank’s official website or app. Scammers mimic bonus promotions to harvest your Social Security number and login. A real bank never asks you to pay a fee to receive a bonus.

A note on bonus churning

Some people systematically open new accounts to collect bonuses, then move on, a practice known as bonus churning. Done carefully it can be lucrative, but it carries real trade-offs. Opening and closing many accounts can generate ChexSystems marks, trigger early-closure fees, and complicate your taxes with multiple 1099 forms. Banks also increasingly track and exclude repeat bonus-seekers. If you go this route, keep meticulous records, respect each bank’s eligibility windows, and never let the pursuit of a bonus push you into fees or a damaged banking record. For most people, claiming one or two well-chosen bonuses a year is the sweet spot.

Is a bonus worth it versus a higher rate?

Whether a bonus beats simply earning a strong ongoing rate depends on how long you plan to keep the money in the account. A one-time bonus is a big return on a short commitment, but it does nothing for you after it posts. A high-yield account earns you money every month you keep a balance there. For cash you will hold long term, comparing account structures matters more than any headline bonus; our breakdown of HYSA vs. CD vs. money market for 2026 walks through which vehicle fits which goal. The strongest play for many savers is to grab a checking bonus for the account they will use daily, then keep their savings in a separate high-yield account.

Frequently asked questions

How long does it take to get a bank bonus?

It varies by bank. Once you complete every requirement, most bonuses post within a few days to about 90 days. The offer terms should state the expected timing. If it does not arrive by the promised date, contact the bank with your saved terms and transaction records.

Do I have to pay taxes on a bank account bonus?

Yes. Bank bonuses are taxable income, usually reported to you and the IRS on a 1099-INT or 1099-MISC, and taxed at your ordinary income rate. You generally owe the tax even if you do not receive a form, so keep your own records.

Will opening accounts for bonuses hurt my credit score?

Opening a bank account usually does not affect your credit score the way a loan or credit card does, because most banks use a ChexSystems check rather than a hard credit pull. However, a poor ChexSystems record from past account problems can get future applications denied, so open accounts responsibly.

Can I earn the same bank bonus more than once?

Generally no. Most offers are limited to new customers and exclude anyone who has held that account within a recent window, often 12 to 24 months. Always read the eligibility rules before applying, since claiming a bonus you do not qualify for can get it clawed back.

Are bank bonus offers safe?

Bonuses from established, FDIC-insured banks are legitimate. The real risk is missing a requirement or paying fees that erase the reward, not the bank refusing to pay. Beware of copycat scams: apply only through the official site or app, and never pay a fee to receive a bonus.

The bottom line

Bank account bonuses are one of the simplest ways to earn a few hundred, or occasionally a few thousand, dollars for work you would arguably do anyway: moving your banking to a new institution. The path to actually getting paid is unglamorous but reliable. Read the terms, confirm your direct deposit qualifies, hit every deadline, keep the account open and funded, and remember the bonus is taxable. Because offers change constantly, treat any dollar figure you see, including the $3,000 headline, as a ceiling that only a few premium offers reach. Before you apply, always verify the live bonus amount and full terms on the bank’s official page.

")

{kind=link}