Most current forecasts point to mortgage rates drifting gradually lower through 2026, with some projections putting the average 30-year fixed rate near 5.9% by year-end — down from the roughly 6%–7% range seen recently. But that number is a forecast, not a promise: the Federal Reserve held rates steady in 2026, a few officials have floated possible hikes, and any single inflation report can push the outlook in either direction.

Quick answer: Several forecasters expect 30-year mortgage rates to end 2026 around 5.9%, continuing a slow decline that followed the Fed’s 2025 rate cuts. However, the Fed paused in 2026 and some policymakers see possible hikes, so the path is uncertain and could change with new inflation data. Don’t time your home purchase around a specific rate prediction — focus on what you can control, like your credit score, down payment, and shopping multiple lenders.

What actually drives mortgage rates

It’s a common myth that the Federal Reserve “sets” mortgage rates. It doesn’t — not directly. The Fed sets the federal funds rate, which is an overnight rate banks charge each other. That influences short-term borrowing costs like credit cards and home equity lines, but 30-year mortgages march to a different beat.

The single biggest driver of fixed mortgage rates is the bond market — specifically the yield on the 10-year U.S. Treasury note. Mortgage rates tend to move in step with the 10-year Treasury, usually sitting a percentage point or two above it. When investors buy more Treasury bonds, yields fall and mortgage rates tend to follow. When they sell, yields rise.

So what moves Treasury yields and, by extension, your mortgage rate? A few big forces:

- Inflation. This is the headline driver. When inflation runs hot, lenders demand higher rates to protect the future value of the money they’re lending. Cooling inflation generally clears the path for lower rates.

- The Federal Reserve’s stance. The Fed doesn’t set mortgage rates, but its signals about future policy heavily shape investor expectations. A Fed that’s cutting (or expected to cut) tends to pull rates down; a Fed on hold or hinting at hikes keeps them sticky.

- The broader economy. Strong job growth and robust spending can push rates up; signs of slowdown often push them down as investors seek the safety of bonds.

- Global events and demand for bonds. Geopolitical shocks, government debt levels, and overseas demand for U.S. Treasurys all nudge yields around.

The takeaway: mortgage rates are the product of many moving parts, which is exactly why even careful forecasts come with wide error bars.

The 5.9% forecast — and its big caveats

Here’s the setup heading into mid-2026. The Fed delivered a series of rate cuts in 2025, which helped ease borrowing costs across the economy. Coming out of that, a number of housing and economic forecasters projected that 30-year mortgage rates would continue a slow grind downward through 2026, with some landing near 5.9% by the end of the year — a meaningful step down from the highs in the 6%–7% range.

That sounds encouraging if you’re a buyer or hoping to refinance. But the caveats matter just as much as the number:

- The Fed held rates in 2026. After cutting in 2025, the Fed paused. A pause means rates aren’t getting an automatic push lower from policy — the decline has to come from cooling inflation and bond-market dynamics instead.

- Some officials see possible hikes. Not every policymaker agrees on the direction. If inflation reaccelerates, the conversation can shift from “when do we cut?” to “do we need to hike?” That alone can stall or reverse a forecasted decline.

- Forecasts are snapshots, not guarantees. A single surprising jobs report or inflation reading can move the 10-year Treasury within hours, and mortgage rates with it. The 5.9% figure is a reasonable central estimate, not a finish line that’s locked in.

| Scenario | What it would take | Likely direction for rates |

|---|---|---|

| Rates ease toward ~5.9% | Inflation keeps cooling; economy softens modestly | Gradually lower |

| Rates stay in the 6% range | Inflation sticky; Fed stays on hold | Roughly flat |

| Rates tick back up | Inflation reaccelerates; hike talk grows | Higher |

The honest bottom line: a move toward the high-5% range by the end of 2026 is plausible, but it’s far from certain. Always check the latest figures with a current source — rate trackers update daily, and the picture can shift quickly.

Buy now or wait? How to think about it

The “should I wait for lower rates?” question is one of the most common in personal finance — and one of the trickiest, because nobody can reliably time the market. Here’s a framework that beats guessing.

The case for buying now

- You’re financially ready. Stable income, an emergency fund intact after the down payment and closing costs, and a comfortable monthly payment matter more than the headline rate.

- You can refinance later. If rates do fall, refinancing is an option (more on the math below). The old saying — “marry the house, date the rate” — captures the idea that you can change your rate later but you lock in the home now.

- Waiting has costs too. Rent paid while waiting is money you don’t get back, and home prices can rise even when rates don’t fall. A lower rate on a more expensive house isn’t always a win.

The case for waiting

- Your finances aren’t ready yet. If waiting lets you boost your credit score, save a larger down payment, or pay down debt, that can improve your rate and terms more reliably than betting on the market.

- Your situation may change. A possible move, job change, or major life event in the near term can make renting the smarter call for now.

The key insight: trying to perfectly time the bottom of the rate cycle is a losing game even for professionals. Base the decision on your own readiness and budget, not on a forecast. If the numbers work today at today’s rate, a future rate drop is a bonus you can capture through refinancing — not a reason to sit on the sidelines.

Refinancing math: the rough rule of thumb

If you buy now and rates fall later, refinancing lets you swap your existing loan for a new one at a lower rate. But refinancing isn’t free — you typically pay closing costs again, often a few thousand dollars. So the question is whether the monthly savings are worth that upfront cost.

A common, simple rule of thumb: refinancing often makes sense if you can lower your rate by at least about 0.5 to 1 percentage point and you plan to stay in the home long enough to recoup the closing costs. That’s a guideline, not a law — the right threshold depends on your loan size and how long you’ll keep the loan.

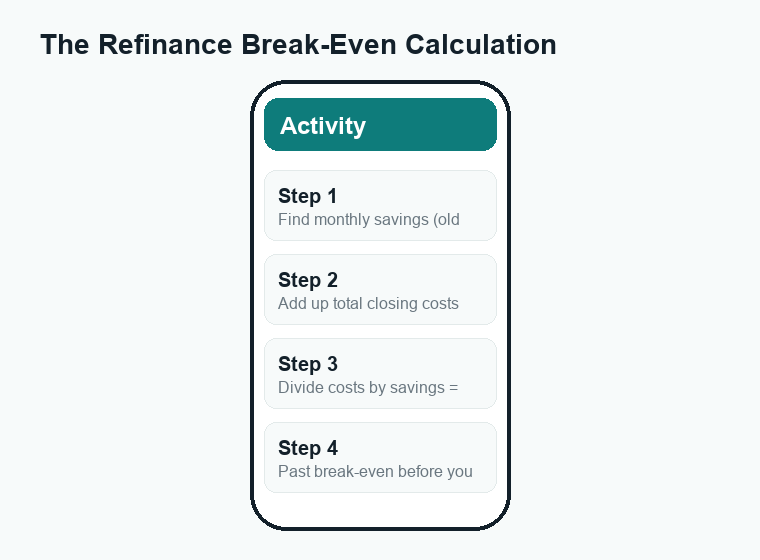

The cleaner way to decide is the break-even calculation:

| Step | What to do | Example |

|---|---|---|

| 1. Find your monthly savings | Old payment minus new payment | $150/month |

| 2. Add up the closing costs | Lender fees, appraisal, title, etc. | $4,500 |

| 3. Divide costs by savings | Closing costs ÷ monthly savings | $4,500 ÷ $150 = 30 months |

| 4. Compare to how long you’ll stay | Past break-even = likely worth it | Staying 5+ years → yes |

In that example, you’d break even in about 30 months (2.5 years). If you expect to stay in the home longer than that, refinancing likely pays off. If you might move sooner, the closing costs could outweigh the savings. The numbers above are illustrative — run your own with a refinance calculator and a real quote.

One more note: if rates drift toward the high-5% range as some forecasts suggest, plenty of recent buyers who locked in 6%–7% loans could find refinancing worthwhile. It’s worth keeping an eye on rates and being ready to act when the math works for you.

How to get the best mortgage rate

You can’t control the Fed or the bond market, but you have real influence over the rate you personally get offered. Lenders price loans based on risk, so anything that makes you look like a safer borrower can lower your rate. Focus here:

1. Strengthen your credit score

Your credit score is one of the biggest levers. Borrowers with higher scores typically qualify for noticeably lower rates than those with lower scores. Before applying, pay every bill on time, keep credit card balances low relative to your limits, and avoid opening new credit accounts. Check your credit reports for errors and dispute any you find — you can get free reports at AnnualCreditReport.com.

2. Save a bigger down payment

A larger down payment reduces the lender’s risk and can earn you a better rate. Putting down at least 20% also lets you avoid private mortgage insurance (PMI) on conventional loans, which lowers your monthly payment further. Even if 20% isn’t realistic, a bigger down payment generally helps your terms.

3. Shop multiple lenders — this is the big one

This is the most underused money-saving move in the whole process. Rates and fees vary meaningfully from lender to lender, and getting quotes from several — banks, credit unions, and online lenders — can save you real money over the life of the loan. Compare the Annual Percentage Rate (APR), not just the interest rate, because APR folds in fees for a more apples-to-apples comparison.

Worried about your credit score taking a hit from multiple inquiries? Don’t be. Credit-scoring models generally treat all mortgage rate shopping done within a short window (often a few weeks) as a single inquiry, so it’s safe to gather several quotes close together.

4. Consider the loan structure

- Loan term. A 15-year mortgage usually carries a lower rate than a 30-year, though the monthly payment is higher.

- Discount points. You can sometimes pay an upfront fee (“points”) to buy down your rate. Whether that’s worth it depends on how long you’ll keep the loan — similar break-even logic to refinancing applies.

- Loan type. Conventional, FHA, VA, and USDA loans have different rate and eligibility profiles. A VA or USDA loan, if you qualify, can be especially favorable.

Scam-aware tip: Be wary of anyone promising a guaranteed rate far below the market, pressuring you to “lock in now or lose it,” or asking you to wire fees to an unfamiliar account. Legitimate lenders give you a written Loan Estimate within three business days of your application — use it to compare offers, and verify any lender through official channels before sending money.

Frequently asked questions

Will mortgage rates definitely drop to 5.9% in 2026?

No — 5.9% is a forecast some analysts have offered, not a guarantee. It assumes inflation continues to cool and the economy behaves a certain way. The Fed held rates steady in 2026 and some officials have mentioned possible hikes, so rates could stay higher or even rise. Check a current rate tracker for the latest figures, since the outlook changes with new data.

Does the Federal Reserve set mortgage rates?

Not directly. The Fed sets the federal funds rate, a short-term rate for banks. Fixed mortgage rates track the bond market — especially the 10-year Treasury yield — which is driven heavily by inflation expectations and the economic outlook. The Fed’s signals influence those expectations, but your 30-year rate isn’t set by the Fed.

Should I wait to buy a home until rates fall?

Only if waiting genuinely improves your finances — for example, by letting you raise your credit score or save a larger down payment. Trying to time the exact bottom of the rate cycle is unreliable even for experts. If the monthly payment fits your budget at today’s rate and you’re financially ready, buying now and refinancing later if rates drop is often the more practical path.

When does refinancing make sense?

A common rule of thumb is to consider refinancing when you can lower your rate by roughly 0.5 to 1 percentage point and you’ll stay in the home long enough to recoup the closing costs. The most reliable approach is the break-even calculation: divide your total closing costs by your monthly savings to see how many months it takes to come out ahead, then compare that to how long you plan to keep the loan.

What’s the easiest way to lower the rate I’m offered?

Shop multiple lenders. Rates and fees vary from one lender to the next, and gathering quotes from several — banks, credit unions, and online lenders — within a short window counts as a single credit inquiry, so it won’t hurt your score. Compare the APR, not just the interest rate. Pair that with a strong credit score and a solid down payment for the best results.

Conclusion

A move toward 5.9% on the 30-year mortgage by the end of 2026 is a plausible scenario built on cooling inflation following the Fed’s 2025 cuts — but it’s a forecast, not a sure thing, and a 2026 Fed pause plus hike talk keeps the path uncertain. Rather than gambling on a prediction, anchor your decision on your own readiness, run the break-even math before you refinance, and squeeze the best rate you can by improving your credit, saving a larger down payment, and shopping several lenders. And always verify time-sensitive rate details with a current, trusted source before you act.

For more on making the most of your money, explore our related WalletWisp guides on building credit, comparing loan options, and budgeting for big purchases.

{kind=link}