: Earn 10x the National Average")

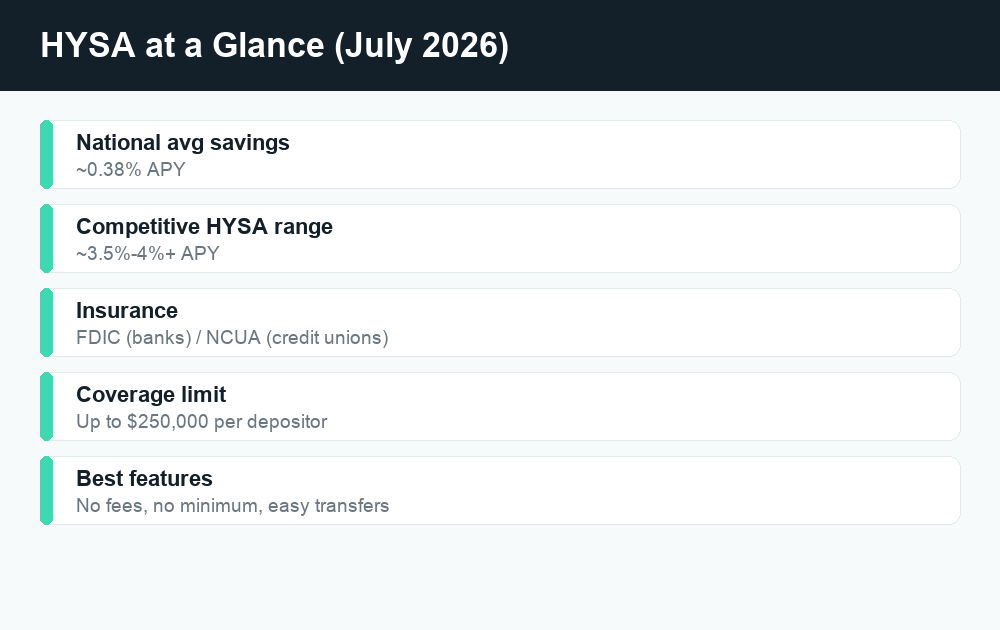

The best high-yield savings accounts in July 2026 are paying many times the national average savings rate of roughly 0.38%, with competitive online banks and credit unions commonly landing in the mid-3% to 4%-plus APY range. That gap means moving cash from a typical big-bank savings account into a high-yield savings account (HYSA) can earn you roughly 10 times more interest on the exact same balance, with the same federal deposit insurance protection.

Quick answer: A high-yield savings account pays a much higher annual percentage yield (APY) than a standard savings account, often many multiples of the ~0.38% national average. Top rates today tend to cluster in the mid-3% to 4%-plus range, but exact numbers move with the Federal Reserve, so no single rate stays “the best” for long. Look for accounts with no monthly fees, no minimum balance, FDIC or NCUA insurance, and easy transfers, then compare current rates on a reputable comparison site before you open one.

What is a high-yield savings account?

A high-yield savings account is a regular savings account that pays a notably higher interest rate than the savings account you’d get at a typical brick-and-mortar bank. Functionally it works the same way: you deposit money, it stays liquid and accessible, and the bank pays you interest for keeping it there. The difference is the yield. While many large national banks advertise rates near the national average of about 0.38%, online banks and credit unions frequently pay several times that.

HYSAs are designed for money you want to keep safe and reachable but still want to grow, like an emergency fund, a down payment you’re saving toward, or cash you’re parking between bigger financial moves. They are not investment accounts: your principal doesn’t go up and down with the stock market, and within federal insurance limits, your deposits are protected. The trade-off is that the rate can change at any time, since savings rates are variable rather than locked in.

How a HYSA differs from a checking account or CD

A checking account is built for everyday spending and bill paying, and it usually pays little or no interest. A certificate of deposit (CD) locks your money up for a set term in exchange for a fixed rate, so you generally can’t touch it without an early-withdrawal penalty. A high-yield savings account sits in between: it pays a strong variable rate while keeping your money accessible for transfers and withdrawals. For most people building an emergency cushion, that liquidity is exactly why a HYSA is a better fit than a CD.

How APY and compounding actually work

When you compare savings accounts, the number that matters most is the annual percentage yield (APY), not the plain interest rate. APY reflects how much you’ll actually earn in a year because it accounts for compounding, which is interest earning interest. Most HYSAs compound daily and pay out monthly, so the interest you earn each day starts earning its own interest going forward.

Because APY already bakes in compounding, it gives you an apples-to-apples way to compare two accounts. An account quoting a higher APY will earn you more over a year than one with a lower APY, assuming the same balance. Here’s a simplified illustration of how the same $10,000 grows over one year at different yields. These figures are rounded estimates for illustration only and assume the rate stays constant, which real-world variable rates won’t.

| APY | Type of account | Approx. interest on $10,000 (1 yr) |

|---|---|---|

| ~0.38% | National average savings | ~$38 |

| ~3.50% | Competitive HYSA (lower end) | ~$350 |

| ~4.00% | Competitive HYSA (higher end) | ~$400 |

The takeaway isn’t the precise dollar amount, which will vary as rates shift. It’s the scale of the difference: a competitive HYSA can multiply your interest several times over compared with leaving cash in a typical big-bank account, and you don’t have to take on any extra risk to capture it.

Your money is still insured

One of the most common worries about online banks is safety, and it’s worth addressing head-on. Reputable high-yield savings accounts carry the same federal deposit insurance as traditional banks. At banks, that’s the FDIC (Federal Deposit Insurance Corporation). At credit unions, it’s the NCUA (National Credit Union Administration). Standard coverage is generally up to $250,000 per depositor, per insured institution, per ownership category.

That insurance means if an insured bank or credit union were to fail, your covered deposits are protected up to the limit. Before opening any account, confirm the institution is FDIC- or NCUA-insured. Most legitimate banks display this clearly, and you can verify a bank on the FDIC’s official site (FDIC.gov) or a credit union on the NCUA’s site (NCUA.gov). If an account promising eye-popping rates can’t show federal insurance, treat that as a serious red flag.

What to look for in a high-yield savings account

The headline APY matters, but it isn’t the whole story. A slightly lower rate at a clean, no-strings account often beats a slightly higher rate buried under fees and restrictions. Here’s what to weigh:

- No monthly maintenance fees. Fees quietly eat into your interest. The best HYSAs charge nothing to keep the account open.

- No (or low) minimum balance. Look for accounts that don’t require a large balance to open or to earn the advertised rate. Some accounts pay the top APY only above a certain threshold, so read the fine print.

- Easy transfers. Since many HYSAs are online-only, you’ll move money between this account and your checking account by linking them. Check how long transfers take and whether there are limits.

- A genuinely competitive APY. Compare against current top rates rather than against your current bank. A rate that beats the national average by a hair isn’t really “high-yield.”

- Reasonable withdrawal access. Understand any monthly transaction limits and how you can get to your money in a pinch.

- Strong reputation and clear terms. Stick with established, federally insured institutions and read how and when the rate can change.

Also watch for introductory or promotional rates that drop after a few months, and for “tiered” rates where the advertised APY only applies to part of your balance. Neither is automatically bad, but you want to know the rules before you commit.

Online banks vs. brick-and-mortar banks

The reason online banks tend to offer the strongest savings rates comes down to overhead. Without thousands of physical branches to staff and maintain, online banks have lower costs, and they often pass some of those savings back to customers as higher APYs. Traditional brick-and-mortar banks, by contrast, frequently pay rates close to the national average even on their “savings” products.

That doesn’t make branch banks wrong for everyone. If you value walking into a branch, depositing cash regularly, or keeping all your accounts under one roof, a traditional bank has real conveniences. A popular middle path is to keep your everyday checking at a bank you like and open a separate high-yield savings account online purely to grow your savings. The two accounts link together, and you move money as needed.

| Feature | Online HYSA | Typical brick-and-mortar savings |

|---|---|---|

| Typical APY | Often several times the average | Often near ~0.38% average |

| Branches | Usually none | Yes |

| Monthly fees | Often none | Sometimes |

| Cash deposits | Harder (transfer-based) | Easy at a branch |

| Federal insurance | FDIC or NCUA | FDIC or NCUA |

How the Fed affects your savings rate

High-yield savings rates don’t move randomly. They tend to track the Federal Reserve’s benchmark interest rate. When the Fed raises rates, banks generally raise the APYs on savings accounts to attract deposits. When the Fed cuts rates, savings APYs tend to drift down. And when the Fed holds rates steady, savings yields tend to stay relatively stable, though individual banks still adjust their offers to stay competitive.

This is exactly why no article can promise you a single “best” rate that will hold. The competitive range today reflects the current rate environment, and it can shift in either direction. The practical implication: because HYSA rates are variable, it’s worth checking your APY periodically. If your bank quietly lets its rate slip well below the market, you’re free to move your money to a better one, and doing so is straightforward.

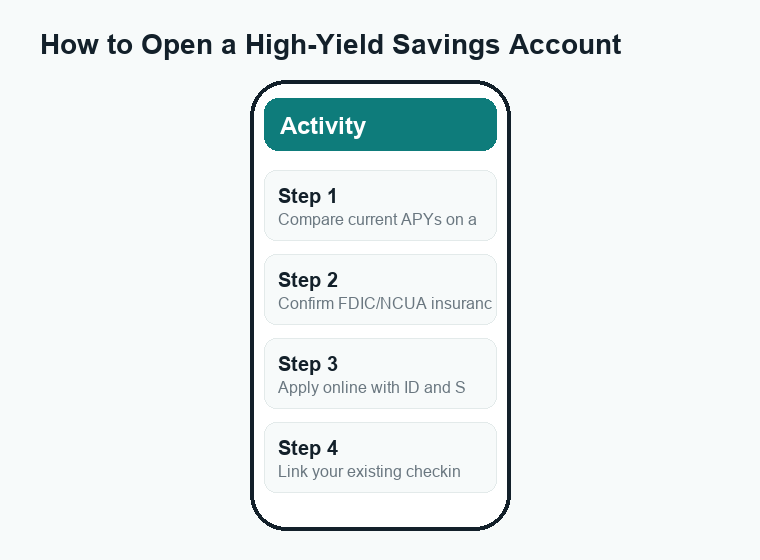

How to open a high-yield savings account

Opening a HYSA is usually a quick online process. The general steps look like this:

- Compare current rates. Use a reputable, up-to-date comparison site to see today’s top APYs side by side, since rates change frequently. Don’t rely on a number you saw months ago.

- Confirm it’s insured and fee-free. Verify the institution is FDIC- or NCUA-insured and check for monthly fees and minimum-balance requirements.

- Apply online. You’ll typically provide your name, address, Social Security number, and a government ID to verify your identity. This is standard and required by law.

- Link your existing bank account. Connect your current checking account so you can fund the HYSA and transfer money in and out later.

- Make your first deposit. Move over your starting balance. Many accounts have no minimum, so you can start small and add more over time.

From there, set up automatic transfers if you want to build savings consistently, and check your rate once in a while to make sure it’s still competitive.

Watch out for scams and look-alikes

High savings rates attract bad actors. Be cautious of unsolicited messages, ads, or “banks” you’ve never heard of promising rates dramatically above the competitive range. Legitimate institutions will clearly state their FDIC or NCUA insurance, and you can independently verify them on FDIC.gov or NCUA.gov. Never enter your Social Security number or banking login on a site you reached through an unexpected text or email link, and type the bank’s web address yourself rather than clicking through. If a rate or offer seems too good to be true, it usually is.

Frequently asked questions

How much can I really earn with a high-yield savings account?

It depends on your balance and the APY, both of which can change. As a rough illustration in today’s environment, $10,000 in a competitive HYSA could earn many times more interest over a year than the same amount at the ~0.38% national average. The exact dollar figure varies, so use the account’s stated APY and your real balance to estimate, and remember the rate can move.

Is my money safe in an online high-yield savings account?

Yes, as long as the institution is federally insured. Reputable online banks carry FDIC insurance and credit unions carry NCUA insurance, generally up to $250,000 per depositor, per institution, per ownership category. Always confirm insurance before opening an account, and verify the institution on FDIC.gov or NCUA.gov if you’re unsure.

Can the bank lower my rate after I open the account?

Yes. HYSA rates are variable, not fixed, and they tend to follow the Federal Reserve’s benchmark rate. Your APY can rise or fall over time. That’s normal, and it’s also why it pays to check your rate occasionally and move your money if your bank falls well behind the market.

What’s the difference between a HYSA and a CD?

A high-yield savings account keeps your money accessible and pays a variable rate, so you can withdraw or transfer when you need to. A certificate of deposit locks your money for a fixed term at a fixed rate, with a penalty for early withdrawal. For an emergency fund or savings you might need on short notice, a HYSA’s liquidity is usually the better choice.

Are there taxes on the interest I earn?

Generally, yes. Interest earned in a savings account is typically treated as taxable income, and your bank will usually send you a tax form if you earn above a certain amount in a year. Tax situations vary, so check current guidance at IRS.gov or consult a tax professional about your specific circumstances.

The bottom line

A high-yield savings account is one of the simplest ways to make your cash work harder without taking on risk. By moving savings out of a typical near-average account and into a competitive, federally insured HYSA, you can earn many times more interest on the same balance. Just remember that rates are variable, move with the Fed, and differ from bank to bank, so compare current APYs on a reputable site, confirm FDIC or NCUA insurance, and watch for fees before you open one. For more on growing and protecting your money, explore our related WalletWisp guides on building an emergency fund, comparing savings accounts and CDs, and choosing the right banking app.

")

{kind=link}