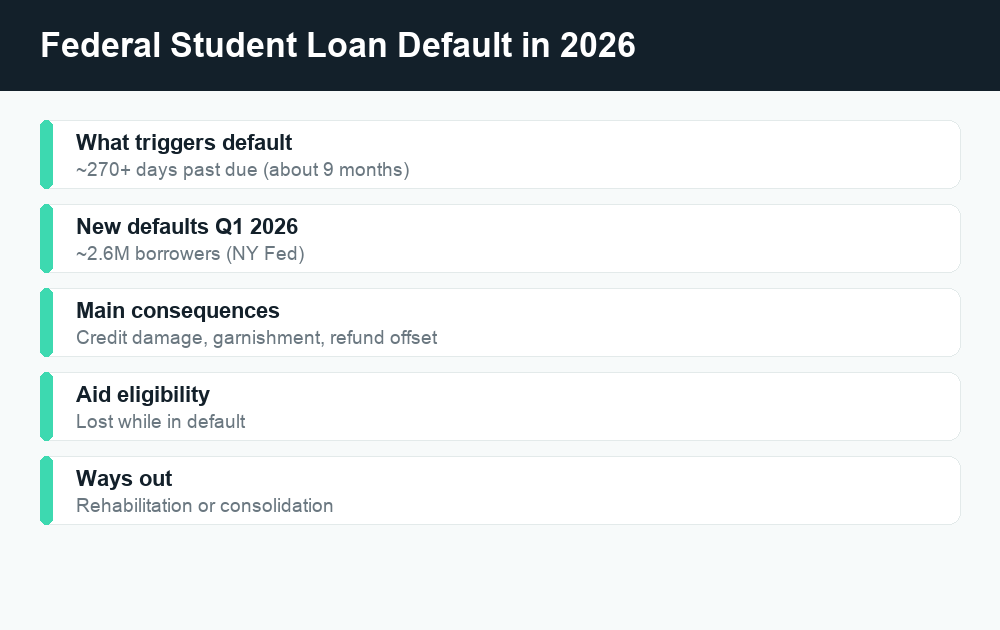

Federal student loan default is back in force in 2026, and the consequences are real: if you go roughly 270 or more days without paying, you can face wage garnishment, a damaged credit score, and the seizure of your tax refund. The good news is that default is fixable, and you have several clear paths out, including loan rehabilitation, consolidation, and switching to an affordable income-driven repayment plan.

Quick answer: Now that pandemic-era pauses have ended, defaults are climbing again. The New York Fed reported that roughly 2.6 million additional federal borrowers were moved to the Department of Education’s Default Resolution Group in the first quarter of 2026. If you are behind, contact your loan servicer and visit studentaid.gov immediately. You can usually get out of default through rehabilitation or consolidation, and you can avoid it altogether by enrolling in an income-driven repayment plan or requesting deferment or forbearance.

Why student loan defaults are surging again in 2026

For several years during the pandemic, federal student loan payments were paused and interest was set to zero. During that window, almost no one could fall into default, because there were no payments to miss. Those protections have now ended, payments have resumed, and the safety net that kept millions of borrowers technically current has been removed.

The result is showing up in the data. According to the Federal Reserve Bank of New York, roughly 2.6 million additional federal borrowers were moved to the Department of Education’s Default Resolution Group in the first quarter of 2026. That group handles loans that have reached serious delinquency or default, and a jump of that size signals that a large wave of borrowers has fallen far behind.

If you are one of them, the most important thing to know is this: you are not stuck. Federal student loans come with recovery options that most other debts do not offer. But these options work best when you act early, so it pays to understand exactly where you stand.

What “default” actually means for federal student loans

People often use “behind on payments” and “in default” interchangeably, but they are not the same thing. There are usually three stages, and knowing which one you are in tells you how urgent your situation is.

- Current: You are making your scheduled payments on time. No action needed beyond staying on track.

- Delinquent: You have missed at least one payment. Your account is past due, and after a certain point your servicer will report the late payment to the credit bureaus.

- Default: For most federal student loans, you typically enter default after roughly 270 or more days without a payment, which is about nine months past due. At that point the full balance can become due, and the loan moves into collections.

The exact timeline and rules can vary by loan type, so always confirm your specific status with your servicer or by logging in at studentaid.gov. The key takeaway is that default is the late stage, not the first warning. If you have only missed a payment or two, you still have time to act before the more serious consequences kick in.

| Stage | Roughly how long past due | What it means |

|---|---|---|

| Current | On time | No penalties |

| Delinquent | 1 to ~269 days | Reported to credit bureaus; late fees and credit damage begin |

| Default | ~270+ days | Full balance due, sent to collections, garnishment and offset possible |

The real consequences of default

Default is serious because it gives the government collection powers that private creditors do not have. You do not get to choose whether these tools are used. Here is what can happen once a federal loan is in default.

Credit damage

Default is reported to the credit bureaus and can stay on your credit report for years. A lower credit score can make it harder and more expensive to rent an apartment, finance a car, or qualify for a mortgage. The longer a default sits unresolved, the more it can drag on your financial life.

Wage garnishment

After default, the government can garnish your wages, meaning a portion of your paycheck is taken automatically to repay the debt. Unlike most creditors, the Department of Education generally does not need to sue you in court first to do this. There are limits on how much can be taken, but losing any slice of your paycheck unexpectedly can be painful.

Tax refund and benefit offset

Through a process called Treasury offset, the government can intercept your federal tax refund and apply it to your defaulted loan. In some cases, a portion of certain federal benefit payments can also be offset. For families counting on a refund each spring, this can come as a shock.

Loss of aid eligibility

While a loan is in default, you generally lose access to additional federal student aid. If you were hoping to go back to school, finish a degree, or pursue a certificate program, default can block the grants and loans you would need to do it.

Because rules and collection practices can change, verify exactly what applies to your loans at studentaid.gov rather than relying on a collector’s word alone.

How to get out of default

If your loan is already in default, you have real options to fix it. The two most common federal paths are loan rehabilitation and consolidation. Each one ends the default status, but they work differently.

Loan rehabilitation

Rehabilitation involves agreeing to a series of on-time monthly payments over a set period. The payment amount is meant to be reasonable and is generally based on your income, so it can be modest if you are earning little. Once you complete the agreed payments, the loan is removed from default. A major benefit of rehabilitation is that the record of the default can be removed from your credit report, though late payments reported before default may remain. Rehabilitation is typically a one-time option per loan, so it is worth using carefully.

Loan consolidation

Consolidation combines one or more federal loans into a new Direct Consolidation Loan, which is not in default. To use consolidation to get out of default, you usually either make a few on-time payments first or agree to repay the new loan under an income-driven plan. Consolidation can be faster than rehabilitation, but it does not erase the default notation from your credit history the way completed rehabilitation can. It is often a good fit if you need to resolve default quickly to regain aid eligibility.

The “Fresh Start” context

You may have heard about Fresh Start, a federal effort that gave many borrowers with defaulted loans a temporary path back to good standing with restored benefits and access to aid. Programs like this come and go and have deadlines and eligibility rules that change over time. Do not assume any particular relief program is still open or that you automatically qualify. Check the current status and your options directly at studentaid.gov, and ask your servicer what applies to your specific loans today.

| Path out of default | How it works | Credit impact |

|---|---|---|

| Rehabilitation | Series of agreed, income-based on-time payments | Default record can be removed once completed |

| Consolidation | Combine loans into a new non-default Direct Loan | Default notation generally remains on record |

How to avoid default in the first place

If you are behind but not yet in default, you are in a much stronger position. The goal now is simple: get into a plan you can actually afford, and keep your loans out of the danger zone. Here are the main tools.

Income-driven repayment (IDR)

Income-driven repayment plans set your monthly payment based on your income and family size rather than your balance. For many borrowers, this dramatically lowers the monthly bill, and in some cases payments can be very low if your income is modest. IDR is one of the most powerful ways to stay current, because a payment you can afford is a payment you are far more likely to make. The specific IDR plans available, and their terms, can change, so review the current menu of plans at studentaid.gov.

Deferment and forbearance

If you hit a temporary rough patch, deferment and forbearance let you pause or reduce payments for a defined period. Deferment may be available for situations like unemployment or returning to school, and on some loan types interest does not accrue during deferment. Forbearance is more broadly available but interest generally keeps accruing, which means your balance can grow. These tools are best used as short-term bridges, not long-term solutions, because pausing payments does not make the debt go away.

Stay reachable and stay informed

One of the simplest ways borrowers slide into default is by losing touch with their servicer. Servicers can change, mail can get missed, and emails can land in spam. Make sure your contact information is current with both your servicer and studentaid.gov, open the messages you receive, and never ignore a notice just because the situation feels overwhelming.

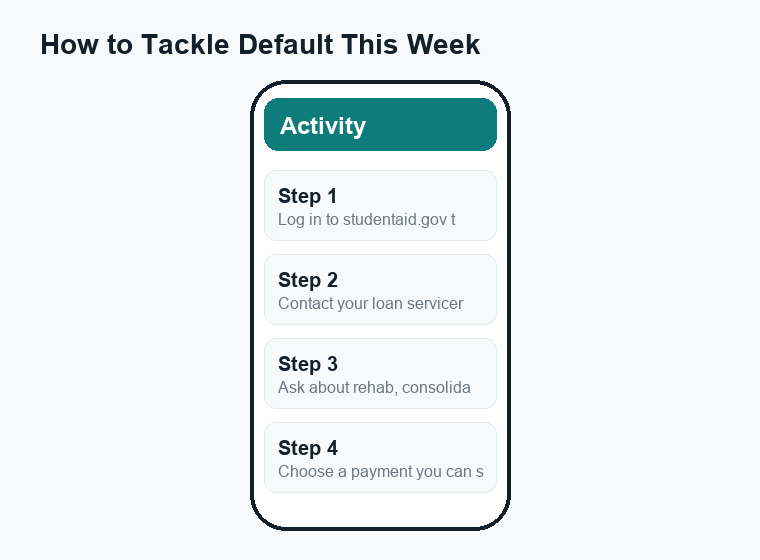

What to do this week if you are behind

Default can feel paralyzing, but the path forward is concrete. If you are delinquent or already in default, take these steps in order.

- Log in to studentaid.gov. Confirm your loan balances, your servicer, and your current status. This is the official source and the safest place to start.

- Contact your loan servicer. Your servicer is listed in your studentaid.gov account. Tell them your situation honestly and ask what options you qualify for.

- Ask specifically about rehabilitation, consolidation, and IDR. Get the monthly payment amounts in writing so you can compare what is affordable.

- Pick the plan you can sustain. The best plan is one you can keep up with every month, not the one with the lowest theoretical payoff.

- Set up autopay if you can. Automatic payments help you avoid the missed-payment slip that starts the slide toward default, and some plans offer a small interest discount for using it.

Watch out for scams

Whenever student loan news spikes, so do scams. Be cautious of any company that calls, texts, or emails promising to “wipe out” your loans, get you instant forgiveness, or fix your default for an upfront fee. The federal options described here, including rehabilitation, consolidation, IDR, and deferment, are free to set up directly through your servicer and studentaid.gov. You never have to pay a third party to access them. Red flags include pressure to act immediately, requests for your studentaid.gov login, and demands for payment before any service is provided. If something feels off, stop and verify through the official channels.

Frequently asked questions

How long does it take to go into default on a federal student loan?

For most federal student loans, default typically happens after roughly 270 days, or about nine months, without a payment. The exact timeline can vary by loan type, so confirm your status with your servicer or at studentaid.gov. Before default, your loan is considered delinquent, which is the stage where late payments start affecting your credit.

Can I get out of default and remove it from my credit report?

Completing loan rehabilitation can remove the record of the default from your credit report, although any late payments reported before default may still appear. Consolidation gets you out of default too, but it generally does not erase the default notation from your credit history. If repairing your credit is a top priority, ask your servicer whether rehabilitation is the better fit for you.

Will my tax refund really be taken if I default?

It can be. Through the Treasury offset process, the government can intercept your federal tax refund and apply it to a defaulted loan, and in some cases a portion of certain federal benefits as well. Resolving the default through rehabilitation or consolidation is the way to stop these collection actions. Because rules can change, verify what applies to your situation at studentaid.gov.

What if I genuinely cannot afford any payment right now?

Talk to your servicer about an income-driven repayment plan, which bases your payment on your income and family size and can be very low for borrowers with limited earnings. If you are facing a short-term hardship, deferment or forbearance can pause payments temporarily, though interest may continue to build during forbearance. The worst choice is to do nothing and let the loan drift toward default.

Is loan forgiveness still available in 2026?

Forgiveness programs and relief efforts exist, but their availability, terms, and deadlines change over time and depend on factors like your loan type and employment. Do not assume any particular program is open or that you automatically qualify. Check the current options at studentaid.gov and confirm details with your servicer rather than trusting promises from outside companies.

The bottom line

The return of student loan defaults in 2026 is a wake-up call for millions of borrowers, but default is not a dead end. Whether you are already in collections or just starting to fall behind, you have proven paths out: rehabilitation, consolidation, income-driven repayment, and temporary deferment or forbearance. The single most important move is to act early, contact your servicer, and verify everything at studentaid.gov before a missed payment turns into something far harder to undo.

For more help managing debt and protecting your money, explore our related WalletWisp guides on budgeting, credit repair, and avoiding financial scams.

{kind=link}