")

If you’re wondering is Venmo FDIC insured, here’s the short version: it depends on how the money is held. Your everyday Venmo balance is generally not FDIC insured on its own, but you can get FDIC pass-through insurance when you enroll in features like Direct Deposit or the Venmo Debit Mastercard, which move your funds into a partner bank. That one distinction trips up a lot of people, and getting it wrong could matter if PayPal (Venmo’s parent company) ever ran into trouble.

In this guide, we’ll break down exactly when your money is covered, when it isn’t, what FDIC “pass-through” insurance actually means, and the simple steps you can take to keep your cash protected. No jargon, no fine-print headaches — just plain answers.

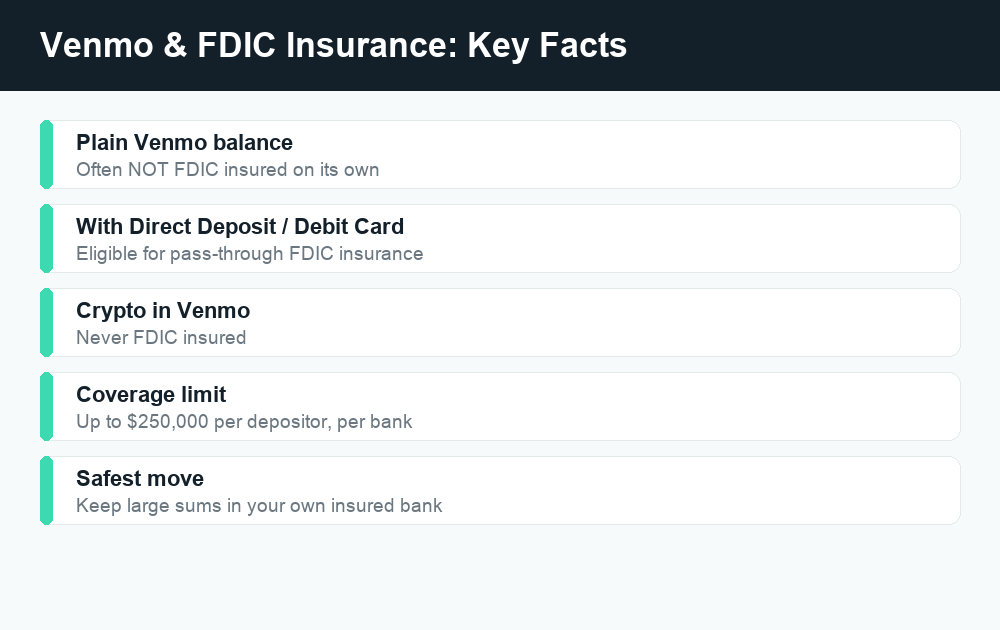

Quick answer: A plain, unused Venmo balance is typically not FDIC insured. However, Venmo offers FDIC pass-through insurance on eligible balances when you enroll in Direct Deposit, set up the Venmo Debit Mastercard, or otherwise hold funds at a partner bank. Crypto held in Venmo is never FDIC insured. To be safest, don’t store large sums in Venmo — move spare cash to your own insured bank account.

What does “FDIC insured” actually mean?

The Federal Deposit Insurance Corporation (FDIC) is a U.S. government agency that protects money you deposit at insured banks. If an FDIC-member bank fails, the FDIC reimburses depositors up to the legal limit — currently $250,000 per depositor, per insured bank, per ownership category. This is why people feel safe keeping money in a checking or savings account: even if the bank collapses, your covered balance is protected.

Here’s the catch that matters for apps like Venmo: FDIC insurance covers banks, not payment apps. Venmo is a financial technology company owned by PayPal, not a chartered bank. So whether your Venmo money is insured comes down to one question — is that money sitting at a partner bank in a way that qualifies for coverage, or is it just floating in your Venmo balance?

Is Venmo FDIC insured? The honest answer

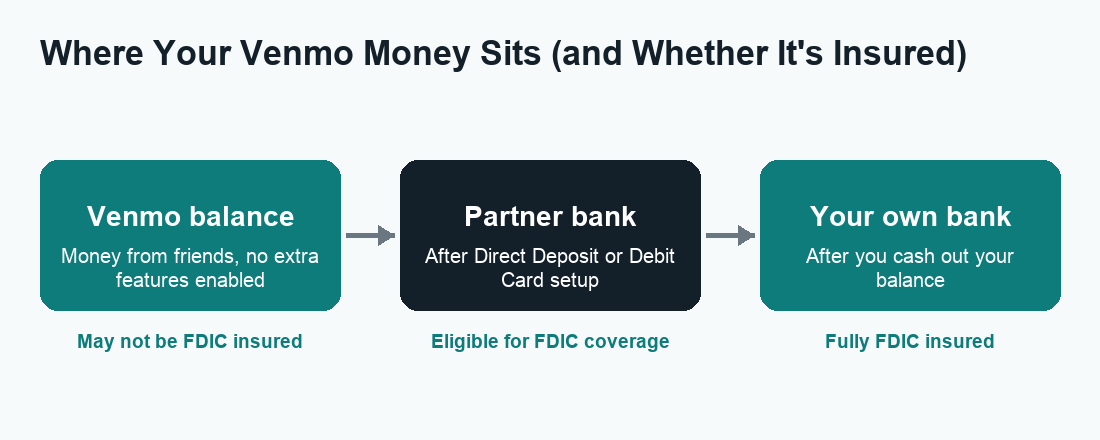

Venmo itself is not a bank, so the app as a whole isn’t “FDIC insured.” Instead, Venmo works with one or more partner banks to provide FDIC pass-through insurance on certain eligible balances. Pass-through insurance means the protection “passes through” Venmo to the underlying bank account — but only if specific conditions are met.

In practice, this is the dividing line:

- Eligible (often covered): Balances tied to features that place your money at a partner bank — most notably when you’ve set up Direct Deposit or activated the Venmo Debit Mastercard. Once you enroll, the funds in your Venmo account can become eligible for pass-through FDIC insurance.

- Not eligible (often not covered): A basic Venmo balance from a friend paying you back, where you’ve never enabled Direct Deposit or the debit card. That money may simply sit in Venmo’s system and not qualify for pass-through coverage.

Because Venmo periodically updates its terms and partner-bank arrangements, the exact eligibility rules can shift. Always confirm your specific situation in the Venmo app or on Venmo’s official help pages before assuming your balance is protected.

Why “pass-through” insurance is conditional

For FDIC pass-through insurance to apply, regulators generally require that the records clearly show the money is held in custody for you (the actual owner) at an FDIC-insured bank. When Venmo routes eligible balances into a partner bank under the right structure, your share can be insured up to the standard limits — combined with any other money you hold at that same bank under the same ownership category. If you already bank with one of Venmo’s partner banks, your combined total at that bank counts toward the single $250,000 limit, not a fresh $250,000.

What’s covered vs. what’s NOT covered in Venmo

This is the part worth memorizing. Not everything inside the Venmo app gets the same treatment.

| What you hold in Venmo | FDIC pass-through insured? | Notes |

|---|---|---|

| Plain Venmo balance (no Direct Deposit / debit card) | Often not insured | May not qualify for pass-through coverage on its own |

| Balance after enrolling in Direct Deposit | Generally eligible | Funds held at a partner bank can qualify |

| Balance tied to the Venmo Debit Mastercard | Generally eligible | Activating the card can make funds eligible |

| Cryptocurrency bought in Venmo | Never FDIC insured | Crypto is not a bank deposit and can lose value |

| Money already moved to your linked bank | Insured by your bank | Standard FDIC coverage at your own bank |

Your Venmo balance

A standalone balance — the kind you build up when friends Venmo you for dinner — is the gray area. If you’ve never enabled the features that route money to a partner bank, that balance may not be FDIC insured. It’s not “gone” or at high risk day to day, but it doesn’t carry the federal safety net of a real bank deposit.

Venmo Debit Card and Direct Deposit

These are the features that flip the switch. When you set up Direct Deposit (having a paycheck or benefits routed to your Venmo account number and routing number) or activate the Venmo Debit Mastercard, your eligible funds are held at a partner bank — and that’s what makes pass-through FDIC insurance possible. If you treat Venmo a bit like a checking account, enabling these is the safer path.

Cryptocurrency in Venmo

This one is simple: crypto is never FDIC insured. Bitcoin, Ethereum, and other coins you buy or hold in Venmo are not bank deposits. They can rise or fall in value, and there is no government reimbursement if their price crashes or if something goes wrong with the crypto service. The FDIC only insures deposits at banks — full stop.

Is Venmo safe to use day to day?

Yes — for most people, Venmo is a reasonable, widely used way to send and receive money. PayPal, its parent company, is a large, regulated, publicly traded financial firm with substantial security infrastructure. The everyday risks with Venmo aren’t really about the company collapsing; they’re about scams, mistaken payments, and account takeovers. FDIC insurance wouldn’t help with any of those anyway — it only covers a bank failure.

So “is my money safe in Venmo?” has two parts:

- Bank-failure safety — addressed by FDIC pass-through insurance on eligible balances (and best handled by not storing big sums in the app).

- Everyday safety — addressed by good security habits and scam awareness, which matter far more for the average user.

The biggest real-world risks

- Scams: Venmo payments to strangers are like handing over cash — usually instant and hard to reverse. Treat “send money to claim a prize,” fake buyer/seller deals, and “accidental payment, please send it back” messages as red flags.

- Sending to the wrong person: Usernames look alike. Once sent, you can only ask the recipient to return it — there’s no guaranteed clawback.

- Account takeover: Phishing texts and SIM-swap attacks target payment apps. Strong authentication is your defense.

How to keep your money safe in Venmo

Whether or not your balance qualifies for FDIC pass-through insurance, these steps reduce your real risk the most:

- Don’t use Venmo as a savings account. Keep only what you plan to spend soon. Move larger amounts to your own FDIC-insured bank, where coverage is automatic and clear.

- Turn on two-factor authentication (2FA) and a device PIN/Face ID lock in Venmo’s security settings.

- Enable Direct Deposit or the Venmo Debit Mastercard if you intend to hold funds in the app, since that’s what can make your balance eligible for pass-through coverage.

- Only pay people you know and trust. For buying from strangers, prefer methods with buyer protection.

- Set your transactions to private so your payment activity isn’t visible to others.

- Cash out regularly. Transfer your balance to your linked bank, where standard FDIC insurance applies to your bank deposits.

- Ignore unsolicited “support” messages. Venmo won’t ask for your password, PIN, or 2FA code. Verify anything through the official app only.

If a transaction is stuck or in limbo, that’s a separate issue from insurance — see our guide on why a Venmo payment is pending to sort it out.

How Venmo compares to Cash App and Zelle on insurance

People often ask the same question about every app. Here’s the broad shape of it — but always verify each app’s current terms directly:

| App | FDIC coverage model | Key nuance |

|---|---|---|

| Venmo | Pass-through on eligible balances (via partner bank) | Usually requires Direct Deposit or debit card; crypto excluded |

| Cash App | Pass-through via partner bank on certain balances | Stocks and Bitcoin are not insured |

| Zelle | No app balance — moves money bank-to-bank | Funds live in your own insured bank account |

Zelle is structurally different: it doesn’t hold a balance at all, so your money stays in your own FDIC-insured bank the whole time. If safety-by-design is your priority, that’s worth knowing. You can read more in our overview of whether Zelle is safe and how long Zelle transfers take.

What happens to your money if Venmo or PayPal failed?

This is the scenario FDIC insurance is built for. If PayPal/Venmo became insolvent, your eligible, pass-through-insured balances at the partner bank should be protected up to the FDIC limits, and you’d recover them through the standard FDIC process. Balances that don’t qualify for pass-through insurance, plus any crypto, would not have that federal backstop — you’d be a general claimant, which is a far weaker position.

It’s worth keeping perspective: a sudden failure of a company the size of PayPal is unlikely, and there’s no reason to panic. But “unlikely” isn’t “impossible,” and that’s precisely why the simplest protection — not parking large sums in the app — is so effective. Your own bank account does the insurance job automatically.

Frequently asked questions

Is Venmo FDIC insured by default?

Not automatically. A basic Venmo balance is often not FDIC insured on its own. Pass-through FDIC insurance typically applies only after you enroll in features like Direct Deposit or the Venmo Debit Mastercard that hold your funds at a partner bank. Confirm your status in the app.

How much of my Venmo money is insured?

FDIC pass-through coverage follows the standard limit — up to $250,000 per depositor, per insured bank, per ownership category. If you also hold money directly at the same partner bank, your balances are combined toward that single limit rather than each getting its own.

Is cryptocurrency in Venmo FDIC insured?

No. Crypto is never FDIC insured. It’s not a bank deposit, its value can go up or down, and there’s no government reimbursement if its price falls or something goes wrong with the service.

Does enabling Direct Deposit make my Venmo balance safer?

Generally, yes, from an insurance standpoint. Direct Deposit (and the Venmo Debit Mastercard) routes eligible funds to a partner bank, which is what can make your balance qualify for pass-through FDIC insurance. It doesn’t protect against scams, though — security habits handle that.

Is my money safer in Venmo or my own bank?

Your own FDIC-insured bank is the clearer, simpler option — coverage is automatic and not dependent on which app features you’ve enabled. A good rule of thumb is to keep only spending money in Venmo and move the rest to your bank.

Can I lose money if Venmo gets hacked?

FDIC insurance does not cover fraud or hacking — it only covers a bank failure. To protect against account takeover, turn on two-factor authentication, use a device lock, never share codes, and ignore unsolicited “support” messages. Report unauthorized activity to Venmo right away.

If I send money to the wrong person, will FDIC cover it?

No. FDIC insurance has nothing to do with mistaken or scam payments. Venmo transfers are usually instant and hard to reverse, so double-check the username and amount before sending. If you suspect fraud, contact Venmo through official channels and, if needed, report it to the CFPB.

Where can I verify Venmo’s current FDIC terms?

Check the Venmo app’s help/legal section and Venmo’s official website for the most current language, and consult the FDIC’s own resources at fdic.gov for how pass-through insurance works. Be wary of third-party sites or DMs claiming to be Venmo support.

The bottom line

Venmo isn’t a bank, so it isn’t “FDIC insured” as a whole. What you get is conditional pass-through insurance on eligible balances — usually once you’ve set up Direct Deposit or the Venmo Debit Mastercard — while plain balances and all crypto sit outside that protection. The cleanest way to stay safe is also the easiest: keep only what you’ll spend in the app, use strong security, stay alert to scams, and let your own insured bank account hold the rest. For more on how the app works in practice, our guide to Venmo fees and the broader Venmo resources are good next stops.

Last updated: June 2026. Fees, limits, and features can change — always confirm current details in the app. WalletWisp is an independent guide and is not affiliated with any app mentioned. This article is general information, not financial advice.

Related: Venmo fees explained · Is Zelle safe? · More Venmo guides

")

")

")

{kind=link}