The Apple Card is a no-fee, iPhone-first rewards credit card built around Daily Cash: you earn 3% back at Apple and select partner merchants, 2% on any Apple Pay purchase, and 1% when you swipe the titanium physical card. It charges no annual fee, no foreign transaction fees, and no late fees, and it pairs with a high-yield Apple Card Savings account. For 2026, the Apple Card remains one of the simplest cards for people deep in the Apple ecosystem, though flat-rate rivals like the new Robinhood Gold Card now beat it on raw cash back.

Below we break down exactly how the rewards work, the real fee structure, the current Savings APY range, who issues the card, the credit score you likely need to get approved, how Apple Card Family works, and how it stacks up against Robinhood Gold.

How Apple Card Daily Cash rewards work

The Apple Card’s rewards program is called Daily Cash, and the name is literal: your cash back lands in your Apple Cash balance (or Apple Card Savings) every day as transactions post, rather than once a month. There are no rotating categories to activate and no spending caps on how much you can earn.

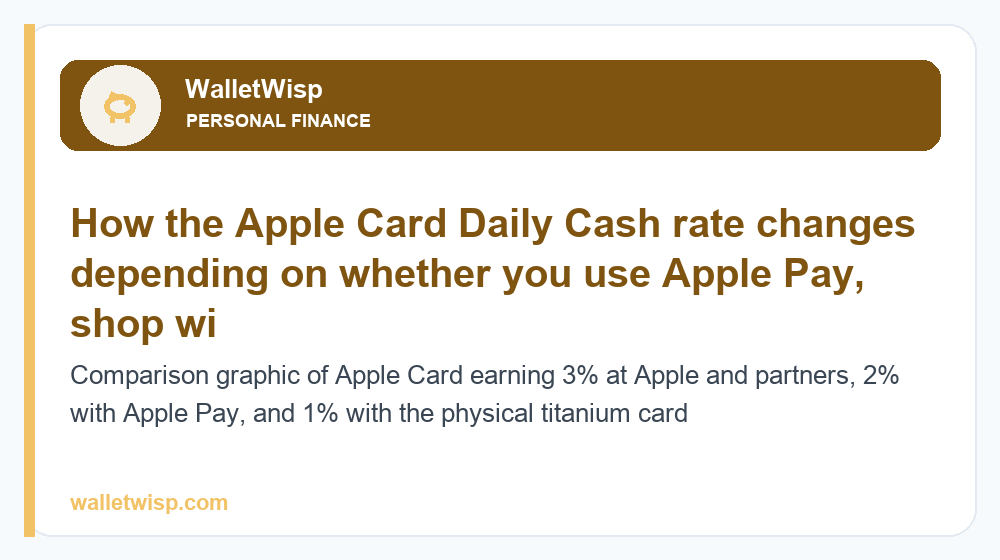

The rate you get depends on how you pay, which is the key quirk of this card. Using Apple Pay from your iPhone or Apple Watch earns more than swiping the physical card.

| How you pay | Daily Cash rate | Examples |

|---|---|---|

| Directly with Apple | 3% | Apple Store, App Store, apple.com, Apple TV+, iCloud+, Apple Music |

| Select partner merchants (via Apple Pay) | 3% | Uber & Uber Eats, Walgreens, Nike, T-Mobile, Exxon/Mobil, Ace Hardware, Panera Bread |

| Any other purchase with Apple Pay | 2% | Groceries, restaurants, gas, online checkout where Apple Pay is accepted |

| Physical titanium card (chip/swipe) | 1% | Any merchant that doesn’t take Apple Pay |

The practical takeaway: to get real value from the Apple Card you need to use Apple Pay as much as possible. If you frequently swipe the physical card, you’re earning just 1% and a basic 2% flat-rate card would beat it everywhere. Because Daily Cash posts to Apple Cash, it’s worth understanding the balance and transfer rules — see our guide to Apple Cash limits in 2026 before you route large amounts through it.

Apple Card fees: what you actually pay

Fee transparency is the Apple Card’s strongest selling point. It carries essentially no consumer fees, which is rare even among premium no-annual-fee cards.

| Fee type | Apple Card |

|---|---|

| Annual fee | $0 |

| Foreign transaction fee | $0 |

| Late payment fee | $0 |

| Over-limit fee | $0 |

| Returned payment fee | $0 |

| Purchase APR (variable, 2026 estimate) | ~18% – 29% based on creditworthiness |

| Cash advance fee | Not offered (no cash advances) |

There’s an important nuance: while the Apple Card charges no late fee, missing a payment still adds interest to your balance and can be reported to the credit bureaus, which hurts your score. “No late fee” means no penalty charge, not consequence-free. The variable APR range above is an estimate for 2026 and moves with the prime rate, so check your own offer for the exact number.

Apple Card Savings account and APY

Apple Card holders can open a linked high-yield Savings account with no fees, no minimum deposit, and no minimum balance. You can route your Daily Cash straight into it automatically, and you can also transfer money in from a linked bank account.

The Savings APY is variable. It peaked well above 4% during the high-rate era of 2023–2024, but as the Federal Reserve trimmed rates through 2025, the yield drifted lower. For 2026, expect the APY to sit somewhere in the roughly 3.5%–4.0% range (an estimate — always confirm the live rate in the Wallet app, since it changes without notice). That’s still competitive with mainstream online savings accounts, but it’s no longer a category leader, and it requires staying inside the Apple ecosystem. If you’re chasing the best return on cash, compare it against current promos in our roundup of the best bank account bonuses for 2026.

Who is the Apple Card issuer?

Since launch in 2019, the Apple Card has been issued by Goldman Sachs, with Mastercard as the payment network. That partnership is in transition. Goldman has been winding down its consumer-banking arm, and Apple has been reported to be lining up a new banking partner (JPMorgan Chase has been widely reported as a frontrunner in talks) to take over the program, with a handover that may complete in 2026.

For cardholders, an issuer change should be largely behind the scenes — the card, the Wallet-app experience, and Daily Cash are Apple-branded regardless of which bank sits behind them. Still, terms such as the APR range and Savings APY are ultimately set by the issuing bank, so a new partner could adjust them over time. Treat any specific rate in this article as a 2026 estimate and verify the current figures before applying.

Apple Card approval and credit score needed

There’s no published hard cutoff, but based on reported approvals the Apple Card typically targets applicants with fair-to-good credit, roughly a 600+ FICO score, with the best APRs reserved for good-to-excellent credit (670 and up). Some thin-file and rebuilding applicants have been approved, which makes it more accessible than many premium rewards cards.

The application runs in the Wallet app and takes minutes. A helpful feature: Apple shows you your offer — credit limit and APR — based on a soft pull before you accept, so checking your terms won’t ding your credit. Only when you accept the card does a hard inquiry hit your report.

Factors that improve your odds of approval and a better APR:

- On-time payment history across your existing accounts

- Low credit utilization (ideally under 30% of your limits)

- Verifiable income relative to requested spending power

- Limited recent hard inquiries and new accounts

If your score is on the edge, it’s worth spending a few months strengthening it first. Our step-by-step guide to improving your credit score in 2026 covers the fastest levers, and the Apple Card itself can then help maintain a healthy score once you’re approved, since it reports to all three bureaus.

Apple Card Family: sharing and co-owning

Apple Card Family lets you share one Apple Card with up to five people in your Family Sharing group. It comes in two flavors:

- Co-owners: Two people share equal responsibility for one account, can merge their existing Apple Card lines into a shared line, and both build credit history on the account. Both must be 18 or older.

- Participants: Family members age 13+ can be added as participants with their own optional spending limits and Daily Cash. The organizer can set controls and monitor activity.

This makes the Apple Card unusual: it’s one of the few cards where two people can genuinely co-own an account and build credit together, rather than one person being a secondary authorized user. It’s useful for couples merging finances or for parents helping a teen establish responsible spending habits with guardrails.

Apple Card pros and cons

Pros

- No annual, foreign transaction, late, or over-limit fees

- Daily Cash pays out every day with no caps or rotating categories

- 3% back at Apple and a solid roster of everyday partner merchants

- Fast in-app application with a soft-pull pre-approval offer

- Genuinely useful budgeting tools and clear spending summaries in Wallet

- Linked high-yield Savings and true co-ownership via Apple Card Family

- Strong privacy and security (unique numbers, no printed card number)

Cons

- Only 1% back when you use the physical card — you must use Apple Pay to win

- No welcome bonus and no 0% intro APR offer

- iPhone required; not useful for Android users

- Rewards live in the Apple ecosystem (Apple Cash/Savings)

- Flat-rate rivals now offer 3% on everything, beating the 2% Apple Pay tier

- Issuer transition adds some uncertainty to future terms

Apple Card vs the new Robinhood Gold Card

The most talked-about challenger in 2026 is the Robinhood Gold Card, which flips the Apple Card’s model on its head by paying a flat 3% cash back on everything — but only if you pay for a Robinhood Gold membership. Here’s how the two compare.

| Feature | Apple Card | Robinhood Gold Card |

|---|---|---|

| Base rewards | 1% physical / 2% Apple Pay / 3% Apple & partners | 3% flat on all categories (5% on travel via portal) |

| Annual/membership cost | $0 | Requires Robinhood Gold (~$5/month or ~$50/year) |

| Issuer | Goldman Sachs (transitioning) | Coastal Community Bank |

| Network | Mastercard | Visa |

| Foreign transaction fee | $0 | $0 |

| Card material | Titanium | Metal (stainless/tungsten tiers) |

| Best for | Apple ecosystem users who tap Apple Pay | Robinhood users who want flat 3% everywhere |

| Availability | Widely available | Rolling out from a waitlist |

The math is straightforward. If most of your spending happens where Apple Pay is not accepted, or you don’t want to swipe your phone, the Robinhood Gold Card’s flat 3% will out-earn the Apple Card’s 1%–2% — as long as your rewards exceed the ~$50–$60 annual Gold cost (breakeven is around $2,000–$6,000 of spend depending on how you’d otherwise earn). But the Robinhood card requires an active Gold subscription and ties you to the Robinhood app, and availability is still limited.

The Apple Card wins on simplicity and zero cost: there’s no membership to maintain, no breakeven to clear, and the ecosystem tools (Savings, Family, budgeting) are genuinely good. For heavy Apple Pay users who also spend at partners like Uber, T-Mobile, and Walgreens, the effective earn rate creeps toward 3% anyway, closing much of the gap.

Who should get the Apple Card in 2026?

Get the Apple Card if you own an iPhone, use Apple Pay routinely, spend meaningfully with Apple or its partner merchants, and value a genuinely fee-free card with clean budgeting tools and a decent linked savings account. It’s also a strong pick for couples wanting to co-own an account or parents introducing a teen to credit.

Look elsewhere if you’re on Android, prefer swiping a physical card, want a sign-up bonus or a 0% intro APR, or simply want the highest flat cash-back rate — in which case a no-fee 2% card or the Robinhood Gold Card may serve you better. As always, only apply if you can pay the balance in full each month, because the variable APR will quickly erase any rewards you earn.

Frequently Asked Questions

Does the Apple Card have an annual fee?

No. The Apple Card charges no annual fee, no foreign transaction fee, no late fee, no over-limit fee, and no returned payment fee. Your only real cost is interest if you carry a balance, so paying in full each month keeps the card effectively free.

What credit score do I need for the Apple Card?

There’s no official minimum, but reported approvals suggest you generally want fair-to-good credit, roughly a 600+ FICO score, with the best APRs going to those at 670 and above. You can see your personalized offer via a soft credit pull before accepting, so checking won’t hurt your score.

Who is the Apple Card issuer in 2026?

The Apple Card has been issued by Goldman Sachs on the Mastercard network. Goldman is exiting consumer banking, and Apple has been reported to be moving to a new banking partner (JPMorgan Chase has been widely reported in talks), with a possible handover in 2026. The Apple-branded experience should stay the same regardless.

How does Apple Card Daily Cash actually work?

You earn 3% back at Apple and select partner merchants, 2% on any Apple Pay purchase, and 1% on physical-card transactions. The cash back posts daily to your Apple Cash balance or Apple Card Savings, with no caps and no categories to activate.

What is the Apple Card Savings APY right now?

It’s a variable rate that we estimate is around 3.5%–4.0% for 2026, down from its 4%+ peak as interest rates fell. The account has no fees and no minimums. Always confirm the live APY in the Wallet app, since it can change at any time.

Is the Apple Card better than the Robinhood Gold Card?

It depends on your habits. The Robinhood Gold Card pays a flat 3% on everything but requires a paid Robinhood Gold membership (~$50–$60/year). The Apple Card is free and rewards Apple Pay use. If you spend a lot outside Apple Pay, Robinhood likely earns more; if you want zero cost and Apple ecosystem tools, the Apple Card wins.

Can two people share an Apple Card?

Yes, through Apple Card Family. Two adults can be co-owners of one shared account and both build credit, and family members age 13+ can be added as participants with optional spending limits. You can share with up to five people in your Family Sharing group.

Does using the Apple Card help build credit?

Yes. The Apple Card reports to all three major credit bureaus, so on-time payments and low utilization can help build or maintain your score. Just remember that although there’s no late fee, a missed payment still accrues interest and can be reported, which would hurt your credit.

")

{kind=link}