SoFi Checking and Savings is a single online bank account that combines a high-yield savings side, a checking side and a debit card, with no monthly fees and no minimum balance. When you set up qualifying direct deposit (or deposit at least $5,000 every 30 days), the savings portion earns a strong variable APY of roughly 3.80% as of early 2026 (rate is variable and can change), checking earns a small APY, and you can qualify for a cash sign-up bonus of up to $300. Without direct deposit, you still get a fee-free account but earn a much lower base rate.

SoFi (short for Social Finance) is a chartered bank — SoFi Bank, N.A., Member FDIC — so your deposits are federally insured. It is best for people who route their paycheck through direct deposit and want one simple app that handles spending and saving together. Below is a full 2026 breakdown of the rates, the direct-deposit rules, fees, Vaults, overdraft coverage and the FDIC partner-bank program, plus exactly who should (and shouldn’t) open one.

What is SoFi Checking and Savings?

Unlike most banks that sell checking and savings as separate products, SoFi bundles them into one account you open together. You get a checking balance for everyday spending, a linked high-yield savings balance for your goals, a Mastercard debit card, and access to “Vaults” — sub-accounts inside savings that let you separate money by goal. Everything lives in the SoFi mobile app or website.

Key headline features in 2026 include no monthly maintenance fee, no account-minimum fee, no overdraft fee, fee-free access to 55,000+ Allpoint ATMs, the option to get paid up to two days early with direct deposit, and automatic “Roundups” that sweep spare change into savings. The catch — and it is the central thing to understand — is that SoFi’s best perks (top APY, overdraft coverage, cash bonus) are gated behind direct deposit.

SoFi Checking and Savings APY in 2026

The SoFi Checking and Savings APY is tiered based on whether you have qualifying direct deposit. Rates are variable and SoFi adjusts them in line with the broader rate environment, so treat the figures below as representative early-2026 estimates rather than a locked-in promise.

APY with direct deposit

Members who receive qualifying direct deposits — or who deposit $5,000 or more in the prior 30 days — earn the top savings APY, around 3.80%. This top rate also applies to money held inside Vaults, so organizing your savings into goals does not cost you any interest. The checking balance earns a smaller APY (around 0.50%), which is still better than the near-zero rate at most big brick-and-mortar banks.

APY without direct deposit

If you skip direct deposit and don’t hit the $5,000 deposit threshold, the savings rate drops sharply to a base rate near 1.00%. That is still positive, but it defeats the main reason to bank with SoFi. If you can’t or don’t want to move your paycheck, a standalone high-yield savings account may serve you better — compare current options in our roundup of the best high-yield savings rates for 2026.

| Feature | Details (early 2026, estimates) |

|---|---|

| Savings APY (with direct deposit) | Up to ~3.80% variable |

| Savings APY (no direct deposit) | ~1.00% variable base rate |

| Checking APY | ~0.50% variable |

| Monthly maintenance fee | $0 |

| Minimum opening deposit | $0 |

| Overdraft fee | $0 (coverage up to $50 with qualifying direct deposit) |

| ATM network | 55,000+ Allpoint, fee-free |

| Sign-up bonus | Up to $300 with direct deposit (tiered) |

| FDIC insurance | Standard $250K; up to $2M via partner-bank program |

| Early paycheck | Up to 2 days early with direct deposit |

The direct-deposit requirement, explained

“Qualifying direct deposit” is the phrase that unlocks nearly everything good about the account, so it’s worth understanding precisely. A qualifying direct deposit is an electronic ACH deposit of a paycheck, pension or government benefit from your employer, payroll provider or a benefits payer. One-off transfers you push from another bank, mobile check deposits, and most peer-to-peer transfers (like a friend sending you money) generally do not count.

SoFi gives you a second path: instead of direct deposit, you can qualify by receiving $5,000 or more in total qualifying deposits during the prior 30-day evaluation period. That alternative is useful for freelancers, gig workers and the self-employed who don’t have a traditional employer payroll but move enough money through the account. If you meet either bar, you get the top APY, overdraft coverage and access to the bonus. Miss both, and you fall back to the base rate.

SoFi sign-up bonus in 2026

SoFi regularly offers a cash welcome bonus for new members who set up direct deposit within a promotional window (commonly the first 25–30 days after opening). The bonus is tiered by how much direct deposit you receive, and the top tier has typically been $300. Exact amounts and windows change, so confirm the current offer at sign-up. A representative tier structure looks like this:

| Total qualifying direct deposit (in promo window) | Typical bonus |

|---|---|

| $1,000 – $4,999.99 | ~$50 |

| $5,000 or more | ~$300 |

Because the account has no monthly fee and no minimum, a bonus like this is close to free money for anyone already planning to move their paycheck. If bonus-hunting is your priority, it’s worth cross-shopping — see our list of the best bank account bonuses for 2026 before you commit, since a competing offer may pay more for the same direct deposit.

Fees, overdraft and ATM access

SoFi’s fee structure is genuinely lean, which is one of its strongest selling points. There is no monthly maintenance fee, no minimum-balance fee, and no fee to open. In-network ATM withdrawals across the 55,000+ Allpoint network are free; out-of-network and international ATM operators may still charge their own fees, and SoFi generally does not reimburse third-party ATM surcharges.

On overdrafts, SoFi charges no overdraft fees. Better still, members who receive at least $1,000 in qualifying direct deposits in the prior 30 days can get free overdraft coverage up to $50 — SoFi covers small shortfalls on debit purchases and the negative balance is squared up on your next deposit, with no fee. That is a meaningful safety net compared with legacy banks that historically charged $35 per overdraft item.

Vaults and Roundups

Vaults are SoFi’s savings sub-accounts. Instead of opening multiple savings accounts, you create named Vaults — say “Emergency Fund,” “Vacation” and “New Car” — inside your single savings balance. Each Vault earns the same savings APY as the main balance, and you can automate contributions or set target amounts. It’s a simple, effective way to practice goal-based saving without juggling several institutions.

Roundups pair with Vaults: turn it on and SoFi rounds each debit-card purchase up to the next dollar and sweeps the difference into a Vault of your choice. A $4.30 coffee moves $0.70 into savings. It’s a low-effort way to build a cushion in the background. SoFi also offers debit-card cash-back rewards at select merchants from time to time, though the specific offers rotate.

FDIC insurance and the partner-bank program

Your money at SoFi is protected. The account is held at SoFi Bank, N.A., Member FDIC, so standard federal deposit insurance of $250,000 per depositor applies automatically. For savers with larger balances, SoFi offers expanded coverage through its SoFi Insured Deposit Program, which spreads your deposits across a network of participating partner banks. Through that program, eligible balances can be insured up to $2 million (and more for joint accounts), well beyond the standard $250,000 cap at a single bank.

This is the same “sweep to program banks” model that many fintechs and cash-management accounts use, but it’s worth knowing the mechanics: the extra insurance above $250,000 comes from your funds being held at multiple FDIC-insured partner banks, not from a single higher limit at SoFi. For the vast majority of everyday savers keeping under $250,000, the standard FDIC coverage already has you fully protected.

SoFi vs. Chime vs. a traditional bank

SoFi competes with other app-first banks and with legacy institutions. The table below shows how it stacks up on the features that matter most. Chime, another popular fintech, takes a similar direct-deposit-first approach; if you’re weighing the two, our detailed Chime high-yield savings 2026 breakdown covers its rates and rules.

| Feature | SoFi | Chime | Typical big bank |

|---|---|---|---|

| Top savings APY (est. 2026) | ~3.80% | ~2.00% | ~0.01–0.05% |

| Checking earns interest | Yes (~0.50%) | No | Usually no |

| Monthly fee | $0 | $0 | $0–$15 |

| Requires direct deposit for top perks | Yes (or $5K/30 days) | Yes | Varies |

| Sign-up bonus | Up to ~$300 | Occasional/referral | Sometimes $200–$400 |

| Physical branches | No | No | Yes |

| Extended FDIC coverage | Up to $2M (partner banks) | Standard $250K | Standard $250K |

Pros and cons of SoFi Checking and Savings

Pros:

- Competitive high-yield savings APY (up to ~3.80%) when you use direct deposit.

- Checking also earns interest — rare among free accounts.

- No monthly, minimum-balance or overdraft fees.

- Cash sign-up bonus up to $300 for new direct deposits.

- Vaults and Roundups make goal-based saving easy.

- Up to $2M FDIC coverage via the partner-bank program.

- Paycheck up to two days early and fee-free overdraft up to $50.

Cons:

- Best rate requires direct deposit or $5,000 in monthly deposits; otherwise APY drops to ~1.00%.

- No physical branches — fully digital, so no in-person service.

- Cash deposits are inconvenient (must use retail partners, often with a fee).

- Rates are variable and have fallen from their 2023–2024 peaks.

- Out-of-network ATM surcharges generally aren’t reimbursed.

Who SoFi Checking and Savings is best for

SoFi is an excellent fit if you have a steady paycheck you can route via direct deposit, want your checking and savings in one clean app, and value earning interest on your spending balance while keeping fees at zero. It rewards people who consolidate — the more of your banking life runs through it, the more the perks (top APY, bonus, overdraft coverage, early pay) actually apply.

It’s a weaker choice if you rely on cash deposits, want a branch you can walk into, or can’t commit to direct deposit — in which case a dedicated high-yield savings account without a direct-deposit hurdle will likely earn you more. Chasing the very highest savings yield alone? A standalone HYSA sometimes edges out SoFi’s rate, so it’s worth comparing before deciding whether the all-in-one convenience is worth it.

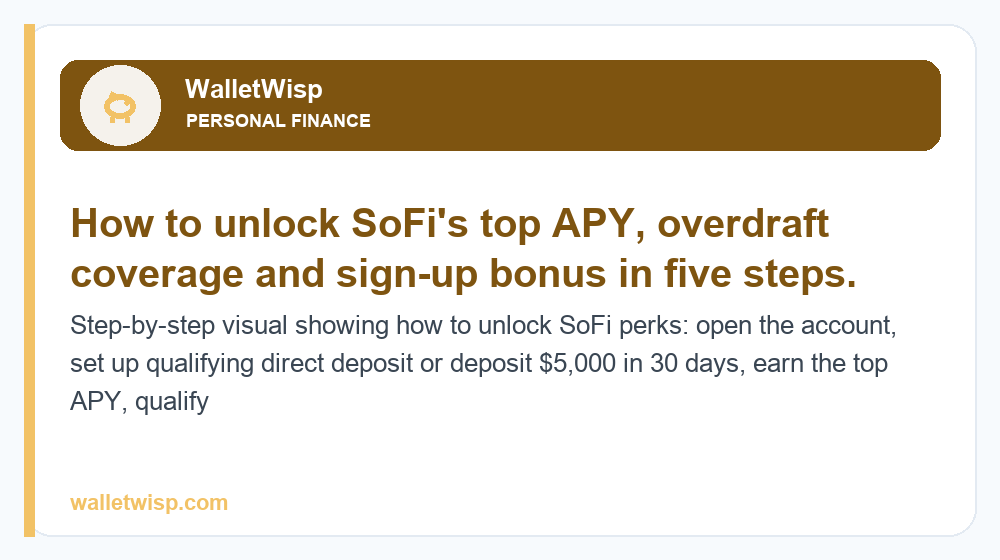

How to open a SoFi account

- Apply online or in the SoFi app — you’ll need your Social Security number, ID and basic personal details. There’s no minimum to open.

- Fund the account with an initial transfer (optional) so it’s ready to go.

- Set up qualifying direct deposit with your employer or payroll provider — this is what unlocks the top APY, overdraft coverage and the bonus.

- Receive enough direct deposit within the promo window to earn your tiered welcome bonus.

- Turn on Roundups and create Vaults to automate your saving.

Frequently Asked Questions

Is SoFi Checking and Savings a real bank account?

Yes. It’s a genuine deposit account issued by SoFi Bank, N.A., Member FDIC. SoFi obtained a national bank charter, so it holds and insures deposits directly rather than relying solely on a partner bank for the base account.

What is the SoFi savings APY in 2026?

As of early 2026, the savings side earns up to roughly 3.80% APY with qualifying direct deposit and about 1.00% without it. Checking earns around 0.50%. All figures are variable and can change with market conditions, so verify the live rate before opening.

Do I really need direct deposit to earn the top rate?

To earn the top APY you need qualifying direct deposit or at least $5,000 in total qualifying deposits during the prior 30 days. Without either, your savings rate drops to the roughly 1.00% base rate, though the account stays fee-free.

How much is the SoFi sign-up bonus?

The bonus is tiered, historically up to $300 for $5,000+ in direct deposits and about $50 for $1,000–$4,999, within a promotional window after opening. Exact amounts and terms change, so confirm the current offer at sign-up.

Does SoFi charge overdraft or monthly fees?

No. There are no monthly maintenance fees, no minimum-balance fees and no overdraft fees. Members with at least $1,000 in monthly qualifying direct deposits can also get free overdraft coverage up to $50.

How does SoFi’s FDIC insurance work?

Standard FDIC insurance of $250,000 per depositor applies automatically. Through the SoFi Insured Deposit Program, eligible balances can be insured up to $2 million by spreading deposits across partner banks — useful for savers holding more than the standard limit.

What are SoFi Vaults?

Vaults are savings sub-accounts inside your main balance that let you separate money by goal, such as an emergency fund or a vacation. Each Vault earns the same savings APY, and you can automate contributions and pair them with Roundups.

Is SoFi better than Chime or a traditional bank?

SoFi typically offers a higher savings APY than Chime and far more than legacy banks, plus interest on checking. Chime and traditional banks have their own strengths — Chime for a simple spend-and-save flow, big banks for branches and cash deposits. The best choice depends on whether you’ll use direct deposit and value an all-in-one app.

")

{kind=link}