To improve your credit score, focus on two things first: pay every bill on time and keep your credit card balances low relative to your limits. Those two habits drive the majority of your score, and you can start both today for free.

Quick answer: Your credit score is mostly built on payment history (about 35%) and how much of your available credit you use (about 30%). Set up autopay so you never miss a due date, get your card utilization below 30% (ideally under 10%), don’t close your oldest cards, and dispute any errors on your credit reports for free at AnnualCreditReport.com. Most positive changes show up within one to three months, so be consistent and patient.

What a credit score actually is

A credit score is a three-digit number that lenders use to estimate how likely you are to repay borrowed money. The most widely used scores in the United States are FICO scores, which generally range from 300 to 850. The higher your number, the lower the risk you appear to be, which usually means easier approvals and better interest rates on credit cards, car loans, and mortgages.

Your score is calculated from the information in your credit reports, which are maintained by the three major credit bureaus: Equifax, Experian, and TransUnion. Each bureau collects data from lenders about your accounts, balances, payment history, and more. Because lenders don’t always report to all three bureaus, your score can differ slightly depending on which report it’s based on. That’s normal.

One important mindset shift for beginners: you don’t have a single, permanent score. You have a range of scores that move up and down as your reports update, typically every month. Improving your credit is a process of building good habits and letting them compound over time, not a one-time fix.

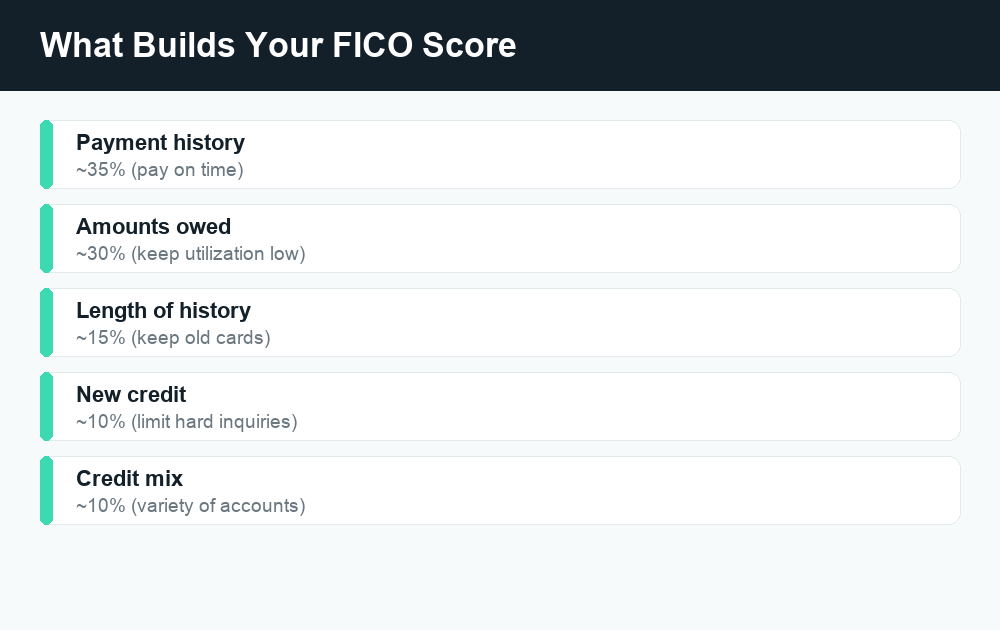

The five FICO factors and roughly how much each matters

FICO scores are built from five categories of information. Knowing the rough weight of each one tells you exactly where to spend your effort. The percentages below are approximate and can vary from person to person, but they’re a reliable guide for prioritizing.

| Factor | Rough weight | What it measures |

|---|---|---|

| Payment history | ~35% | Whether you pay bills on time |

| Amounts owed (utilization) | ~30% | How much of your available credit you use |

| Length of credit history | ~15% | How long your accounts have been open |

| New credit | ~10% | Recent applications and newly opened accounts |

| Credit mix | ~10% | The variety of accounts you manage |

Notice that the top two factors together make up roughly 65% of your score. If you do nothing else, getting these two right will move the needle more than any other tactic. The remaining three factors matter, but they reward patience and consistency more than quick action.

Step 1: Always pay on time, and let autopay do the remembering

Payment history is the single largest factor, so a missed payment hurts more than almost anything else you can do. A payment is typically reported as late once it’s 30 days past due, and a single late mark can stay on your report for years. The good news is that this is the easiest factor to control.

Set up autopay for at least the minimum payment on every credit card and loan. This guarantees you never miss a due date because life got busy. If you can, set autopay to cover the full statement balance so you also avoid interest charges. Keep a small buffer in your checking account so an autopay never bounces.

If you’ve missed payments in the past, don’t panic. The impact of a late payment fades over time as you build a streak of on-time payments behind it. The most powerful thing you can do is make sure today’s payment, and every payment from here forward, is on time.

Step 2: Lower your credit utilization

Credit utilization is the percentage of your available credit that you’re currently using, and it’s the second-biggest factor at about 30%. If you have a $1,000 limit and a $500 balance, your utilization on that card is 50%. Lenders generally like to see this number low, because high utilization can signal that you’re stretched thin.

A common rule of thumb is to keep utilization below 30%. If you want to optimize, aim for under 10%. This applies both to each individual card and to your total across all cards. Here are practical ways to bring it down:

- Pay down balances before the statement closing date, not just the due date. The balance reported to the bureaus is usually the one on your statement, so paying early can lower the number that gets reported.

- Make a mid-cycle payment. Paying twice a month keeps your reported balance lower without changing how much you spend.

- Ask for a credit limit increase. A higher limit with the same spending automatically lowers your utilization. Just be careful not to treat the extra room as a license to spend more.

- Spread spending across cards so no single card is maxed out.

Because utilization is recalculated each time your balances are reported, this is one of the fastest-moving levers you have. Pay a card down significantly, and you may see the effect on your next score update.

Step 3: Don’t close your old credit cards

It’s tempting to close a card you rarely use, but closing it can backfire in two ways. First, length of credit history accounts for about 15% of your score, and your oldest accounts help raise the average age of your credit. Closing an old card can shorten that history over time. Second, closing a card removes its credit limit from your total available credit, which can push your utilization percentage up even if your spending hasn’t changed.

Instead of closing an old card, keep it open and active with a small recurring charge, like a streaming subscription, paid off automatically each month. If the card has an annual fee you no longer want to pay, ask the issuer whether you can downgrade to a no-fee version of the card rather than closing it outright, which often preserves the account’s age.

Step 4: Limit hard inquiries and apply for credit only when you need it

When you apply for new credit, the lender usually performs a “hard inquiry” on your report. New credit makes up about 10% of your score, and each hard inquiry can lower your score by a small amount temporarily. A handful of inquiries usually isn’t a big deal, but several in a short window can add up and may signal risk to lenders.

A few practical guidelines:

- Space out applications. Apply for new cards or loans only when you actually need them, not just for a sign-up bonus you don’t have a plan for.

- Use prequalification tools when available. Many issuers let you check your odds with a “soft” inquiry that doesn’t affect your score.

- Rate shopping is treated gently. When you’re shopping for a single loan like a mortgage or auto loan, multiple inquiries within a short shopping window are typically grouped and counted as one, so comparison shopping for one loan generally won’t pile up penalties.

Step 5: Check your reports and dispute errors for free

Errors on your credit reports are more common than people expect, and a mistake, like a payment marked late that you actually paid on time, or an account that isn’t yours, can drag your score down for no reason. Fixing one can give your score a legitimate boost.

The official, government-authorized source for your free credit reports from all three bureaus is AnnualCreditReport.com. It’s free, and you should use it rather than lookalike sites that try to charge you or upsell subscriptions. Review each report for:

- Accounts you don’t recognize (a possible sign of identity theft)

- Payments marked late that you paid on time

- Wrong balances or credit limits

- Duplicate accounts

- Personal information errors

If you find a mistake, you can dispute it directly with the credit bureau that’s reporting it, usually online, by mail, or by phone. The bureau is required to investigate. Keep records of what you submit. Because each bureau may have different information, it’s worth checking all three.

Step 6: Build credit with a secured card or as an authorized user

If you have little or no credit history, or you’re rebuilding after a rough patch, two beginner-friendly tools can help you establish a positive track record.

Secured credit cards

A secured card requires a refundable cash deposit that typically becomes your credit limit. You use it like a normal card and pay it off each month, and the issuer reports your good behavior to the bureaus. Over time, responsible use can help you build history and qualify for an unsecured card. When choosing one, look for a card that reports to all three bureaus, has low or no fees, and offers a path to graduate to a regular card and get your deposit back.

Becoming an authorized user

If someone you trust, such as a family member, adds you as an authorized user on their well-managed credit card, that account’s positive history can sometimes appear on your report and help your score. This works best when the primary cardholder has a long history of on-time payments and low utilization. Make sure you both understand the arrangement, because their behavior on that card can affect you too.

Be patient: improvements take time

Credit building is a marathon, not a sprint. Some changes, like lowering your utilization, can show up on your next score update within a billing cycle. Others, like the fading impact of a late payment or a longer average account age, take months or years to fully play out. As a general expectation, meaningful improvement often takes one to three months or more of consistent habits.

Be wary of anyone promising to “fix” your credit overnight or to legally remove accurate negative information for a fee. Legitimate negative marks generally have to age off your report over time, and no one can erase truthful information early. If a service sounds too good to be true, it usually is.

Common credit score myths, busted

A lot of credit “advice” passed around online is simply wrong and can cost you money. Here are two of the most persistent myths.

| Myth | The reality |

|---|---|

| Checking my own score hurts it | Checking your own score is a “soft” inquiry and does not affect your score. Check it as often as you like. |

| I should carry a balance to build credit | You don’t need to carry a balance or pay interest. Paying your statement in full each month still builds positive history. |

Two more worth knowing: closing a card does not erase its history immediately, but it can hurt your utilization and eventually your average account age, so it’s rarely a quick win. And income is not part of your FICO score, though lenders may ask for it separately when deciding how much credit to extend.

Free tools to track your progress

You don’t need to pay for credit monitoring to keep an eye on your score. Many banks and credit card issuers now show a free FICO or VantageScore right inside your account dashboard or mobile app. Several free apps and websites also offer score tracking, often funded by showing you card and loan offers, so you can watch your number move as your habits improve.

Remember that the free score you see may use a slightly different model or bureau than a specific lender pulls, so treat it as a directional guide rather than an exact prediction. The trend over time is what matters most. For free copies of the underlying reports themselves, always go to AnnualCreditReport.com.

Frequently asked questions

How long does it take to improve my credit score?

It depends on what you change and where you’re starting. Lowering your credit utilization can show up within a single billing cycle once your new balance is reported. Other improvements, like a late payment losing its sting or your accounts aging, take longer. Plan on one to three months or more of consistent good habits to see meaningful movement, and longer to recover from serious negative marks.

Does checking my own credit score lower it?

No. When you check your own score or report, it’s recorded as a soft inquiry, which has no effect on your score. Only hard inquiries, which happen when a lender checks your credit because you applied for something, can lower it slightly. You can check your own score as often as you want without any penalty.

Do I need to carry a balance on my credit card to build credit?

No, and this is one of the most expensive myths out there. You build positive payment history simply by using the card and paying it off. Paying your statement balance in full each month avoids interest entirely while still reporting on-time payments to the bureaus. Carrying a balance just costs you money in interest without helping your score.

Is it bad to close a credit card I don’t use?

It often is. Closing a card removes its credit limit from your total available credit, which can raise your utilization percentage, and over time it can lower the average age of your accounts. If the card has no annual fee, it’s usually better to keep it open with a small recurring charge. If it has a fee, ask the issuer about downgrading to a no-fee version instead of closing it.

Where can I get my credit report for free?

Use AnnualCreditReport.com, the official site authorized to provide free reports from Equifax, Experian, and TransUnion. Be cautious of similar-sounding websites that try to charge you or sign you up for a paid subscription. Reviewing your reports regularly is the best way to catch errors and signs of identity theft early.

The bottom line

Improving your credit score comes down to a short list of repeatable habits: pay on time every time (autopay makes this automatic), keep your card balances low, hold onto your older accounts, apply for new credit sparingly, and check your reports for errors you can dispute for free. None of it requires paying a “credit repair” company, and none of it requires carrying a balance. Stay consistent, give it a few months, and verify any time-sensitive details with the official sources before you act.

For more beginner-friendly money guidance, explore our related WalletWisp guides on budgeting, choosing your first credit card, and avoiding common financial scams.

")

{kind=link}