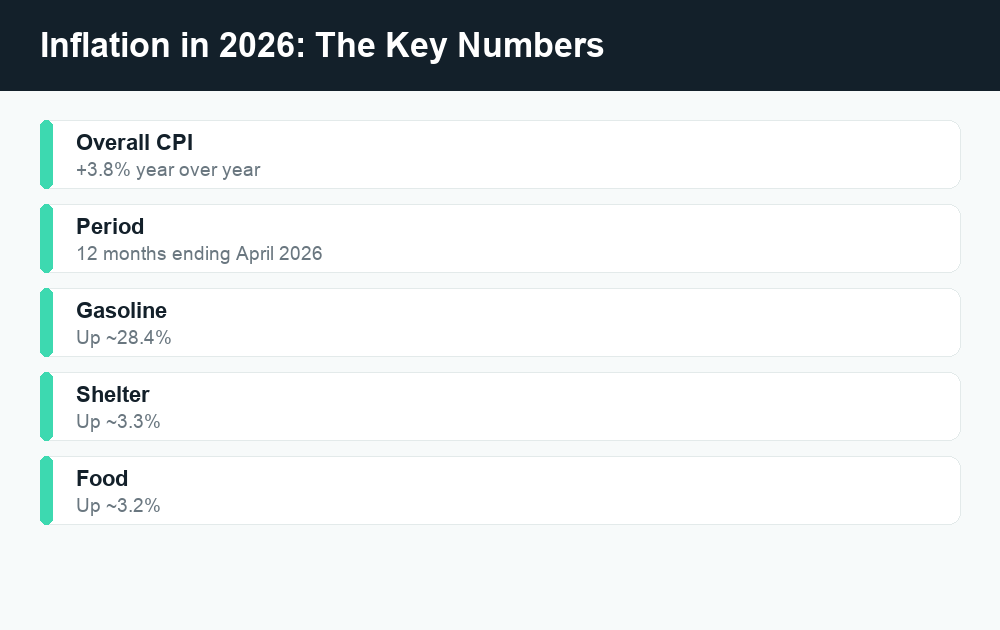

Inflation in 2026 climbed to 3.8% over the 12 months ending in April, the largest annual increase since May 2023. The biggest culprits were gasoline (up about 28.4% year over year), shelter, and broader energy costs, which means most U.S. households are feeling the squeeze most at the gas pump and on their monthly housing bill.

Quick answer: The Consumer Price Index rose 3.8% in the year ending April 2026, the steepest jump since May 2023. Gasoline led the way at roughly 28.4%, while shelter (about 3.3%) and food (about 3.2%) added steady pressure. To protect your budget, track your spending, trim your biggest categories first, switch to generics, lower energy and grocery bills, build a cash buffer, look for ways to boost income, and park savings in a high-yield savings account.

What inflation actually means for your money

Inflation is the rate at which prices rise over time. When economists say inflation was 3.8% over the year ending April 2026, they mean a typical basket of goods and services cost about 3.8% more than it did 12 months earlier. The headline number comes from the Consumer Price Index (CPI), which the U.S. Bureau of Labor Statistics tracks each month.

That 3.8% figure matters because it is the largest annual increase since May 2023. After a long stretch of cooling, prices reaccelerated, and the rebound was not spread evenly. A few categories did most of the damage, which is actually good news for your budget: when you know exactly where the pressure is coming from, you can target your defenses instead of cutting everything blindly.

It helps to remember what inflation is not. A 3.8% inflation rate does not mean every price went up 3.8%. Some things rose far more, some barely moved, and a few may have fallen. Your personal inflation rate depends on how you spend. If you drive a lot, the gas spike hit you hard. If you rent in a tight market, shelter is your headache. Understanding your own mix is the first step to protecting your wallet.

Where prices rose the most in 2026

The 3.8% headline was driven heavily by energy and housing. Here is how the major categories stacked up over the 12 months ending April 2026.

| Category | Approx. 12-month change | What it covers |

|---|---|---|

| Gasoline | ~ +28.4% | Fuel for your vehicle; the single biggest mover |

| Shelter | ~ +3.3% | Rent and the cost of owning a home |

| Food | ~ +3.2% | Groceries and dining out |

| Overall CPI | +3.8% | The all-items basket combined |

Gasoline and energy

Gasoline was the standout, up roughly 28.4% from a year earlier. Energy prices are notoriously volatile because they respond quickly to global supply, geopolitics, and seasonal demand. A swing this large at the pump ripples through the rest of the economy, since shipping, food production, and delivery all rely on fuel. When energy spikes, you often feel it twice: once when you fill up, and again later when higher transport costs nudge up the price of other goods.

Shelter and housing

Shelter rose about 3.3%, and because housing is the largest single line item in most household budgets, even a modest percentage increase is a big dollar increase. Shelter costs in the CPI capture rent and an estimate of what homeowners would pay to rent their own homes. This category tends to move slowly but persistently, which makes it a steady drag on budgets rather than a sudden shock.

Food and everyday essentials

Food climbed about 3.2%, covering both groceries and restaurant meals. Food inflation is especially noticeable because you buy it constantly, so the higher prices show up every single week. Energy and housing drove much of the overall gain, but food is where many families feel inflation most, simply because of how often they shop.

The real impact on households

When prices rise faster than your paycheck, your money buys less. That is the core problem with inflation: unless your income grows at least as fast as prices, your standard of living quietly slips. A 3.8% increase may sound small, but stacked on top of the price increases of recent years, it compounds.

The pain is also uneven. Lower- and middle-income households spend a larger share of their income on necessities such as gas, rent, and groceries, which are exactly the categories that rose the most in 2026. That means the families with the least room to absorb higher costs are often the ones hit hardest. Retirees on fixed incomes and anyone whose pay has not kept up also feel a tighter pinch.

There is a silver lining worth knowing: some payments are designed to keep pace with inflation. Social Security benefits, for example, receive an annual cost-of-living adjustment (COLA) tied to inflation. The exact amount changes each year and is set by the Social Security Administration, so check SSA.gov for the current figure rather than assuming. Some wages, contracts, and tax brackets also adjust over time, though rarely as fast as you might like.

How to protect your budget from inflation

You cannot control the inflation rate, but you can control how you respond to it. The goal is simple: widen the gap between what you earn and what you spend, and steer your cuts toward the categories that climbed the most. Here are seven concrete tactics, in roughly the order you should tackle them.

1. Track your spending first

You cannot fix a leak you cannot see. Before cutting anything, spend two or three weeks logging every dollar, either in a budgeting app, a spreadsheet, or by reviewing your bank and card statements. Sort spending into categories so you can see exactly where your money goes. Most people are surprised by how much lands in a few buckets. This step costs nothing and is the foundation for every move that follows.

2. Cut the biggest categories first

A 10% trim on your largest expense saves more than eliminating several tiny ones. For most households the heavy hitters are housing, transportation (including gas), food, and subscriptions. Ask hard questions: Can you refinance or renegotiate anything? Combine trips or carpool to burn less fuel? Drop streaming services you rarely watch? Focus your energy where the dollars are, not on skipping the occasional coffee.

3. Buy generic and shop smarter

Store-brand groceries, medications, and household goods are frequently made to similar standards as name brands but cost noticeably less. Switching generics across your grocery list can shave a meaningful amount off every trip with little change in quality. Pair that with planning meals around what is on sale, using a list to avoid impulse buys, checking unit prices, and leaning on store loyalty programs and cash-back apps.

4. Lower your energy and grocery bills

With gas and energy leading 2026’s increases, these are high-value targets. To cut fuel costs, keep tires properly inflated, drive smoothly, combine errands, and use a gas-price app to find cheaper stations. At home, lower energy use by adjusting your thermostat a few degrees, sealing drafts, switching to LED bulbs, and running large appliances during off-peak hours if your utility offers time-of-use rates. On groceries, reducing food waste, batch-cooking, and eating out less often add up quickly.

5. Build a cash buffer

Inflation makes emergencies more expensive, so a financial cushion matters more than ever. Aim to build an emergency fund covering three to six months of essential expenses. If that feels out of reach right now, start smaller. Even a few hundred dollars set aside can keep a surprise car repair or medical bill from going on a high-interest credit card, which is its own kind of budget killer.

6. Boost your income

Cutting expenses has a floor, but income has more room to grow. Options include asking for a raise (especially if your pay has not kept up with rising prices), picking up a side gig, selling items you no longer use, or turning a skill into freelance work. Even a modest extra stream of income can offset higher gas and grocery bills and rebuild your savings faster.

7. Use a high-yield savings account

Money sitting in a traditional checking or low-rate savings account loses purchasing power as prices rise. A high-yield savings account (often offered by online banks) typically pays far more interest than the national average, helping your cash keep more of its value. Look for an account that is FDIC-insured, charges no monthly fees, and has no minimum-balance traps. Rates change constantly, so compare current offers before opening one, and never wire money or share login details with anyone who contacts you out of the blue claiming to offer a special rate.

Watch out for inflation-related scams

Tough economic news is a goldmine for scammers, who lean on urgency and fear. Be skeptical of anyone promising “inflation relief checks,” guaranteed high investment returns, or government payments that require an upfront fee or your bank login. Legitimate federal benefits, including any cost-of-living adjustments, are announced through official channels such as IRS.gov and SSA.gov, never through a random text, email, or social media ad. If an offer pressures you to act immediately or pay to receive money, treat it as a red flag and walk away.

Frequently asked questions

What was the inflation rate in 2026?

The Consumer Price Index rose 3.8% over the 12 months ending April 2026, the largest annual increase since May 2023. Energy and housing drove much of the gain. For the most current monthly figure, check the official source at the U.S. Bureau of Labor Statistics, since the rate is updated regularly.

Why did gas prices go up so much?

Gasoline rose about 28.4% year over year, the single biggest mover in 2026. Energy prices are highly volatile and respond quickly to global supply, geopolitical events, and seasonal demand. Because so many other goods rely on fuel for production and shipping, a large gas spike can push up prices elsewhere too.

Does inflation mean everything costs 3.8% more?

No. A 3.8% inflation rate is an average across a wide basket of goods and services. Some categories rose much more (gasoline jumped roughly 28.4%), some less, and a few may have fallen. Your personal inflation rate depends on how you spend, so a heavy driver or a renter in a tight market may feel a higher rate than the headline number.

Will my Social Security or wages keep up with inflation?

Social Security benefits receive an annual cost-of-living adjustment (COLA) tied to inflation, and some wages and tax brackets adjust over time as well. However, these adjustments do not always match price increases dollar for dollar, and the timing can lag. The exact COLA changes each year and is set by the Social Security Administration, so verify the current figure at SSA.gov.

What is the single best move to protect my budget?

Start by tracking your spending so you know where your money actually goes, then cut your biggest categories first. Pairing those two steps with a high-yield savings account for your cash buffer gives you the most protection for the least effort. There is no one trick, but targeting the largest expenses beats trimming many tiny ones.

The bottom line

Inflation reaccelerating to 3.8% in 2026 is a real headwind, especially with gas up sharply and housing climbing steadily. But the same data that delivers the bad news also hands you a roadmap: you know which categories rose most, so you know where to aim. Track your spending, attack your biggest expenses, switch to generics, drive down energy and grocery bills, build a cash buffer, grow your income, and let a high-yield savings account work for you. Stay alert for scams that prey on economic anxiety, and verify any time-sensitive figures with official sources like BLS, IRS.gov, and SSA.gov before acting.

For more ways to stretch every dollar, explore our related WalletWisp guides on building an emergency fund, choosing a high-yield savings account, and cutting your monthly bills.

{kind=link}