: What It Means for Your Savings, Loans & Credit Cards")

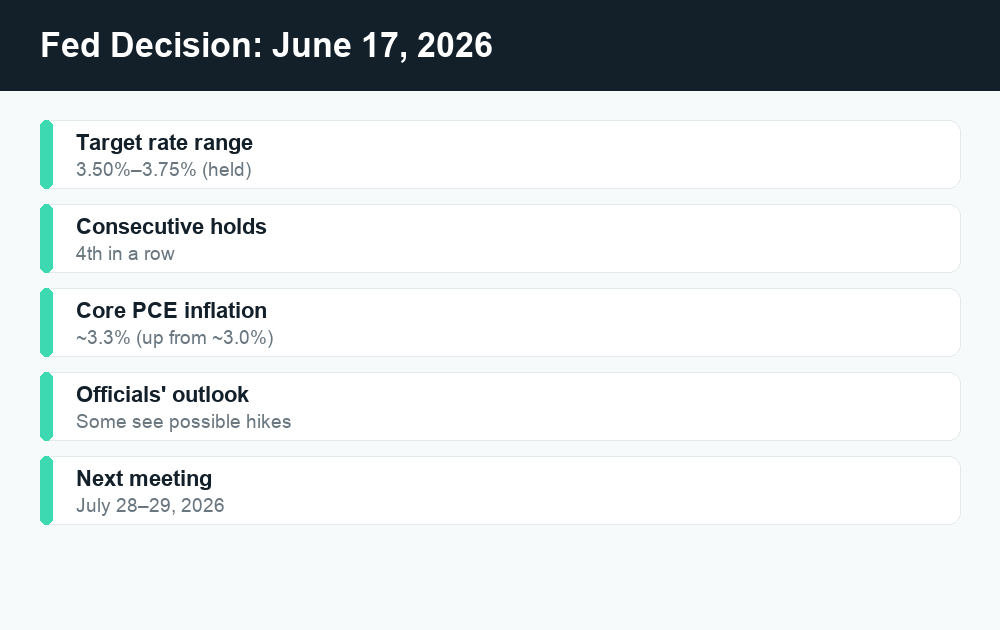

At its June 17, 2026 meeting, the Federal Reserve held its benchmark federal funds rate steady at a target range of 3.50%–3.75% — the fourth straight time it has chosen to leave rates unchanged. For your money, a “hold” means the recent status quo largely continues: high-yield savings accounts and CDs stay relatively attractive for now, mortgages remain in the rough 6% range, and credit card APRs stay painfully high, so paying down balances is still the smartest move.

Quick answer: The Federal Reserve kept its target rate at 3.50%–3.75% on June 17, 2026, marking the fourth consecutive hold. Because core inflation has ticked back up to roughly 3.3%, some Fed officials are even floating possible rate hikes this year rather than cuts. Practically, savers should lock in today’s still-elevated yields, while borrowers should keep attacking high-rate debt. The next decision comes at the July 28–29, 2026 meeting — always verify the latest figures at federalreserve.gov.

What a “rate hold” actually means

The federal funds rate is the interest rate banks charge one another for overnight loans, and it’s the lever the Federal Reserve uses to influence the broader cost of borrowing across the economy. When the Fed “holds,” it leaves that target range exactly where it was at the previous meeting — in this case, 3.50%–3.75%.

A hold is neither a cut nor a hike. It signals that the Fed’s policymaking committee, the Federal Open Market Committee (FOMC), believes the current setting is appropriate while it watches how the economy and inflation evolve. June 2026 marked the fourth hold in a row, which tells you the central bank is firmly in “wait and see” mode rather than actively pushing rates in either direction.

Why does this matter to your wallet? Because the federal funds rate ripples outward. It directly shapes the prime rate, which in turn anchors the APRs on credit cards, home equity lines of credit, and many variable-rate loans. It also influences what banks pay you on savings and what lenders charge for mortgages and auto loans. When the Fed holds, the rates you see day to day tend to stay roughly where they’ve been — though they can still drift based on competition, the bond market, and lender appetite.

Why the Fed is holding (and even eyeing hikes)

The Fed has a dual mandate: keep prices stable and keep employment strong. To gauge prices, it leans heavily on a measure called core PCE inflation, which strips out volatile food and energy costs to reveal the underlying trend.

Here’s the wrinkle in 2026: core PCE inflation has risen to roughly 3.3%, up from about 3.0% in December 2025. That’s moving in the wrong direction, away from the Fed’s long-stated 2% goal. When inflation climbs, cutting rates would risk pouring fuel on the fire, so the Fed has stayed put.

More striking, several Fed officials now project the possibility of rate hikes rather than cuts later this year. That’s a meaningful shift in tone. For much of the prior two years, the market debate was about how soon and how fast the Fed would cut. Now the conversation has flipped toward whether rates may need to go higher to bring inflation back under control. Nothing is decided — the Fed has emphasized it remains data-dependent — but the door to higher rates is no longer closed.

| What changed | December 2025 | June 2026 |

|---|---|---|

| Fed funds target range | 3.50%–3.75% | 3.50%–3.75% (held) |

| Core PCE inflation (approx.) | ~3.0% | ~3.3% |

| Direction officials are signaling | Mixed | Some see possible hikes |

| Next scheduled decision | — | July 28–29, 2026 |

Figures are approximate and drawn from the Fed’s June 2026 communications. Confirm the latest data at federalreserve.gov before making decisions.

What it means for your high-yield savings and CDs

Here’s the good news if you’re a saver: when the Fed holds at an elevated level, the yields on high-yield savings accounts (HYSAs), money market accounts, and certificates of deposit (CDs) tend to stay relatively generous. Many online banks have continued offering yields well above what traditional brick-and-mortar savings accounts pay.

That said, savings rates are not guaranteed. The yield on a high-yield savings account is variable, meaning your bank can lower it at any time — and banks often trim those rates in anticipation of future Fed moves, not just after them. With some officials now talking about hikes, savings yields could even hold steady or edge up, but there are no promises.

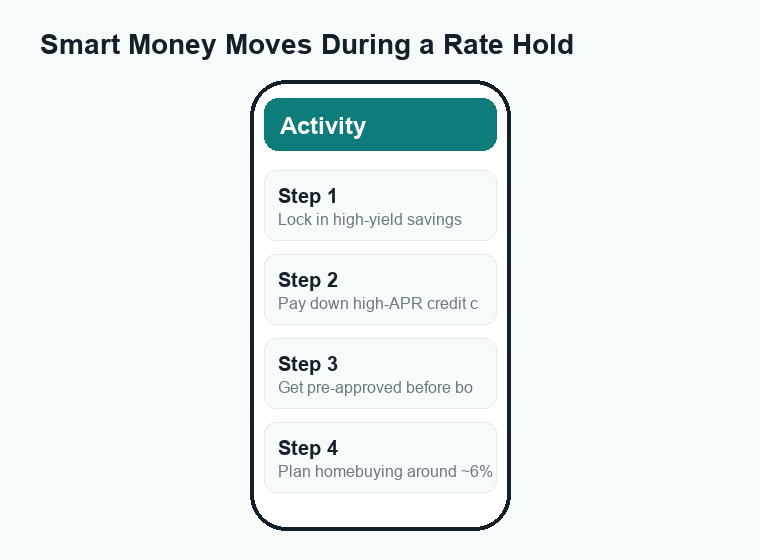

This is exactly why CDs deserve a look right now. A CD locks in a fixed rate for a set term — say 6 months, 1 year, or longer. If you believe today’s elevated yields won’t last forever, locking part of your cash into a CD guarantees that rate for the full term, even if savings accounts later fall. A common strategy is “CD laddering,” where you split money across several CDs with staggered maturity dates so you always have some cash coming available while still capturing longer-term rates.

A few practical tips for savers in this environment:

- Compare yields, not just brand names. Online banks frequently beat big national banks by a wide margin. Always check the current APY before opening an account.

- Mind the fine print. Watch for minimum balance requirements, monthly fees, and whether the advertised rate is an introductory teaser.

- Confirm FDIC or NCUA insurance. Stick with banks insured by the FDIC or credit unions insured by the NCUA so your deposits are protected up to the legal limit.

- Don’t lock up your emergency fund. Keep cash you might need quickly in a liquid HYSA, and only ladder money you won’t touch into CDs.

What it means for mortgages

Mortgage rates don’t move in lockstep with the federal funds rate — they track longer-term bond yields more closely — but the Fed’s posture still shapes the overall climate. With the Fed holding and inflation sticky, mortgage rates have stayed in roughly the 6% range rather than falling back to the ultra-low levels seen earlier in the decade.

For prospective homebuyers, the key takeaway is to plan around today’s rates rather than betting on a near-term drop. If officials are openly discussing hikes, waiting for dramatically cheaper mortgages could be a long bet. Focus instead on what you can control: improving your credit score, saving a larger down payment, and shopping multiple lenders, since rate quotes can vary meaningfully from one lender to the next.

If you already have a mortgage at a higher rate, keep an eye on the market but don’t count on a refinance windfall this year. Refinancing makes sense only when the new rate is low enough to recoup your closing costs within a reasonable time. Run the numbers carefully, and verify current rates with lenders directly rather than relying on headline averages.

What it means for credit cards

This is where a Fed hold hits hardest — and where you have the most power to act. Credit card APRs are tied to the prime rate, which moves with the federal funds rate. Because the Fed is holding at an elevated level (and may even hike), credit card interest rates remain high. Carrying a balance month to month is one of the most expensive forms of debt most households face.

A rate hold won’t bring your card’s APR down. If anything, the risk now tilts toward rates staying high or climbing. So the strategy is straightforward: pay down high-interest credit card balances as aggressively as your budget allows. Every dollar of balance you eliminate is a guaranteed return equal to your card’s APR — a return that’s hard to beat anywhere else.

Tactics that can help:

- Attack the highest-APR card first (the “avalanche” method) to minimize total interest paid, or the smallest balance first (the “snowball” method) if you need quick motivational wins.

- Consider a 0% balance-transfer offer if you qualify, but read the terms: there’s usually a transfer fee, and the promotional rate expires, after which a high APR returns.

- Pay more than the minimum. Minimum payments are designed to keep you in debt for years; even modest extra payments shorten the payoff dramatically.

- Stay scam-aware. Be wary of unsolicited calls or texts promising to “lower your interest rate” or “consolidate your debt” for an upfront fee. Legitimate help doesn’t demand payment before doing anything. When in doubt, contact your card issuer directly using the number on the back of your card.

What it means for auto loans

Auto loan rates also tend to stay elevated when the Fed holds at higher levels, because lenders’ funding costs remain high. Whether you’re financing a new or used vehicle, expect to pay more in interest than buyers did a few years ago.

The smart moves here mirror the mortgage playbook. Shop for financing the same way you shop for the car itself: get pre-approved through your bank or credit union before you walk into a dealership, so you have a benchmark rate to compare against the dealer’s offer. A stronger credit score and a larger down payment will both lower your rate and your total interest. And be cautious about stretching the loan term to 72 or 84 months just to shrink the monthly payment — longer terms mean you pay far more interest overall and risk owing more than the car is worth.

Savers vs. borrowers: what to do now

The current environment rewards two simple habits — and they point in opposite directions depending on which side of the ledger you’re on.

| If you’re a… | Smart move in a rate-hold environment |

|---|---|

| Saver | Lock in today’s elevated yields with HYSAs and CDs; ladder CDs; keep your emergency fund liquid. |

| Credit card holder | Pay down balances aggressively; consider a 0% transfer; never just pay the minimum. |

| Homebuyer | Plan around ~6% rates; boost credit and down payment; shop multiple lenders. |

| Car buyer | Get pre-approved before the dealership; avoid ultra-long loan terms. |

| Everyone | Build an emergency fund and avoid taking on new high-interest debt. |

The overarching theme: when borrowing is expensive and saving is rewarding, prioritize cash that’s working for you (in insured savings) over debt that’s working against you (on high-APR cards). That balance is the foundation of nearly every sound financial plan, regardless of what the Fed does next.

Frequently asked questions

Did the Fed raise or lower rates in June 2026?

Neither. At the June 17, 2026 meeting, the FOMC held the federal funds target range steady at 3.50%–3.75%. It was the fourth consecutive hold, meaning rates have been left unchanged at four straight meetings.

Could the Fed actually raise rates this year?

It’s possible. Core PCE inflation rose to roughly 3.3% (up from about 3.0% in December 2025), and several Fed officials now project the possibility of rate hikes rather than cuts later in 2026. Nothing is guaranteed — the Fed says it remains data-dependent — but higher rates are back on the table. The next decision comes at the July 28–29, 2026 meeting.

Will my high-yield savings rate go down now?

Not necessarily because of this hold. Savings yields are variable and can change at any time, but when the Fed holds at an elevated level, HYSA and CD rates often stay relatively attractive. If you want certainty, a CD lets you lock in a fixed rate for its term. Always confirm the current APY before opening an account.

Should I pay off my credit card or save more money?

For most people carrying a balance, paying off high-APR credit card debt comes first. The interest rate on credit card debt almost always exceeds what you can earn in savings, so eliminating that balance delivers a guaranteed return. The common exception is keeping a small emergency fund so you don’t have to borrow again when a surprise expense hits.

Where can I verify the latest Fed decision and rates?

Go straight to the source. The Federal Reserve publishes its decisions and the official target range at federalreserve.gov. For inflation data, the Bureau of Economic Analysis and the IRS-adjacent federal sources are authoritative. Time-sensitive numbers change, so always confirm the current figures before acting.

The bottom line

The Fed’s June 2026 decision to hold rates at 3.50%–3.75% — its fourth straight hold, with some officials now eyeing possible hikes — means the recent landscape continues: rewarding for savers, expensive for borrowers. Use it to your advantage by locking in today’s still-elevated savings yields, attacking high-interest credit card and auto debt, and planning your homebuying around current rates rather than hoped-for cuts. Watch the July 28–29 meeting for the next signal, and always verify the numbers at federalreserve.gov. For more, see WalletWisp’s related guides on high-yield savings accounts, building an emergency fund, and paying down credit card debt.

{kind=link}