Yes, cash stuffing and no-spend challenges can genuinely work, but mostly as short-term tools to break overspending habits, not as a complete money plan. Cash stuffing forces awareness by making you physically hand over bills, while a no-spend challenge resets your spending reflexes for a set window, and both lose their power if you never connect them to a real budget.

Quick answer: Cash stuffing means withdrawing cash and dividing it into labeled envelopes or a binder so you can only spend what’s in each category. A no-spend challenge means buying nothing but essentials for a set period to reset habits. Both create helpful “friction” and awareness, but cash stuffing costs you card rewards and high-yield savings interest and carries the risk of lost or stolen cash, while no-spend challenges aren’t a long-term plan. Use them to jump-start change, then graduate to a real budget like 50/30/20 paired with a high-yield savings account.

Open any money corner of social media in 2026 and you’ll see two trends on repeat: people fanning out cash into color-coded envelopes, and others posting day-by-day updates of a “no-spend month.” Both have exploded in popularity, especially with younger savers who grew up tapping cards and phones and never really felt money leave their hands. The question worth asking before you join in is simple: do these trends actually work, or are they just satisfying videos?

The honest answer is that both can help, but they solve a specific problem (impulsive, autopilot spending) and come with real trade-offs. This guide explains how each method works step by step, the psychology behind why they help, and the pros and cons no viral video bothers to mention, so you can decide whether either belongs in your financial toolkit.

What is cash stuffing (the envelope method)?

Cash stuffing is a modern, social-media-friendly rebrand of the decades-old envelope budgeting method. The idea is straightforward: instead of swiping a card and tracking spending after the fact, you withdraw physical cash and divide it among labeled envelopes (or slots in a “budget binder”), one for each spending category. When an envelope is empty, you stop spending in that category until the next time you refill it.

The appeal is that it turns an abstract number on a banking app into something you can see and touch. There’s no overdraft, no “I’ll check the balance later,” and no end-of-month surprise. The limit is literally in your hands.

How cash stuffing works, step by step

- List your spending categories. Common ones include groceries, gas, dining out, entertainment, personal care, and “fun money.” Keep fixed bills like rent and utilities out of cash (more on that below).

- Set a dollar amount for each category. Base these on what you actually earn and spend, not wishful thinking. This is your budget.

- Withdraw the cash. After payday, take out the total for your cash categories and break it into the right denominations.

- Stuff the envelopes. Put each category’s cash into its labeled envelope or binder slot.

- Spend only what’s inside. When you buy groceries, pay from the grocery envelope. When it’s empty, you’re done for that cycle.

- Reconcile and refill. At the end of the cycle, note what’s left over, decide whether to roll it into savings, and refill for the next period.

Many people keep some categories on cash and others (like fixed bills and subscriptions) on autopay, which is a sensible hybrid rather than going all-cash for everything.

What is a no-spend challenge?

A no-spend challenge is exactly what it sounds like: for a set period, you spend money only on essentials and pause everything else. Essentials typically mean rent or mortgage, utilities, groceries, transportation to work, insurance, and minimum debt payments. Everything discretionary, such as takeout, new clothes, impulse buys, streaming add-ons, and coffee runs, goes on hold.

The length is up to you. A “no-spend weekend” is a gentle start, a “no-spend week” is a common middle ground, and a “no-spend month” is the version that tends to go viral. The point isn’t to suffer; it’s to interrupt automatic spending long enough to notice your patterns and break the habit loop.

How to run a no-spend challenge

- Pick your window. Start short if you’re new to it. A week is plenty to learn something.

- Define your rules in writing. Decide exactly what counts as an “essential” before you start, so you’re not negotiating with yourself in the moment.

- List your known exceptions. A pre-planned birthday gift or a prescription refill is fine; write it down up front so it’s a decision, not a slip.

- Plan around the gaps. Cook what’s already in your pantry, line up free activities, and unsubscribe from promotional emails for the week.

- Track and reflect. Note every urge to spend and what triggered it. The urges you record are your real budgeting lesson.

Why these trends actually help: the psychology

Neither method is magic. They work because of two well-understood behavioral principles.

Friction. Tapping a card or phone is frictionless by design, which is great for merchants and dangerous for impulse control. Cash stuffing deliberately adds friction: you have to physically count out bills and watch the envelope get thinner. Studies of consumer behavior have long suggested that paying with cash feels more “painful” than paying with plastic, and that small pain is exactly what slows down impulse purchases. A no-spend challenge adds a different kind of friction: a flat rule (“not this month”) removes the constant micro-decision of whether each purchase is worth it.

Awareness. Most overspending happens on autopilot. When every dollar has a job and a visible limit, you’re forced to confront trade-offs in real time: buying this means less of that. No-spend challenges create awareness by subtraction. When you can’t spend on the usual things, you suddenly see how often you reached for them out of boredom, stress, or habit rather than genuine need.

In short, these trends help most when your problem is behavioral, not mathematical. If you earn enough but keep leaking money on impulse buys, friction and awareness are the right medicine.

The honest pros and cons

Here’s where the viral videos go quiet. Both methods carry real downsides that matter for your long-term finances.

| Method | Best for | Real downsides |

|---|---|---|

| Cash stuffing | Chronic overspenders; people who ignore app balances; anyone who needs a hard, visible limit | You forfeit credit-card rewards and cash back; cash sitting in envelopes earns zero interest (vs. a high-yield savings account); lost or stolen cash is gone for good; clunky for online bills and shopping |

| No-spend challenge | Resetting habits; finding hidden spending leaks; recovering after a splurge or holiday | It’s a sprint, not a system; the “deprivation” can trigger a rebound spending spree afterward; it doesn’t fix the underlying budget; easy to quietly stockpile a wish list and buy it all on day one after |

The cash stuffing trade-offs in plain English

The biggest hidden cost of cash stuffing is opportunity cost. Money in an envelope does nothing. That same money in a high-yield savings account (HYSA) earns interest, and rates in recent years have been meaningfully higher than the near-zero of a traditional account. Pulling large amounts of cash to sit in a drawer means giving up that interest, and giving up any credit-card rewards or cash back you’d earn by spending strategically and paying the balance in full.

There’s also plain cash risk. Bills in your home aren’t insured the way bank deposits are. If envelopes are lost, stolen, or damaged, there’s no fraud department to call. For this reason, never keep large sums of cash around, and never carry your full month’s budget in your bag at once.

The no-spend challenge trade-offs in plain English

A no-spend challenge is a reset button, not an operating system. It can absolutely break a bad streak and surface spending you didn’t realize you were doing. But on its own it doesn’t tell you what a sustainable budget looks like, and the deprivation framing can backfire. If you white-knuckle through a no-spend month and then “reward” yourself with a shopping spree, you may end up roughly where you started. The challenge only pays off if you carry the lessons into a permanent plan.

Who benefits most from each?

- You’re a good fit for cash stuffing if: you consistently overspend, you tune out digital balances, your overspending is concentrated in a few categories like dining and shopping, and you’re disciplined enough to handle physical cash safely. It’s especially useful while you’re rebuilding control after debt trouble.

- You’re a good fit for a no-spend challenge if: you want a quick diagnostic of where your money actually goes, you’re recovering from a big spending event, or you need momentum to kick off a longer-term budgeting effort.

- You may not need either if: you already track spending, pay credit cards in full each month, and hit your savings goals. In that case, the rewards and interest you’d give up by going all-cash likely outweigh the behavioral benefit. There’s no prize for using a harder method than you need.

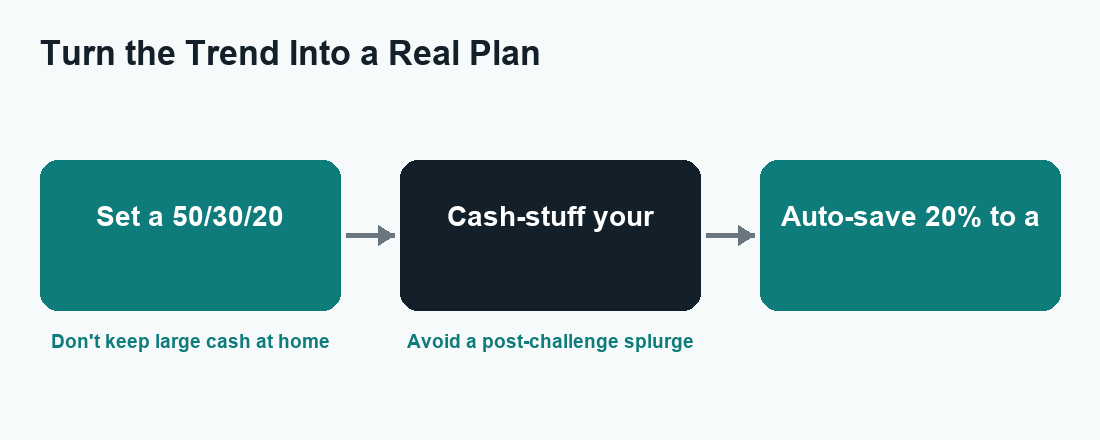

How to combine the trends with a real budget

The smartest move is to treat these trends as on-ramps to a durable system rather than the destination. Here’s how the pieces fit together.

Start with a real budget framework: 50/30/20

The 50/30/20 rule is a simple, widely used starting point: aim for roughly 50% of your take-home pay on needs (housing, utilities, groceries, transportation, insurance, minimum debt payments), 30% on wants (dining out, entertainment, hobbies), and 20% on savings and extra debt payoff. These are guidelines, not gospel; high-cost-of-living areas often need to bend the percentages. The point is to give every dollar a category before the month begins.

Use cash stuffing only where it earns its keep

You don’t have to go all-cash to get the benefit. A practical hybrid looks like this:

- Keep fixed needs (rent, utilities, insurance, subscriptions) on autopay so nothing important is ever late.

- Apply cash stuffing only to the “wants” categories where you tend to overspend, such as dining, entertainment, and impulse shopping. That’s where physical friction does the most good.

- Keep the cash you actually carry small, refilling weekly rather than monthly to limit loss risk.

Park your savings in a high-yield savings account, not an envelope

This is the key correction to the cash-stuffing trend. The 20% you’re setting aside should not sit in an envelope earning nothing. It belongs in a high-yield savings account, where it’s FDIC-insured (at a bank) or NCUA-insured (at a credit union), safe from theft, and actually earning interest. Automate the transfer on payday so saving happens before you can spend it. You get the behavioral win of cash stuffing on your discretionary spending and the financial win of compounding interest on your savings.

Run a no-spend challenge as a periodic tune-up

Use no-spend challenges occasionally rather than as your main strategy: a no-spend week after the holidays, or a no-spend month to fast-track an emergency fund. Each round is a chance to re-examine your categories and tighten the budget. The lessons (the urges you logged, the subscriptions you didn’t miss) should feed straight back into your 50/30/20 numbers.

A quick word on scams and safety

Budgeting trends themselves aren’t scams, but their popularity attracts bad actors. Be wary of anyone selling “cash stuffing systems,” paid templates promising guaranteed results, or “money challenge” apps that ask for your bank login or upfront fees. You don’t need to pay anyone to put cash in an envelope or skip purchases for a week. And remember the core safety rules: keep household cash minimal, store savings in an insured account, and verify any account or rate details on the official source, whether that’s your bank, IRS.gov, or SSA.gov, before acting on time-sensitive information.

Frequently asked questions

Is cash stuffing better than using a budgeting app?

Neither is universally “better.” Cash stuffing wins on tactile friction and a hard limit, which helps chronic overspenders. Budgeting apps win on convenience, automatic tracking, and not forcing you to give up card rewards or savings interest. Many people get the best of both by app-tracking their full budget while cash-stuffing only the categories where they overspend.

Do no-spend challenges really save money?

They can, but the lasting value is behavioral more than financial. A single no-spend month might save a noticeable amount, yet that benefit evaporates if you binge afterward. The real payoff is discovering your spending triggers and feeding those lessons into a permanent budget so the savings continue long after the challenge ends.

How much cash should I keep in envelopes?

As little as practical. Only stuff what you’ll spend in the near term, ideally refilling weekly rather than carrying a full month at once. Cash at home isn’t insured against loss or theft, so keep amounts modest and store your actual savings in a high-yield savings account instead.

Can I do cash stuffing and still earn credit card rewards?

Not on the categories you pay in cash, since you’re not using a card there. If rewards matter to you, reserve cash stuffing for the few categories where you struggle with impulse control, and keep disciplined, paid-in-full card spending for the rest. That hybrid preserves most of your rewards while still applying friction where you need it.

Are these trends a replacement for a full budget?

No. Cash stuffing is a spending-control tactic and a no-spend challenge is a temporary reset. Both work best layered on top of a real budgeting framework like 50/30/20, paired with automated savings into an insured high-yield account. Use the trends to change behavior, not to replace planning.

The bottom line

Cash stuffing and no-spend challenges deserve their popularity because they target a genuine problem: frictionless, autopilot spending. They build awareness and slow down impulse buys in a way that pure willpower often can’t. But neither is a complete plan, and cash stuffing in particular can quietly cost you card rewards, savings interest, and security if you take it too literally. Use them as tools, not religions: apply friction where you overspend, run an occasional reset, and anchor everything to a real budget and an insured high-yield savings account. For more, see our related WalletWisp guides on the 50/30/20 budget, choosing a high-yield savings account, and building your first emergency fund.

")

{kind=link}