For most people in 2026, the smartest place for cash is a layered setup: keep your emergency fund in a high-yield savings account (HYSA) for instant access, lock money you won’t touch for a set period into a certificate of deposit (CD), and use a money market account (MMA) when you want a higher balance with check-writing or debit access. All three are safe when held at an FDIC-insured bank or NCUA-insured credit union, and all three pay far more than a traditional checking account.

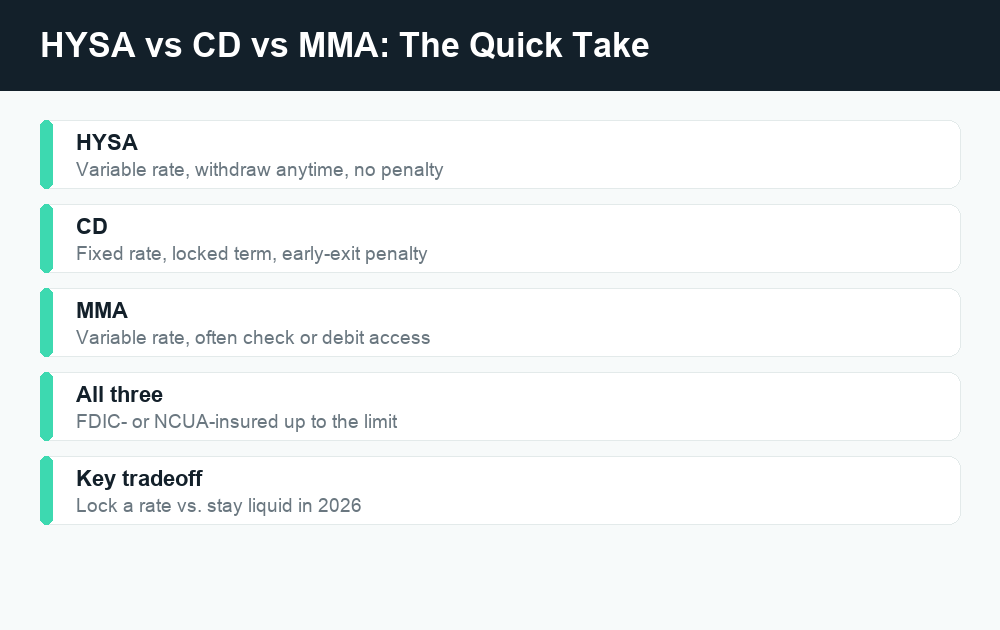

Quick answer: A high-yield savings account is best for your emergency fund and everyday savings because you can withdraw anytime. A CD locks in today’s rate for a fixed term, which is useful when rates are uncertain but means an early-withdrawal penalty if you cash out early. A money market account sits in between, often pairing a competitive rate with check or debit access. Match each tool to a job rather than picking just one.

Interest rates are still elevated in mid-2026, but the Federal Reserve has been holding steady and the direction from here is uncertain. That backdrop matters for one simple reason: deciding whether to lock a rate with a CD or stay liquid in a savings or money market account is a real tradeoff right now. If rates fall, the person who locked a CD looks smart. If rates climb or you need the money sooner than planned, staying liquid wins. This guide walks through how each account works, compares them side by side, and gives you a plain-English framework for deciding where each dollar should live.

The three accounts at a glance

All three are deposit accounts, meaning you’re handing cash to a bank or credit union that pays you interest for the privilege of holding it. None of them invest your money in stocks or bonds, so you can’t lose your principal the way you can in the market. The differences come down to four things: how much interest you earn (APY), how easily you can get your money out (liquidity), how much you need to open the account (minimums), and what extra features come along for the ride.

High-yield savings accounts (HYSA)

A high-yield savings account is a regular savings account that pays a much higher annual percentage yield than the rock-bottom rate most big brick-and-mortar banks offer. They’re usually offered by online banks, which keep costs low and pass the savings on to you. Your money stays fully liquid: you can transfer it to your checking account in a day or two, and there’s no penalty for taking it out. The rate is variable, so it can rise or fall as broader interest rates move.

Certificates of deposit (CDs)

A CD is a time deposit. You agree to leave a lump sum untouched for a set term, anywhere from a few months to several years, and in exchange the bank pays you a fixed APY that’s locked in for the whole term. The tradeoff is access: if you withdraw before the maturity date, you typically pay an early-withdrawal penalty, often a chunk of the interest you’ve earned. Because the rate is fixed, a CD shields you from falling rates, which is exactly why CDs draw attention when the Fed’s next move is unclear.

Money market accounts (MMA)

A money market account is a savings-style account that often pays a competitive yield while adding the convenience of a checkbook, a debit card, or both. It blends features of savings and checking. Minimums and tiers can be higher than a plain HYSA, and the best rates sometimes require keeping a larger balance. Like a savings account, the rate is variable. Note that a money market account at a bank is not the same thing as a money market fund, which is an investment product and is not FDIC-insured.

Side-by-side comparison

Here’s how the three stack up on the factors that matter most. Exact numbers change constantly, so this table focuses on how each account behaves rather than quoting a specific rate, which would be out of date by the time you read it.

| Feature | High-Yield Savings (HYSA) | Certificate of Deposit (CD) | Money Market (MMA) |

|---|---|---|---|

| Typical rate (APY) | High and variable; moves with the market | Fixed for the full term; locked at opening | Competitive and variable; sometimes tiered by balance |

| Access to your money | Anytime, no penalty (transfer takes a day or two) | Locked until maturity; early-withdrawal penalty applies | Anytime, often with checks or a debit card |

| Typical minimum | Often $0 to low; varies by bank | Varies; some require a set minimum deposit | Sometimes higher; best rates may need a larger balance |

| Insured? | Yes, FDIC (bank) or NCUA (credit union) | Yes, FDIC or NCUA | Yes, FDIC or NCUA |

| Best for | Emergency fund and everyday savings | Money you won’t need until a set date | Bigger balance you want to earn on but still tap |

The pattern is easy to see. HYSAs and MMAs keep your money flexible but expose you to falling rates over time. CDs do the opposite: they trade flexibility for a guaranteed rate. None is “best” in the abstract; the right one depends on when you’ll need the money.

What “insured” really means

This is the part that lets you sleep at night. Standard federal deposit insurance covers your money up to the legal limit per depositor, per insured institution, for each account ownership category. At banks, that protection comes from the FDIC; at credit unions, it comes from the NCUA. The exact coverage limit is set by federal rules, so confirm the current figure on FDIC.gov or NCUA.gov before assuming a large balance is fully protected.

Two practical takeaways. First, if your balance is approaching the coverage limit, you can spread money across more than one insured institution to stay fully covered. Second, always verify an account is actually insured before you deposit. A genuine bank or credit union will display its FDIC or NCUA membership, and you can look the institution up directly through the FDIC’s BankFind or the NCUA’s research tools. This matters because a money market fund (an investment) is not insured, even though its name sounds nearly identical to a money market account.

The lock-it-or-stay-liquid question in 2026

This is the decision that makes 2026 interesting. Rates are still high, but the Fed is holding and nobody can reliably predict the next move. That creates a genuine fork in the road:

- If you lock a CD and rates later fall, you’ll be glad you secured a higher fixed yield while it lasted. Your rate is guaranteed for the whole term regardless of what the market does.

- If you stay in an HYSA or MMA and rates climb, your variable yield rises with them, and you never tied up your cash.

- If you lock a CD and then need the money early, the early-withdrawal penalty can wipe out much of your interest, the worst outcome of the three.

You don’t actually have to guess. A CD ladder lets you hedge. Instead of putting one lump sum into a single CD, you split it across several CDs with staggered maturity dates, for example one-year, two-year, and three-year terms. As each rung matures, you either spend the cash or roll it into a new CD. A ladder gives you regular access to a portion of your money while still capturing fixed rates, so you’re not forced to bet everything on one prediction about the Fed.

A simple decision framework

Forget chasing the single highest number. The cleaner approach is to match each pot of money to the account that fits its job. Here’s the framework most personal-finance pros would recognize.

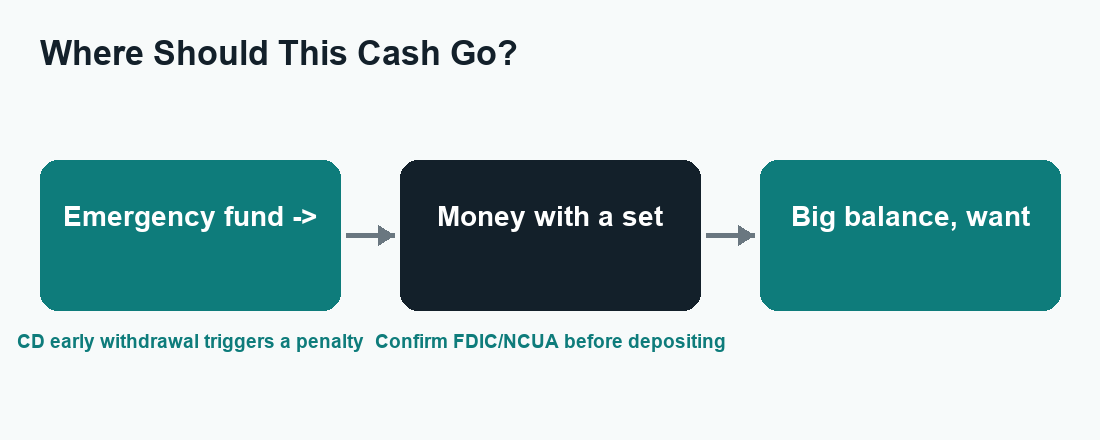

1. Emergency fund and short-term savings → HYSA

Money you might need on short notice, an emergency fund, a near-term bill, a buffer, belongs in a high-yield savings account. The whole point of this money is that you can reach it instantly without penalty. A CD would defeat the purpose, and the variable rate on an HYSA is a fair price for keeping it liquid. If you do nothing else after reading this article, moving your emergency fund out of a near-zero big-bank savings account and into an HYSA is the highest-value step.

2. Money you won’t need for a set term → CD or CD ladder

If you have a specific date in mind, a tuition bill 18 months out, a down payment in three years, money you’re certain you won’t touch, a CD locks in a known return and removes the temptation to spend it. Build a ladder if you want some of it to free up along the way. Just be honest with yourself about the timeline, because the early-withdrawal penalty is real.

3. Bigger balance you want to keep accessible → MMA

If you’re holding a larger cash balance, say, proceeds from a sale, a business reserve, or a big savings cushion, and you want to earn a solid rate while still writing the occasional check or using a debit card, a money market account is the natural fit. It rewards a higher balance with convenience that a plain savings account may not offer.

| Your situation | Where it usually goes |

|---|---|

| 3-6 months of expenses for emergencies | HYSA |

| Cash earmarked for a goal 1-5 years out | CD or CD ladder |

| Large balance you want to earn on and tap | MMA |

| Everyday spending money | Checking (not covered here) |

Many people use all three at once, and that’s the point. There’s no rule that says you must choose a single account type.

How to choose a specific account safely

Once you’ve decided on the account type, picking the right provider comes down to a few checks. Rates change weekly, so always confirm the current APY on the institution’s own site rather than trusting an old comparison article, including this one.

- Confirm FDIC or NCUA membership before depositing. Look it up directly through the regulator’s site, don’t just take a logo at face value.

- Read the fine print on fees and minimums. A headline rate means little if monthly fees or a high minimum balance eat into it.

- For CDs, check the early-withdrawal penalty and the term carefully before you commit.

- Watch for promo rates that expire or “introductory” yields that drop after a few months.

- Be alert to scams. If an “account” promises a yield that looks dramatically higher than everything else, or pressures you to act immediately, treat it as a red flag. Insured deposit accounts don’t pay outlandish returns.

Frequently asked questions

Is a high-yield savings account safe?

Yes, as long as it’s offered by an FDIC-insured bank or an NCUA-insured credit union, your money is protected up to the federal coverage limit per depositor, per institution, per ownership category. The “high yield” refers to the interest rate, not to any added risk. Verify the institution’s insured status on FDIC.gov or NCUA.gov before depositing.

What happens if I take money out of a CD early?

You’ll typically pay an early-withdrawal penalty, which is usually a portion of the interest you’ve earned and is set by the bank when you open the CD. In some cases the penalty can eat into your interest significantly, so only put money in a CD that you’re confident you won’t need before the maturity date. Check the specific penalty terms with the bank before committing.

What’s the difference between a money market account and a money market fund?

They sound alike but are very different. A money market account is a deposit account at a bank or credit union and is FDIC- or NCUA-insured. A money market fund is an investment product, usually held at a brokerage, and is not insured. This guide is about money market accounts. Always confirm which one you’re being offered.

Should I lock in a CD now or wait?

It depends on your timeline and your read on rates, and nobody can predict the Fed with certainty. If you have money you won’t need for a set period and want to guarantee today’s rate against a possible decline, a CD or a CD ladder makes sense. If you might need the money sooner or expect rates to rise, staying liquid in an HYSA or MMA is safer. A ladder lets you hedge both ways.

Can I use more than one of these accounts at the same time?

Absolutely, and most people should. A common setup is an HYSA for the emergency fund, a CD or ladder for goal-based savings with a known date, and an MMA for a larger balance you want to keep accessible. Matching each pot of money to the right tool beats forcing everything into a single account.

The bottom line

There’s no single winner among high-yield savings accounts, CDs, and money market accounts, because each is built for a different job. Keep your emergency fund liquid in an HYSA, lock money you won’t need into a CD or a CD ladder to capture today’s rate, and use an MMA for a larger balance you still want to reach. All three are safe when held at an insured institution, and all three beat letting cash sit idle in a big-bank account earning almost nothing. Just confirm current rates, fees, and insurance on the official source before you open anything, since the numbers move constantly in 2026.

For more on building your cash strategy, see our related WalletWisp guides on starting an emergency fund, building a CD ladder step by step, and choosing the best online banks.

")

{kind=link}